Risks & Controls for NGOs

Risks and Control

You can read the information below in over 15 languages! Simply use the translation tool in the top-left corner of the screen to select your preferred language, including অসমীয়া, বাংলা, ગુજરાતી, हिन्दी, ಕನ್ನಡ, മലയാളം, मराठी, মৈতৈলোন্, नेपाली, ଓଡ଼ିଆ, ਪੰਜਾਬੀ, संस्कृतम्, தமிழ், తెలుగు, and اُردُو.

Session Layout:

-

Rationale for Risk management

-

Key concepts relating to risk

-

Risk Management Policy

-

Concept of Internal Controls

-

Areas for internal controls in an NGO

Why understand risk management

-

Risks discussed in NGO-funder relationship, idea is how to understand, capture and manage risks on part of NGOs

-

Good risk management is (a) basic to an effective organisation and (b) ensures better delivery of services to the community.

-

Understand risk appetite (willingness to take risk to achieve objectives) and risk tolerance (ability or boundary to take risk) in an organisation. Risk appetite is about “taking risk” and risk tolerance is about “controlling risk”. Risk appetite is at aggregate level while risk tolerance is at activity level.

-

Risk management is how to bridge the gap between risk appetite and tolerance

-

Understand acceptable internal controls

Key Concept:

-

Threat: A danger in the environment, a potential cause of harm. e.g. legislative changes, technology, competition, inflation, globalisation etc

-

Risk: The probability and potential impact on achievement of objectives when encountering a threat.

-

Internal risks: personnel issues, technology issues etc within the organisation.

-

External risks: economic, political, legal, act of God etc. in external environment

-

- Residual Risk: The risk which inevitably remains after all reasonable mitigation measures have been taken.

No organisation is completely free from risks. The environment will always contain risks.

Types of risks facing Organisations

-

Ethical risk: due to unethical behaviour

-

Operational risk: inability to achieve objectives, capacity/competence gaps, financial/funding constraints, access constraints

-

Financial risk: improper financial planning and management

-

Reputational risk: damage to image and reputation

-

Safety risk: accident/illness

-

Security risk: violence/crime

-

Fiduciary risk: corruption/fraud/theft/diversion

-

Legal/compliance risk: violating laws or regulations

-

Information risk: data breach/loss digital risk

-

Competition risk: competitor take your market for goods/services

Key Concepts

-

Risk management/mitigation: Organisational practices, procedures and policies (P&Ps) that reduce the probability of risