Social Security Laws for NGOs

- Social Security Laws for NGOs

- FAQ: Gratuity

- FAQ: Employees' Provident Fund (EPF)

- EPF Scheme 1952

- Pension Scheme

- EDLI Scheme

- PF contribution

- Advances & Withdrawals, Interest, and Settlement of Final Accounts

- Transfers and Transfer Claims of Employees

- TDS on Claims

- Grievance redressal

- FAQ: Shops & Establishment Act

- FAQ: Maternity Benefit Act, 1961

- FAQ: Professional Tax

Social Security Laws for NGOs

You can read the information below in over 15 languages! Simply use the translation tool in the top-left corner of the screen to select your preferred language, including অসমীয়া, বাংলা, ગુજરાતી, हिन्दी, ಕನ್ನಡ, മലയാളം, मराठी, মৈতৈলোন্, नेपाली, ଓଡ଼ିଆ, ਪੰਜਾਬੀ, संस्कृतम्, தமிழ், తెలుగు, and اُردُو.

Got questions about Social Security Law? Ask them on the forum or see what Social Security Laws related questions people are asking here.

Why comply with other laws

Section 12AB of Income Tax Act state that: For non-compliance of such requirements of any other laws for the time being in force by the trust or institution as are material for the purpose of achieving its objects. The CIT may cancel the registration certificate basis due process in law.

Social Security Regulations for NPOs-Snapshot

EPF: EPF, EPS and EDLI are 3 schemes under the Employees' Provident Funds and Miscellaneous Provisions Act, 1952 managed by EPFO. Aapplicability: Mmandatory for organizations with 20 or more employee (including employees through contractor unless it has a sperate code, Apprentices unless appointed under Payment of Apprentice Act) for establishment specified in Schedule 1. NGOs are covered under EPF since 1.4.2015 by law. In house PF trusts allowed if the return is equal or higher than what is paid by EPFO

ESI: Employees' State Insurance is a self-financing health insurance scheme for Indian workers. Ambiguity regarding applicability to an establishment but charitable medical and educational institutions run by trust, societies etc covered. The fund is managed by the Employees' State Insurance Corporation under ESI Act 1948.

Applicability: It is mandatory for organizations with 10 or more employee.

Minimum Wages Act 1948: Centre & states fix minimum wage, to be revised at least once every 5 years for scheduled employment. Per hour/day/month rate for 4 defined categories of workers i.e. unskilled, semi-skilled, skilled and highly skilled.

Professional Tax Act: Levied on persons earning income by way of either practicing a profession, employment, calling or trade. PT is levied by state/UT.

Applicability: Out of 28 states, PT applicable in 21 states. Not applicable in states of Delhi, UP, Rajasthan, HP, Uttaranchal, Arunachal Pradesh and Haryana. Rates based on income slabs with deduction not above Rs.2500/- PA. Exemption for certain categories. Multi state operations-PT regn in each of those states. Deduction and deposit frequency may vary as per respective state act.

Maternity Benefit Act 1961: 26 weeks-8 weeks prenatal and 18 weeks postnatal (2017 amendment from 12 weeks) paid leave during maternity period for first two children. Applicable when 10 or more employees and minimum 80 days work by employee in 12 months for eligibility. 12 weeks for more than 2 children and adoption, 2 weeks for tubectomy, 6 weeks for miscarriage and MTP and additional 1 month in case of illness certified by medical practitioner. Creche facility if employee strength above 50.

Gratuity: The Payment of Gratuity Act 1972 is applicable on establishments with 10 or more employees.

Shops & Establishment Act: State Act. Applicability based on coverage of charitable institution within the definition of ‘Establishment/Commercial Establishment’. Regulates working hours, opening closing, holidays, employment of children, leaves including earned leave, OT etc. Need to obtain license and furbish necessary returns.

Apprentices Act 1961: to regulate training in industry/establishment as per a contract for apprenticeship. Establishment with 30 or more workers must engage apprentices in range of 2.5-15% of workforce. Provided stipend during training based on category of apprentice i.e. trade, graduate, technical, vocational based on prescribed benchmarks. Apprentice is not a worker and therefore labor laws not applicable. Reporting requirements for employer.

Sexual harassment of Women at Workplace (Prevention, Prohibition & Redressal) Act 2013: Policy against sexual harassment of women at workplace, it can be gender neutral also, Internal committee (IC) where employee strength exceeds 10, create awareness and visibility of POSH and IC, management facilitate enquiry for POSH matters to IC, Annual reporting by IC to management and district authority if more than 10 employees. POSH compliance in Directors Report for company.

EPF & Misc Provisions Act 1952:

- Inclusion: Employee Provident Fund scheme (EPF) 1952, Employee Pension Scheme (EPS) 1995 and Employee Deposit Linked Insurance Scheme (EDLI), 1976

- Eligibility: All employees (full/part time) working for more than 30 days in a year covered. Once an employee always an employee, once an establishment always an establishment.

- Excluded Employees: employee whose pay is more than Rs. 15,000 a month at the time of joining provided he is not member of EPFO. For coverage of establishment, both coverable and excluded total to be considered. Not available for Newspaper establishment. Employees drawing less than Rs 15,000 per month have to mandatorily be members.

- EPF Scheme: The contribution paid by employer and employee is 12 per cent each of basic wages (including fixed allowances), DA plus retaining allowances. Contribution eligible for 80C benefit and interest is exempt from tax-for FY 24-25 it is 8.25%.

- EPS: Minimum 10 yeas of contributory service or attaining 58 years of age (reduced pension from 50-57 yrs and defer pension beyond 58) and whether in service or superannuated.

- 6 type of pension-superannuation, disabled, widow/child pension, orphan, nominee,

- dependent parents pension/ Pension= Pensionable Salary (average of last 60 months) X

- Pensionable Service)/70. Provide life certificate annually in November of each year

- EDLI: Insurance benefit min 2.5 lakhs upto Rs.7.0 lakhs in case of death while in service to family member/nominee

- 12% employee share to EPF, 12% employer share-8.33% for EPS upto Rs.1250/- per month and remaining plus 3.67% to EPF, EDLI contribution (0.5%) and EPF admin charges (0.5%) paid by employer. Total liability on employer is 13%. Can restrict contribution to Rs.15k i.e. PF wage ceiling for all employees even if comp is more than 15k. Employer share can be restricted to 15k as per law.

- Any organization employing less than 20 employees can opt for voluntary coverage with 10 % Contribution

- Tax on withdrawal of EPF >50k less than 5 years-TDS 10%

- UAN-12 digit for all previous and current memberships

- Final PF withdrawal: Form 19 for EPF made online

- Interest- exempt from tax except for interest on employee contribution exceeding Rs.2.5 lakhs per annum from 1.4.2021

-

EPF Deposit: by employer within 15 days of close of month online and submit ECR which captures both payment and filing. Non deposit by 15th entails interest and penalty. Member will earn interest even if there is default by

employer

-

Various forms for services and all submission online now. E nomination by members mandatory.

-

Deposit in PPF account is not compliance under EPF

-

Non refundable Advance from EPF contribution for various needs permitted

-

HR department should ensure that e KYC of employees (Linking of Aadhar, Mobile Number, Email id, PAN, E- nomination etc.) are complete in the EPFO site.

-

An employee, who has resigned / terminated from the organization should be

exited from the EPF portal within 2 months of last contribution by the employer.

-

In order to avoid mingling of funds for FC and NFC EPF contribution, it is

advisable to generate separate challan for employees paid from FC and NFC

respectively.

-

An individual who joined the Employees' Provident Fund (EPF) scheme after September 1, 2014, cannot open an Employees' Pension Scheme (EPS) account if his/her monthly salary exceeds Rs 15,000. In such cases the complete 12% of share will go to provident fund account.

-

Form-11 to be obtained and kept in employee files for all exempted employees.

-

Register of Wages, Leave, Advances / Loan, Fine to be maintained by the employer.

ESI Act 1948-Compliances

🕟 Eligibility: All the employees (full time/part time) working with the organization for more than 30 days in a year are eligible for ESI Benefits.

💴 Employees earning daily average wage up to Rs.176 are exempted from ESIC contribution. Employer will contribute both shares

💵 As per the rules, in ESI, employee whose ‘gross pay’ is more than Rs 21,000 in a month are not eligible for ESI benefits. Employees drawing less than Rs 21,000 per month have to mandatory become members of the ESI.

💰 Contribution by Employer and Employee: The contribution paid by employer is 3.25 per cent of wages. The employee will contribute 0.75 per cent of wages. Deposit within 15 days of closing of month. Benefits: Medical, Sickness, Maternity Disablement, Dependents, Funeral.

Payment of Gratuity Act 1972

- Eligibility: As per section 4(1) of payment of gratuity Act 1972, gratuity shall be payable to an employee on superannuation, termination, resignation of employment after he has rendered five years (4 years and 240 days) or more. continuous service or on death/disablement due to accident/disease (5 year rule not applicable in such cases)

- Applicable to organization with 10 or more employees in previous 12 months

- Calculation: The gratuity amount depends upon the tenure of service and last drawn salary. Formula: Last drawn salary (basic salary plus dearness allowance) X number of completed years of service X 15/26. Maximum ceiling Rs.20 lakhs

- Due for payment within 30 days, prosecution and penalty for delay.

- Gratuity contribution: 4.81% of basic pay as per employment contract

- As per new Code of Wages 2019, the basic salary of employee cannot be less than 50% of his gross wages.

- Concept of fixed term employee under SS Code would be eligible even if the term is less than 5 years

- Secure gratuity liability through subscribing to group gratuity scheme of LIC or other insurance companies

Comp structure

For inclusion of labour benefits, comp structure is the first step

- The breakdown of salary (CTC/CTO) needs to be formally part of HR policy

- All benefits would be computed based on breakdown of comp

- Attempt should be to extend maximum reasonable benefits and protect take home as win-win situation.

- Ensure compliance of comp structure with laws is crucial

- Extreme care in preparing employment contracts including the comp structure

Budgeting for social security benefits

In charitable organization, it is important that the provisions of mandatory Labour compliances are kept in mind at the time of budgeting itself as it is not feasible for the organization to contribute for these compliances in absence of budget from own funds.

Points to be kept in Mind:

- Minimum Salary budgeted in the project should be Wages defined in Minimum Wages Act of State + 13% of EPF employer share (including administrative charges) + 3.25 % of ESI employer share + 15 days salary for gratuity benefit.

- Example: a field worker to be paid Rs. 8000 per month then the provision for his salary in budget should be Rs. 9,685/-

- Budgeting for grant proposals should be done accordingly

| Monthly Salary | 8,000.00 |

|

Employer Share of EPF 13 % (including admin charges) |

1,040.00 |

| Employer Share of ESI @ 3.25% | 260.00 |

| Gratuity (Monthly) | 385.00 |

| Cost to Organisation | 9,685.00 |

💲 These benefits are not provided by the donors separately in the budget therefore it is advisable that the salary provided in the budget should be on “Cost to Organization” principlele to ensure that these mandatory continuation can be paid.

🤝🏼 However if in exceptional cases it is not possible to provide these benefits to project staffs then their posts should not be included in the “Human Resource” cost.

💰 Instead the same should be budgeted as programme / field implementation cost and such person should be hired on consultancy on TOR basis and their payment should be made on deliverables basis and monthly invoice should be obtained against same.

📂 NO attendance register / leave records etc. should be maintained for these staffs. However for internal monitoring or control purpose separate records may be maintained.

Labour Codes

29 existing labour laws have been consolidated under four new codes, with an intent to amalgamate, simplify and rationalise the relevant provisions of the subsumed laws.

The Code on Wages, 2019

Amends and consolidates the laws relating to wages and bonus.Industrial Relations Code, 2020

Consolidates and amends the laws relating to trade unions, conditions of employment in industrial establishments, investigation and settlement of industrial disputes.The Social Security Code, 2020

Seeks to amend and consolidate the laws relating to social security with the goal to extend social security to everyone in organised, unorganised and any other sectors.Occupational Safety, Health & Working Conditions Code, 2020

Focussed on consolidating and amending the laws regulating the occupational safety, health and working conditions of the persons employed in an establishment.

The Code on Wages, 2019

The Code on Wages, 2019

- The Payment of Wages Act, 1936

- The Minimum Wages Act, 1948

- The Payment of Bonus Act, 1965

- The Equal Remuneration Act, 1976

Key impact areas

- Widened coverage

No wage threshold for employees, definition of employer includes ‘contractor’ and ‘legal representative of deceased employer’, Universal applicability - New definition of ‘wages’

Applicable to all employees; specified exclusions and conditional inclusions specified, cap on benefits in kind - Timeline for full and final settlement

Two days from the date of removal/resignation/retrenchment/dismissal. - Equal treatment of genders

No discrimination on the basis of gender in matters related to wages, recruitment and conditions of work - Payment of wages and deductions

Payment vide cheque, online mode; no unauthorised deductions allowed from the wages. Deduction not more than 50% of wages for specified matters. Wage slip - Floor wage

Central govt. to fix floor wage for different geographical areas and State govt. shall not fix the minimum wages less than the Floor wage. - Payment of Bonus

Appropriate Govt to decide. However, the likelihood of previous provisions to continue.

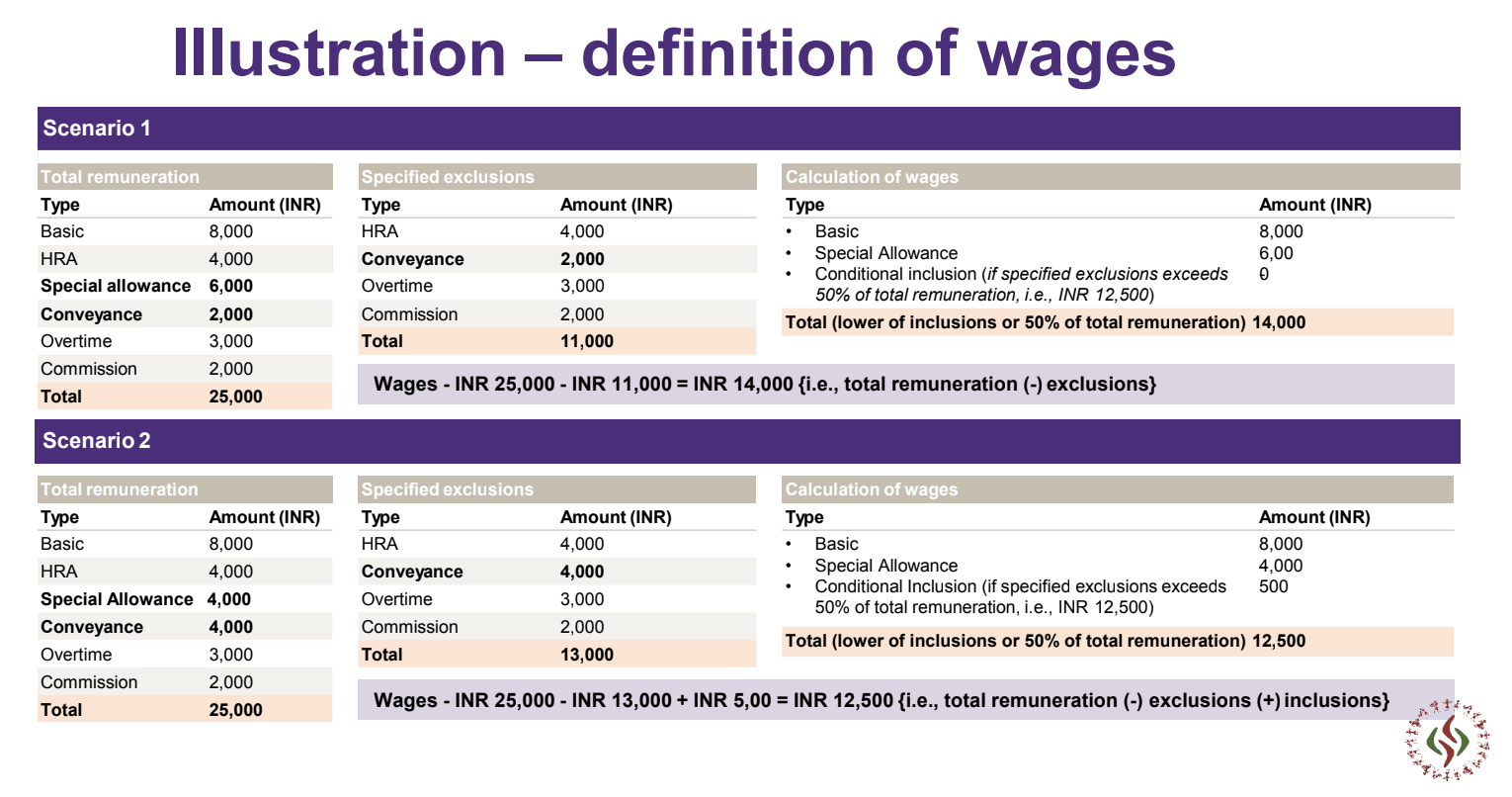

Definition of wages

|

Meaning and inclusions |

Exclusions |

|

Covers all remuneration payable by way of salaries, allowances or otherwise; expressed or capable of being so expressed in terms of money and includes:

|

Specified exclusions (11)

Specified exclusions capped at 50% of total remuneration (except gratuity and retrenchment compensation). |

|

Remuneration in kind to the extent it does not exceed 15% of total wages shall be included in wages. |

|

The Code on Social Security, 2020

Subsumed legislations

- The Payment of Gratuity Act, 1972

- The Employee’s Compensation Act, 1923

- The Employees' State Insurance Act, 1948

- The Employees' Provident Funds and Miscellaneous Provisions Act, 1952

- The Employment Exchanges (Compulsory Notification of Vacancies) Act, 1959

- The Maternity Benefit Act, 1961

- The Cine-Workers Welfare Fund Act, 1981

- The Building and Other Construction Workers' Welfare Cess Act, 1996

- The Unorganised Workers' Social Security Act, 2008

Key impact areas

-

Coverage and registrations: Universal coverage for all working individuals envisaged-unorganised/individual. 20 EPF and 10 ESI Voluntary coverage – opt in/opt out. Limitation introduced as 5 years. ISMW defined.

-

Definition of wages: Wider definition, consistent with definition under Code on Wages, 2019

-

Introduction of new category of beneficiaries: Platform workers, gig workers, fixed-term employees, unorganised workers. 16-60 years, 90 days engagement in 12 months to be registered for SS benefit. Cost increase for aggregators.

-

Increase in quantum of gratuity payment:

-

New category of employees introduced i.e. ‘Fixed term workers’ rendering services for < 5 years versus open contract.

-

Principal employer liable to Gratuity payable to the contract labourers, in case of default by contractor. Gratuity besides PF and ESI.

-

-

Aadhaar Pre-requisite

-

Mandatory for registration, availing benefits.

-

Obligation on International Worker to obtain Aadhaar as per The Aadhar Act, 2016.

-

-

Transition provision: Schemes applicable till one year after Code is implemented, threshold limits to be specified/ notified by central government.

The Occupational Safety, Health and Working Conditions Code, 2020

Subsumed legislations

- The Factories Act, 1948

- The Plantations Labour Act, 1951

- The Mines Act, 1952

- The Working Journalists and other Newspaper Employees (CoS) & M P Act, 1955

- The Contract Labour (R&A) Act, 1970

- The Motor Transport Workers Act, 1961

- The Inter-State Migrant Workmen, Act 1979

- The Working Journalist Act, 1958

- The Beedi and Cigar Workers Act, 1966

- The Sales Promotion Employees Act,1976

- The Cine Workers and Cinema Theatre Workers Act, 1981

- The Dock Workers Act, 1986

- The BOCW Act, 1996

Key impact areas

- Registration and closure

Registration to be applicable if 10 or more workers. - Concept of core and non-core workers

Employment of contract labour in core activities of any establishment is prohibited (with certain exceptions) - Canteen and crèche facility

Mandated for specified establishments - Special provisions for women

Consent of female employees required for working before 6 am and after 7pm along with other safety measures - Leave rules and leave encashment

Workers can ask for encashment of leaves at end of year - Duties of Employees & Employers

Annual Health check up mandated for specified employees of specified establishments - Contractor / ISMW

Registration of contractors if they have 50 or more workers. Liability on principal employer if default by contractor Inter state migrant worker defined-10 or more with wages above Rs.18k per month

The Industrial Relations Code, 2020

Subsumed legislations

The Industrial Relations Code, 2020:

- The Trade Unions Act,1926

- The Industrial Disputes Act,1947

- The Industrial Employment (Standing Orders) Act, 1946

Key impact areas

- Concept of fixed-term employment

Introduced with benefits not be less than of a permanent worker - Conditions for strikes and lockouts prescribed

No strikes and lockouts without giving proper notice in compliance with the norms laid down in the code - Standing orders

Required in establishments where 300 or more workers are employed - Retrenchment, lay-off and closure provisions

Not to be applicable if workers are <300; lay-off related provisions will not be applicable if workers are <50 - Grievance redressal committee mandatory

To be set up where 20 or more workers employed, requires proportionate women representation - Recognition of Trade Unions

All possible efforts have been made in order to provide recognition to the Trade Unions in India. - Re-skilling Fund

Re-Skilling fund for retrenched employee

Please note: Information is for reference only. Read our disclaimer here.

FAQ: Gratuity

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. What is gratuity?

Gratuity is a form of gratitude provided in monetary terms by the employer to the employee for the services rendered by the employee for a period of 5 or more years.

Q2. What are the organisations for which payment of gratuity act is applicable?

Payment of gratuity act, 1972 applies to all shops or establishments having 10 or more employees on any day during the preceding 12 months.

Q3. When are the employees eligible for gratuity?

Employees who have rendered at least 5 years of continuous servicein an organisation are eligible to receive gratuity from the employer.

Q4. When is gratuity payable?

An Organization is liable to pay gratuity to an employee

-

On the termination of his employment after he has rendered continuous service for not less than five years or

-

On his superannuation, or

-

On his retirement or resignation, or

-

On his death or disablement due to accident or disease (the completion of continuous service of five years shall not be considered for the case of death or disablement).

Q5. I have completed 4 years and 245 days of service, am I eligible for gratuity payment?

Yes, in respect of the 5th year, 1 year of completed service = 240 days, therefore you are deemed to have completed 5 years of continuous service if you have completed 250 days of service in the 5th.

Q6. How is gratuity calculated?

Gratuity payable = Last drawn salary *15/26 *No of completed years of service.

Salary for the purpose of the above computation = Basic salary + Dearness allowance

Q7. What is the maximum amount of gratuity that can be paid to an employee?

The amount of gratuity payable to an employee shall not exceed Rs. 20 lakhs.

Q8. Is the gratuity received taxable in the hands of the employee?

In respect of gratuity received by government employees: Entire amount of gratuity is exempt from Income Tax.

In respect of gratuity received by employees other than government employees Amount exempted from tax is

-

20 lakhs (or)

-

Actual gratuity received (or)

-

Last drawn salary *15/26 *No of completed years of service (or)

-

(Whichever is less)

Q9. What is the due date for payment of gratuity?

Gratuity has to be paid within 30 days from the date it becomes payable. (refer FAQ no 4 to know when gratuity becomes payable)

Q10. What is the penalty for default under the Payment of Gratuity Act, 1972?

Any person, for the purpose of avoiding payment of gratuity by making any false statement or false representation:

-

Imprisonment for 6 months or fine up to Rs.10,000 or with both.

An employer, who contravenes or makes default in complying with the provisions of the act:

-

Imprisonment for not less than 3 months and up to 1 year or fine not less than Rs.10,000 but up to Rs.20,000 or with both.

Q11. Is there any interest for delayed payment of gratuity?

In case of employer default:

-

Employer shall pay interest at the simple interest rate (rate notified by the Central Government), from the date on which the gratuity becomes payable to the date till it is paid.

In case of Employee default:

-

No interest shall be payable if the delay in the payment is due to the fault of the employee and the employer has obtained permission in writing from the Controlling Authority for the delayed payment on this ground.

Q12. Whether Gratuity can be allowed as a deduction while calculating taxable income of the employer?

Deduction is allowed only if gratuity is actually paid.

No deduction shall be allowed in respect of any provision made by the assessee for the payment of as per section 40A (7) of the Income tax act, 1961.

Q13. Should the employees under training or apprenticeship be included for the purpose of gratuity?

Yes, irrespective of whether the person is in training or apprenticeship, he is eligible for gratuity, provided he completes a continuous period of 5 years of service

Q14. Does the term continuous service include leaves taken by the employees?

Yes, continuous service includes any leaves, breaks, absence due to any reason, etc.

Q15. Whether the gratuity is to be calculated till the retirement in case of death of an employee?

No, In the case of death of an employee, gratuity is to be calculated only on the completed years of services, not till the retirement.

FAQ: Employees' Provident Fund (EPF)

EPF Scheme 1952

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. Who can be member of EPFO?

A person who is employed for wages in any kind of work, manual or otherwise, in or in, connection with the work of a establishment covered under the Employees’ Provident Funds & Miscellaneous Provisions Act, 1952, and who gets his wages directly or indirectly from the employer, and includes any person employed by or through a contractor in or in connection with the work of the establishment.

Q2. Who can be a member?

An employee of a covered establishment, if not excluded, is compulsorily a member of the employees’ Provident Funds Scheme. The employer of the establishment himself makes the employee a member by following prescribed procedure. An excluded employee is an employee whose pay at the time of being a member exceeds Rs. 15,000/- per month

Q3. Can a member contribute at a higher rate (above 12%) on a voluntary basis?

Yes.

Q4. What is contribution rate payable for a member?

At present, an employee contributes 12% of the Basic wages + Dearness allowance + Retaining allowance in EPF. The employer also pays 12% of pay out of which 8.33% of pay is diverted to Pension Fund and the rest 3.67% is diverted to EPF.

Q5. Does a member contribute to employees’ Pension Scheme and employees’ Deposit-Linked Insurance Fund Scheme (EDLI)?

No. The employer pays 12% out of which 8.33% is diverted to the Pension Fund. An employer also pays 0.5% of Pay in EDLI Scheme.

Q6. What are the benefits available to EPF members?

-

Advances: A member can take non-refundable advances during service period for various purposes:-

-

Treatment of illnesses of self/family: TB, leprosy, paralysis, cancer, mental derangement heart ailment, pandemic or major surgical operation

-

Marriage of self, daughter, son, brother & sister.

-

Post-matriculation education of son/daughter

-

Withdrawal for purchase of house, flat, dwelling house, addition/alteration of house and repayment of loan for the purpose.

-

Withdrawal within one year before retirement: Upto 90% of total PF balance.

-

Advance on unemployment: Upto 75% of total PF balance.

-

- Final settlement: On retirement or two months after ceasing to be an employee.

-

Pension after retirement subject to the eligibility

-

Insurance in case of death while in service.

Q7. What are the other facilities available for a member?

-

Member portal: EPFO provides UAN based online account of member data on EPF website secured with login password.

-

Passbook: for updated balance

-

Online claim filing: A member can file online EPF claims for various benefits through member portal if the EPF account is seeded with Aadhar, PAN & Bank account.

-

Online filing of transfer claim from previous account to new EPF account in case of job change from one covered EPF establishment to another EPF Covered establishment.

-

Modified Declaration form (Form No-11) for automatic transfer of Funds: Members can effect transfer of EPF Fund from previous account to new account without transfer claim if both accounts are linked with UAN and Aadhar seeded.

Q8. Which forms to be filled for claiming benefits?

-

For Final settlement/Withdrawal benefits/Advances: Composite Claim form (Aadhar/non-Aadhar)

-

Scheme certificate: Form 10C

-

For pension: Form 10D

-

For transfer of previous account balance to new account: Form 13

-

For nomination of family members: Form 2

-

Declaration of previous service: form 11

Q9. How to Update Bank account?

A member can update his bank account through a member portal which is then approved by the employer.

Q10. How much time is taken to settle a claim?

As per EPF Scheme, a claim is required to be settled within 20 days.

Q11. What is KYC?

KYC (Know Your Customer) is a member's data updation to improve the services of EPFO for members. These KYC details include PAN, Aadhaar and Bank Account details.

Q12. What are the benefits of KYC?

Claim can be submitted through online mode without attestation of the employer. A member can view his monthly contribution statement by logging on the UAN portal.

Q13 How do I apply for correction in KYC/members’ details?

In order to update or change in KYC (Know your customer) detail on UAN EPFO portal, a member requires UAN (Universal Account Number). Members can login to EPFO UAN portal and update KYC by uploading necessary documents online. Online request for correction in name, date of birth and gender has been introduced.

Q14. How can I update KYC?

Members can update KYC details online in EPFO’s UAN Portal.

Q15. What is UAN?

UAN (Universal Account Number) is a unique 12 digit number allotted to a member. It is a permanent number and remains valid throughout the life of a member. It does not change with the change of employment. UAN helps in automatic transfer of Funds and PF withdrawals.

Q16. Who can generate UAN and How I can get my UAN?

Your Employer can generate the UAN. In case of change in employment, the previously allotted UAN may be provided to the employer.

Q17. What are the benefits of Aadhaar, PAN & Bank accounts details seeded with UAN ?

-

Member can submit claims through online mode

-

Members can file claims directly without the employer's signature.

Q18. What is an Inoperative Account?

An account is classified as an Inoperative account in which contribution has not been received for 3 years after retirement or permanent migration abroad or in case of death. At present, all accounts will earn interest upto 58 years age of a member.

Q19. How Aadhaar, PAN and Bank Account is seeded with UAN?

Member can seed through Member portal, after UAN is activated by employer.

Q20. Will my inoperative account earn interest?

No. However, at present, all accounts will earn interest upto 58 years of age..

Q21. What should I do if my account becomes inoperative?

If you are still working in an establishment covered under EPF & MP Act, 1952, you should get the amount transferred into your new account either by online or offline mode. If you have retired then you may withdraw the amount.

Q22. Will my withdrawal be subject to deduction of income tax (TDS)?

In case a member withdraws his EPF and has rendered less than 5 years of service and accumulated amount is more than Rs. 50,000/, TDS shall be applicable on the following rates:-

|

Submission of PAN |

Non submission of PAN |

No TDS deducted in case of |

|

If 15G/15H is submitted, no TDS is deducted |

TDS is deducted at Maximum Marginal Rate (34.606%) |

Transfer of Fund |

Q23. How does one file a Nomination form for EPF?

Form No-2 is prescribed under Employees Provident Fund, employees’ Pension Scheme and Employee’s Deposit Link Insurance Scheme for submitting family and nomination details.

Q24. What are the benefits of submitting Form No-2?

In case of a member’s death, the family can get the benefit PF/Pension/Insurance without any delay.

Q25. Is it compulsory to enclose cancelled original cheque with the claim form?

Yes. A cancelled original cheque bearing name of the member, his bank account number and IFS Code of the bank should be printed on the cheque itself.In case, members’s bank account is ‘without cheque-book’ facility, then copy of first page of passbook duly attested by the employer or the bank manager may be enclosed with the claim form.

Q26. Are the payments made through NEFT (National Electronic Funds Transfer)?

All payments are made electronically through NEFT or CBS (Core-Banking Solutions).

Pension Scheme

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. What is the formula for calculating the Pension amount?

Pension = (Pensionable Salary (average of last 60 months) X Pensionable Service)/70.

Q2. What is the quantum of pension a member can get on his superannuation?

A member who joins the Employees’ Pension Scheme 1995 at the age of 23 and superannates at the age of 58, and contributes to the (present) wage ceiling of Rs.15000/- may get about Rs.7500/- as pension if service is 35 years.

(Pensionable Salary X Pensionable Service)/70 = (15000x35)/70 = 7500

Q3. How the average salary is determined for granting pension?

The average salary is determined only for giving the pension to member. It is the average of last 60 months. (Non-contributory period, if any, is reduced)

Q4. At what age a member is eligible for pension?

A member is eligible for pension on superannuation at the age of 58 years. If a member leaves employment between 50 and 57 years he can avail the early (reduced) pension.

Q5. In case the employer has failed to pay the pension contribution whether any pension is payable or not?

Non-payment of pension contribution by an employer will not affect the grant of Pension. Pension is guaranteed.

Q6. Is there any increase in the pension amount every year?

No.

Q7. When a member avails reduced pension at the age of 50 can he get his full pension on attaining 58 years?

No. Once Pension is sanctioned it cannot be altered.

Q8. Can a member avail pension even while he is in service?

The member who continues in service even after 58 years can avail the Pension from the age of 58. If a pensioner, who has availed the early pension, may take up employment thereafter and in such cases he will not be eligible to join the Pension Scheme. And the 8.33% contribution from Employer side will go towards EPF fund.

Q9. Can I surrender or sell my full pension for getting a lump sum payment?

No.

Q10. What will be the effect of unemployment period under the Pension Scheme?

The unemployment period will be excluded from the actual service. Pension is based on contributory service only.

Q11. In the absence of family members (family here means the family procreated by the member and not the family in which he/she was born) and nominee, to whom the pension is payable?

It is payable to the dependant parents.

Q12. What are the advantages of taking a Scheme Certificate?

1) It facilitates transfer of Pension Accounts when the employment is changed. 2) If the Holder of Scheme Certificate dies the family will get family pension.

Q13. Who is eligible to get a Scheme Certificate?

A member whose service is 10 years or more and not attained the age of 58 years will be mandatorily issued scheme certificate. A member whose service is less than 10 years can avail the Scheme Certificate to carry forward his pension service but it is not mandatory for such member.

Q14. When and to whom the pensioner is to give a life and non-remarriage certificate?

All pensioners drawing pension under Employees’ Pension Scheme, 1995 are required to give a Life/Non-Remarriage Certificate, duly attested by the Bank Manager/Gazetted Officer after 12 months from the month in which the pension was sanctioned or date of submission of last Life certificate. Physical Life Certificate is to be submitted to the Bank through which the pension is being paid. Failure to submit Life Certificate after one year will result in stoppage of pension after 12 months from the date of submission of last Life Certificate or sanction of pension in case of new Pensioners. In place of physical life certificate ‘Digital Life Certificate’ (DLC) has been introduced from the financial years 201516. Now Pensioners can use their Aadhaar number to submit the DLC. The facility to submit DLC is available in ‘Common Service Centers’ (CSCs), branches of Pension Disbursing Banks, ‘Post Offices’ through ‘India Post Payment Banks’ (IPPB) as well as PF offices.

Q15. Whether member can delay the pension beyond 58 years?

Yes, the member has option to delay the pension beyond 58 years: 1) Member can opt for receiving pension after attaining 59 or 60 years of age but pension contribution stops after 58 years. In this scenario quantum of pension is increase by 4% per year beyond 58 years. 2) Member can opt for receiving pension after attaining 59 or 60 years of age but pension contribution continues after 58 years. In such a scenario the quantum of pension shall be higher than the first case cited above.

Q16. In the absence of nomination, how the P.F. amount of a deceased member is paid?

It is payable to the family members in equal shares, under Para 70 (ii) of EPF Scheme, 1952. If there is no eligible family member, it is payable to the person(s) who are legally entitled to it.

Q17. What is the need for giving nomination for pension?

On the death of a Pension member (before receiving the pension), if there is no eligible family member, pension is payable to the nominee.

EDLI Scheme

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. Whether Assurance benefit under EDLI Scheme is payable for death occurring after leaving the service?

No. Admissible only in case of death while in service.

Q2. To whom the EDLI benefit is payable?

EDLI benefit is payable to the persons eligible to receive the EPF dues.

Q3. Whether Assurance Benefit is payable to missing EPF member?

Payment of Assurance Benefit under EDLI Scheme 1976 is only available on the member’s death while in service to the nominees/legal heirs.

Q4. What is the maximum quantum of Assurance benefit?

Currently, the maximum assurance benefit is Rs.600,000/-.

Q5. Member can now check details of employment in multiple establishment using e-Passbook facility?

-

Visit EPFO Website

-

Click on e-Passbook on the right corner

-

Enter UAN, Password & Captcha

-

Click on Service History.

PF contribution

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. Whether an employer can deduct employer’s share of contribution from the wages of employees?

No. It is not permissible. Any such deduction is a criminal offence.

Q2. Can the wages be reduced by the employer on account of payment to the EPF?

Ans : No. It is specifically barred under section-12 of the EPF & MP Act,1952

Q3. Whether the member is entitled for full interest on the belated deposit of PF dues by the employer?

After realising the dues, the PF members will be given full interest for each due month and it will in no way affect the interest due to members on the contributions paid. The employer shall be charged penal interest under section 7Q and penal damages under section 14B of the Act respectively

Q4. An employee is paid subsistence allowance during the period of his suspension. Whether PF contribution is payable on this?

No.

Q5. Can an employee contribute to the EPF after leaving the service?

No. In the absence of wages & Employer no recovery can be affected. Any contribution by the member must be matched with employer’s share of contribution

Q6. The contribution has been recovered from the wages of the employee but the employer had not paid to the EPF. What is the remedy?

The Employees’ PF Organization will invoke penal provisions of the Act to recover the dues from the employer. Complaint can be lodged with Police under section-406/409 of IPC by the EPFO for action against such employers

Q7. What will be the effect of non-payment of PF dues by an employer? Or how a member is affected for non-payment of EPF dues by the employer?

The Provident Fund amount due to the member will be paid only to the extent of the amount realised from the employer.

Q8. Whether an employer can recover any outstanding dues from the PF amount payable to a member?

No. It is totally prohibited.

Q9. What are the measures by which the PF amount is recovered from a defaulting employer?

Attachment of Bank Accounts, Realisation of dues from Debtors, Attachment & Sale of properties, Arrest and Detention of the Employer, Action under Section 406/409 of Indian Penal Code and Section 110 of Criminal Procedure Code, Prosecution under section 14 of the EPF & MP Act,1952

Q10. How a member is informed about the non-payment of contributions recovered from the wages of the employee but not paid to the EPF?

The Annual P.F. Statement of Account/Member Passbook will indicate the amount paid by the employer. The default period in a year is thus made known to the members. In the current scenario if the member has activated her/his UAN the non-payment/payment of contributions can be verified every month through the e-passbook. Currently, members also receive sms on their registered mobile phones on credit of monthly contribution into their PF account.

Q11. Whether the P.F. amount credited to the member can be attached against any liability?

No. The Provident Fund enjoys protection against attachment by any Court also as per the provisions of section 10 of the EPF & MP Act,1952

Q12. When an employer becomes insolvent or when a company is wound up, whether the contributions will be paid in priority over other debts?

Yes.

Q13. When wages are not collected by the member whether the PF can be deducted or not?

The employer, before paying the member his wages, is required to deduct the PF contribution from his wages and pay to the Regional PF Commissioner. As such PF can be deducted

Q14. Can a member pay contribution in excess of the statutory rate of 12%?

Yes. The member can pay voluntary contribution in excess of his normal contribution of 12% of Rs.15000/-. The total contribution i.e., voluntary + mandatory can be up to Rs.15000/- per month. (The employer may restrict his own share to the statutory rate). The member can also contribute on higher wages i.e., >15000/- after getting permission from APFC/RPFC as per the provisions of para-26(6) of the Scheme

Q15. Can a member demand for showing the recovery of contributions from the employer?

Yes. The contribution card of each member in Form 3-A/ECR copy can be demanded from the employer

Q16. How the contract employees are protected and given their P.F. when the contractor is not paying the dues to the principal employer?

It is the duty of the principal employer to ensure that the Contractor discharges his liability. The Principal Employer must allow payment of bills after ensuring that the Contractor has enrolled and complied in respect of all eligible contract employees every month. The Principle Employer can check the remittance and employee name by using the Establishment Search option available in our website www.epfindia.gov.in. The path is OUR SERVICES >> For Employers >> Important Links >> Establishment Search (Also view Remittances and member name). If the Principal Employer ensures that all contract employees activate their Universal Account Number (UAN), then any default by the contractor can be nipped in the bud.

Q17. Can a member refuse to part with the payment of contribution to the Pension Fund?

The Pension contribution is only a diversion from the employer’s share of the Provident Fund. Hence no consent is required from the member and refusal does not arise.

Q18. Whether an employer can stop paying Employees’ Provident Fund contribution in respect of a member who had attained the age of 55 or 60?

No. The Employees’ Provident Fund Contribution should be paid till the date of his leaving the service, irrespective of the age of the member. Employees who ceases to be EPS(pension) member will get Employers 8.33% contribution in PF.

Advances & Withdrawals, Interest, and Settlement of Final Accounts

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Advances & Withdrawals

Q1. Whether provident fund provides for any refundable loan for Housing etc.?

No. But, non-refundable loans for housing is available.

Interest

Q1. What is the method of crediting interest to the P.F. subscribers?

The compound interest is credited on monthly running balance basis at the statutory rate declared for each year.

Q2. Is there any financial loss to EPF members due to the delay in updating of interest in the member passbook?

Updating of member passbook with interest is an entry process. The date on which the interest is entered in the passbook of the member has no actual financial bearing as the interest earned for the year on his monthly running balances is always added to the closing balance of that year and it becomes the opening balance for the next year. Hence, the member does not suffer any financial loss in case there is any delay in updating interest in his passbook. Further, if a member withdraws his EPF dues before the interest is updated in his passbook, in that case also at the time of his claim settlement, the due interest is calculated and paid from the date it becomes due automatically by the system. Hence, there is no financial loss to a member in the mentioned later case also

Settlement of Final Accounts

Q1. In case the PF amount is not settled within 20 days to whom the matter is to be reported?

He can approach the Regional P.F. Commissioner in charge of grievances; file a complaint on the website using the EPFiGMS feature in the section ‘FOR EMPLOYEES’. The url for the grievance page is http://epfigms.gov.in/ or he can appear before the Commissioner in the ‘Nidhi Apke Nikat’ program being conducted on 10th of every month.

Q2. Is there any time limit for withdrawal of Provident Fund dues?

Only in the case of resignation from service (not superannuation) a member has to wait for a period of two months for withdrawal of the PF amount.

Q3. When the employer is not attesting the claim form how to submit the application for withdrawal of provident fund?

It is the duty of the employer to attest the application form. In case of any dispute, the member may attain attestation preferably from the bank in which he has maintained his account and thereafter submit the same to Regional PF Commissioner, explaining the reasons for not obtaining the signature of the employer. The Regional P.F. Commissioner will pursue the matter with the employer wherever necessary. If the member has activated his Universal Account Number and linked his bank account and Aadhaar then he can submit composite claim (Aadhaar) which only requires the signature of the member.

Transfers and Transfer Claims of Employees

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Transfer

Q1. In case of change in employment whether a member can get his PF account transferred?

On change in employment, the member should necessarily get his PF account transferred to his present establishment, duly submitting Form 13(R). A member can submit a claim for transfer online using the member interface at the unified portal.

Q2. If past accumulations are not transferred on cancellation of exemption, how the provident fund amount is paid to the members?

The local RPFC will ensure transfer of securities/cash and arrange for refund of dues to the members.

Q3. How is a PF member informed of the transfer affected?

A copy of Transfer Certificate (Annexure-K) issued to the transferee Regional P.F. Commissioner/P.F. Trust giving full details of the transfer can be requested from the EPF office.

Transfer claims of Employees

Q1. How do I know if I require a PF transfer?

If the member has more than one PF member IDs (MIDs) and the PF amount of these MIDs has not been transferred into the latest MID, member is required to get his PF transferred into his current MID.

Q2. What is the importance of UAN in online transfer of PF?

Universal Account Number (UAN) acts as an umbrella for the multiple Member IDs allotted to an individual by different employers. UAN enables linking of multiple EPF Accounts (Member Id) allotted to a single member. UAN offers a bouquet of services like dynamically updated UAN card, updated PF passbook including all transfer-in details, facility to link previous members’ PF ID with present PF ID, monthly SMS regarding credit of contribution in PF account and facility for auto-triggering transfer request on change of employment.

Q3. What all information needed at the time of applying online PF transfer?

For online PF transfer please ensure following:

-

Employee should have activated his UAN at https://unifiedportal-mem.epfindia.gov.in/memberinterface/portal Mobile number used for activation should also be active as OTP will be sent in this number.

-

Aadhar number, Bank account of employee should have been seeded against the UAN.

-

The date of exit for the previous employment must have been entered. If date of exit is missing kindly follow the process as given in this FAQ for updation of date of exit.

-

The employer should have approved the e-KYC.

-

Only one transfer request against the previous member ID can be accepted.

-

Personal details reflecting under the “Member Profile” must be verified and confirmed before applying

Q4. Whether date of exit for previous Job/employment is mandatory for applying online Transfer? What are the prerequisites for updation of date of exit?

Yes, updation of date of exit of previous job/employment is mandatory for applying online transfer. The date of exit can be updated only after two months of leaving a job. Also, the date of exit can be any date in the month in which the last contribution was made by the previous employer.

-

This facility is based on Aadhaar-based one-time password (OTP). Thus it can only be utilized by those who have activated their UAN and linked their UAN with a verified Aadhaar number and have mobile linked to Aadhar number for receiving the OTP sent for verification

Q5. What is the process to update date of exit?

-

Go to the https://unifiedportal-mem.epfindia.gov.in/memberinterface/ and login using your UAN and password

-

Click on tab “manage" >> click “mark exit". Under the “select employment” dropdown, select the previous PF account number linked to your UAN

-

Enter the date and reason of exit.

-

Then request for an OTP which will be sent to your Aadhaar-linked mobile number.

-

After you enter the OTP, submit the request. It may be noted that once the date of exit is updated, it cannot be changed.

Q6. How do I know/check if my PF amount has been transferred from my previous member IDs to my current member ID?

The member can check this by viewing his passbook. The member must log in to his member unified portal. In the homepage itself the member must go to View > Passbook. Thereafter the member must enter his UAN, password and captcha to login once again. After login the member can view the passbook of all his MIDs. If his PF has been transferred then the same will be shown as a credit entry in this latest passbook. Otherwise all the passbooks of his previous MIDs will show some balance. In such a case the member is advised to submit online transfer claim.

Q7. With the introduction of UAN and its subsequent linking with Aadhar has made UAN unique for a subscriber. It does not change with change of employment. Then why do I have to file transfer claim?

A member whose UAN is seeded and is fully KYC complaint must not file any transfer claim on change of employment. In such a case whenever an employee joins a new job and the first month’s PF contribution is received then a transfer auto trigger is generated. Soon after, the member’s past PF amount gets automatically transferred into his new account. This automatic transfer gets through if not actively stopped by the member.

Q8. After submitting the transfer claim I am getting an option to download the printable Form 13. Do I need to print the same and submit it to the concerned Field Office?

No. If you have filed online transfer claim then there is no need to submit a physical copy.

Q9. How to track the status of online transfer claim?

The Member e-SEWA portal allows the member to track the status of the transfer claim submitted by going to 'Online Services' tab and then to 'Track Claim Status’. Once the claim is submitted the status shown is “Pending with the employer”. If the employer approves transfer request, status of the form changes to - "Accepted by the employer. Pending at Field Office".

Q10. I have 2 different UANs with one MID linked with each. How do I file online transfer claim in this case?

In such a case there is no provision to file online transfer claim. However a physical claim can be filed duly mentioning the previous and present employment details. The physical Form 13(Transfer claim)can be downloaded from https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form13.pdf. The same must be attested by the authorized signatory of either present or previous employer and submitted to the concerned Field Office. In order to avail all the online services after the transfer-in is effected the member is advised to do the KYC of his latest UAN. Thereafter on job change the member must disclose his KYC compliant UAN to his new employer so as to avoid duplicity of UAN number

Q11. I used to work in an exempted establishment. Now I work in an unexempted establishment. How can I file transfer claim?

Employee is required to submit PF Transfer Claim to the Exempted Trust which will enter the transfer details as Annexure K in Unified Portal. The employer will make the online payment against the Annexure K. After due approval by PF office the past amount and service history gets reflected in his current MID passbook.

Q12. What is Annexure K?

Annexure K is a document which mentions the member details, his PF accumulations with interest, service history, Date of Joining and Date of Exit and employment details including past and present MID. This document is required by the Field Office/Trust to effect a transfer in.

Q13. I want to file a PF transfer claim but I do not know if my past employer was exempted or un-exempted. How can I find out?

The member can view the status of any establishment by going to PF establishment search. The member must go to https://www.epfindia.gov.in. Thereafter, go to Our Services> For Employers > Establishment Search (Under head Services). Then the details of the establishment (name or PF Code) can be entered to view the status of the establishment.

Q14. My PF amount got transferred from my previous MID to my present MID. However my Pension amount has not been transferred. What to do?

The pensionary benefits are dependent on the length of service and the average of last wages drawn. It does not depend on the actual amount lying in the Pension Fund Account. Hence this amount is not transferred during change of employment and a mere transfer of past service history makes the member eligible for pension related benefits

Q15. Why to transfer PF with change in job/employment?

-

The provident fund monies are to provide for a source of income (social security) after retirement during old age. To create a sizable savings it is necessary to start saving early and accumulate the corpus by reducing intermittent withdrawals. Hence it is advisable to transfer PF with each job change to reap full benefits of the social security schemes.

-

1. PF transfer lets the past service transferred into the current member ID. If the total service is more than 5 years then TDS is not charged on PF withdrawal. Clubbing of past service may help the member in crossing the 5 year mark thus saving on TDS.

2. Transferring PF amount instead of withdrawing gives the member the benefit of compounding of funds. The compounding effect can be visualized in a way that if a member does not withdraw his PF money on change of job and gets it transferred to his new account then the same money would get doubled in approximately 8 years, assuming EPFO continues to give at least 8.5% interest rate just like it has given in the past so many years.

3. A service of more than 10 years makes the member eligible for pensionary benefits. Transfer of PF accounts ensures that the past services does not get lapsed and continues to get added in the subsequent employment.

Q16. What are the types and modes of PF transfer?

|

S.No. |

Types of PF Transfer |

Mode of Transfer |

|

1. |

Transfer of PF from one un-exempted establishment to another un-exempted establishment. |

Online |

|

2. |

Transfer of PF from exempted establishment to un-exempted establishment. |

Online |

|

3. |

Transfer of PF from un-exempted establishment to exempted establishment. |

Online |

|

4. |

Transfer of PF from exempted establishment to another exempted establishment. |

Offline |

|

5. |

Transfer of EPS only (for EPF exempt members) from un-exempted establishment to un-exempted establishment. |

Online |

TDS on Claims

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. Under which circumstances TDS will be applicable in accordance with the Ministry of Finance Notification G.S.R. 604(E) dated 31.08.2021?

TDS will be applicable in case of PF Final Settlement, transfer claims, on transfer from Exempted establishments to EPFO and vice versa, on transfer from one Trust on another, past accumulations transfer, at the time of annual accounts processing, on back period accounting after accounts for year 2021-22 are processed in accordance with the Ministry of Finance Notification G.S.R. 604(E) dated 31.08.2021 .

Q2. What is the effective date of deduction of TDS in accordance with the Ministry of Finance Notification G.S.R. 604(E) dated 31.08.2021?

It will be effective from 1st day of April, 2022.

Q3. Is there any minimum amount upto which tax is not deducted ?

The threshold limit for contributions for previous year 2021-22 and subsequent previous year is 2,50,000/- for EPF members.

Q4. At what rate TDS will be deducted if PF account is linked with a valid PAN for resident member?

If PF account is linked with a valid PAN, rate of TDS shall be 10 percent. (Ref. section 194 A)

Q5. Whether taxable contribution part will be subject to a separate accounting of interest?

Yes, taxable contribution part will be subject to a separate accounting of interest and maintenance as the closing balance of this part will earn interest next year and will be subject to TDS.

Q6. Whether taxable and non-taxable both parts will be used for withdrawal?

Yes, Withdrawal will be from taxable account thereafter from nontaxable account.

Grievance redressal

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. How do I get my grievances redressed?

A complainant can lodge his/her grievance online on – https://epfigms.gov.in. If the complainant has UAN/Establishment/PPO number then he can directly enter his respective detail and fill his/her grievance category and description of grievance along with uploading supporting documents. Thereafter his grievance is forwarded to the concerned PF office which is linked to its UAN/Establishment/PPO number, If the complainant does not have UAN/Establishment/PPO number then he/she can register his grievance in Others category where he has to fill all the details along with the PF Office to which the grievance pertains. After successfully lodging the grievance a unique registration number is generated and sent on his mobile number or on email id. The complainant can see/check the status/disposal of his grievance on the above mentioned portal through registration number. The EPFiGMS is an interactive portal as the complainant can add additional supporting document pertaining to his grievance and EPFO offices too can ask for documents as well as seek further inputs from the complainant regarding his/her grievance. The EPFiGMS portal also has the provision for seeking feedback from the complainant with respect to quality of redressal of his/her grievance in the form of star ratings.

Q2. What is an Electronic Return cum- challan (ECR)?

Every establishment covered under the EPF & MP Act, 1952 has to electronically file information after close of every wage month regarding the number of employees employed, their UAN, their Gross/EPF/EPS/EDLI wages, contributions under the three Schemes on such wages and the administrative charges due, wage disbursal date, and number of excluded employees and their gross wages. The ECR facility on unified portal allows the employer to perform the above important statutory duty. After creating the above information in the ECR,the employer can use the challan process for payment of the contributions & administrative charges declared by him.

Q3. How can I seed my KYC details with UAN?

-

Login to your EPF account at the unified member portal.

-

Click on the “KYC” option in the “Manage”section.

-

You can select the details(PAN, Bank Account, Aadhar etc)which you want to link with UAN.

-

Fill in the requisite fields.

-

Now click on the “Save”option.

-

Your request will be displayed in “KYC Pending for Approval”.

-

Once employer approves the details the message will be changed to “Digitally approved by the employer”.

-

Once UIDAI confirms your details,“Verified by UIDAI”is displayed against your Aadhaar.

-

You can select the details (BankAccount, PAN, Aadhar, Passport)which you want to link with UAN.

Q4. How can I view/download my passbook?

Login to the UAN Member Portal with your UAN and password. Go to the menu ‘Download’ and select ‘Download Passbook’. A link to download the PDF of this passbook will be provided. .

Q5. How can I view/download my UAN card?

You first need to login with your valid UAN and password. Then go to ‘Download’ Menu and select the option ‘Download UAN Card’. A PDF copy of your UAN card can be downloaded.

FAQ: Shops & Establishment Act

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

The Shop and Establishment Act regulates the shops and commercial establishments operating within the state. Every state has its own Shop and Establishment Act. However, the general provisions of the Act are the same in all states. The Labour Department of the respective states implements the Shop and Establishment Act.

Shops are generally defined under the Act as the premises where the selling of goods take place either by retail or wholesale or where services are rendered to customers. It includes offices, godowns, storerooms and warehouses used in connection with the trade or business.

Commercial establishments are generally defined as a commercial, banking, trading or insurance establishment or administrative service in which persons are employed for office work. It includes a hotel, boarding or eating house, restaurant, cafe, theatre, or other public entertainment or amusement places. However, factories and industries are not covered by the Act and are regulated by the Factories Act, 1948 and Industries (Development and Regulation) Act 1951.

Registration Under The Shop and Establishment Act

The shops and commercial establishments covered under the Act must mandatorily apply for registration under the respective state Act. All establishments and business, including the people working and maintaining a business from home, must obtain a Shop and Establishment Registration Certificate or Shop License (“Certificate”) under the Act.

The proprietors who run a business from home without having any physical store or premises are also required to obtain this Certificate. The proprietors of e-commerce business or online business, or online stores and establishment must register under this Act and obtain the Certificate. Every shop and commercial establishment should register itself under the Act within 30 days of commencement of business.

The Certificate or the Shop License acts as a basic registration/license for the business. This Certificate is produced for obtaining many other business licenses and registrations. It serves as proof of the incorporation of commercial establishment or shops. It is also useful when the proprietor of the business wants to obtain a loan or create a current bank account for the business. Most banks will ask for this Certificate for opening a current bank account.

Regulations Under The Shop and Establishment Act

The Act, among other things, regulates the following matters-

-

Hours of work, annual leave, weekly holidays.

-

Payment of wages and compensation.

-

Prohibition of employment of children.

-

Prohibition of employing women and young persons in the night shift.

-

Enforcement and Inspection.

-

Interval for rest.

-

Opening and closing hours.

-

Record keeping by the employers.

-

Dismissal provisions.

Process For Obtaining Shop and Establishment Registration

The procedure for obtaining the Shop and Establishment Registration Certificate differs from state to state. It can be obtained online or offline.

For obtaining the registration certificate online, the proprietor or owner of the shop or business must log into the respective State Labour Department website. The proprietor or owner must fill the application form for the registration under the Shop and Establishment Act, upload the documents and pay the prescribed fees. The prescribed fees differ from state to state. Once the registration form is approved, the registration certificate will be issued online to the proprietor or owner of the business.

For obtaining the registration certificate offline, the registration application is to be filled and submitted to the Chief Inspector of the concerned area along with the prescribed fees. The Chief Inspector will issue the registration certificate to the owner or proprietor after being satisfied with the correctness of the application.

The registration application form contains the details relating to the name of the employer and establishment, address and category of the establishment, number of employees and other relevant details as required.

Documents Required For Shop And Establishment Registration

The documents required for obtaining the shop and establishment registration certificate is-

-

Shop or Business establishment address proof.

-

ID proof of the proprietor.

-

PAN Card of the proprietor.

-

Details of the employees.

-

Payment challan.

-

Additional business licenses necessary for starting the business, if any.

Validity of Shop And Establishment Registration

The validity and fees of the Shop and Establishment Certificate differs from state to state. Some states provide the Certificate valid for a lifetime, while other states provide the Certificate valid for one to five years. The registration application needs to be renewed before the expiry of the period of registration.

Q1. Is the Shop and Establishment Act applicable for the establishments of the central and state government?

No. The establishments of the central and state government are exempted from all provisions of the Shop and Establishment Act. Thus, the establishments of the central and state government need not obtain the Shop and Establishment Act Registration.

Which entities are required to obtain the Shop and Establishment Act Registration?

Q2. The following entities are required to obtain the Shop and Establishment Act Registration:

-

Retail and wholesale shops

-

Premises where services are rendered to customers including office

-

Workhouse or workplace used for trade or business

-

Theatre or place of public entertainment or amusement

-

Commercial establishment

-

Storeroom, warehouse or godown

-

Restaurant or eating house

-

Residential hotel

Q3. Are the Shop and Establishment Act valid in all states/UTs across India?

Yes, the Shop and Establishment Act applies to the whole country. However, every state/UT has its own act to govern entities falling within the state’s area/boundary. However, the general provisions of the act of all states are similar.

Q4. Does a factory owner need to register under the Shop and Establishment Act?

No, factory owners are not required to register under the Shop and Establishment Act as they are governed by a different Act, i.e. the Factories Act, 1948.

Q5. What are the details that are to be filled in the Shop and Registration Act registration form?

The registration form for the Shop and Establishment Act Certificate contains the following details:

-

Name and address of the establishment

-

Full name of the employer

-

Category of establishment

-

Nature of business

-

Name of the manager

-

Date of establishment commencement

-

Employee details

FAQ: Maternity Benefit Act, 1961

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. Eligibility for Maternity Benefit: For a woman to be eligible to claim Maternity Benefit does the date of delivery have to be minimum 12 months after the date of joining? i.e., Is she required to have a minimum of 80 working days in 12 months of service. Or is she required to have minimum 80 days of service?

Minimum 80 days she has to work during preceding 12 months for claiming the benefit.

Q2. Period of maternity benefit?

26 weeks paid leave for first two children and 12 weeks thereafter.

Q3. Miscarriage: On submission of proof of a natural miscarriage, is the staff member entitled to 42 days of paid Maternity Leave?

As per Section 6 women are entitled for benefits of 26 weeks of which not more than 8 weeks shall precede the date of her expected delivery.

Section 9: In case of miscarriage on production of such proof, be entitled to leave with wages for a period of 6 weeks immediately following the day of her miscarriage.

Section 10: Women will be entitled to the benefits in addition to the period of absence allowed u/s. 6 or as the case may be u/s. 9, to leave with wages at the rate of maternity benefit for a maximum period of one month.

Q4. Proof to be submitted: Is a doctor’s certificate confirming the pregnancy and expected date of delivery sufficient? Is there any other form to be submitted?

Rule 5 where Form Nos. 2, 3, and 4 are required forms and proof required for the same.

Q5. Payment of Maternity Benefit: Are we supposed to pay Maternity Benefit like monthly salary or only after submission of the certificate confirming the date of delivery?

As per Section 6(5), the amount of benefits for the period preceding the date of her expected delivery shall be paid in advance and for the subsequent period shall be paid within 48 hours of production of such proof as may be prescribed.

Q6. Work From Home: Will it be made applicable only from July 1, 2017?

Effective from the date of notification.

Q7. Crèche Facility applicable from July 1, 2017? Does the crèche facility apply to the 50 employees in each branch or company as a whole?

Company as a whole – not a branch. Every establishment having fifty or more employees shall have the facility of créche within such distance as may be prescribed, either separately or along with common facilities.

Q8. Resignation after claiming Maternity Benefit: What are the rights of the employer in the event that a staff member does not resume work after the completion of 26 weeks of Maternity Leave and the option to work from home is not applicable?

There is no restriction about resignation immediately after enjoying the benefits.

Q9.Resignation after realising that she is not eligible to claim Maternity Benefit: Will the employer be held responsible for the independent decision of a woman to resign if she is pregnant but not eligible to claim maternity benefit?

In case of resignation employer is not responsible.

FAQ: Professional Tax

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. What is Professional Tax?

A professional tax is a charge that a state government imposes on anybody who receives revenue in whatever way. Contrary to what the name might imply, professional tax applies to everyone. The list contains all different types of people from all other professions, occupations, callings, employment, and trades.

The professional tax is shown on the payslip's deductions side, the top limit has been established at INR 2,500 per person annually. Professional tax is deductible according to Section 16(iii) of the Income Tax Act of 1961. By this clause, an employee's professional tax payment may be deducted from their gross salary when completing their income tax reports.

Professional tax is a state government tax imposed on anyone who makes money from any profession, trade, or job. Not every state imposes this tax. The only conditions that do not impose this tax are Arunachal Pradesh, Rajasthan, and Haryana. Karnataka, Andhra Pradesh, Madhya Pradesh, West Bengal, Telangana, Maharashtra, Assam, Meghalaya, and Tamil Nadu are a few states that impose this tax.

Q2. Who Collects the Professional Tax?

The states are in charge of professional tax. States impose a direct tax on every person who earns money. Although state governments handle professional tax, not all states collect it from individuals.

The sole body having the authority to enact legislation about income tax is Parliament, as stated in Article 246 of the Indian Constitution. State governments have the power to pass legislation regarding certain taxes, such as the professional tax. States can enact legislation governing this state government tax under Article 276 of the Indian Constitution.

Q3. Eligibility

The following are subject to professional tax:

-

An individual

-

Hindu Undivided Family (HUF)

-

Whether or whether it is incorporated by a company, firm, cooperative society, association of people, or group of people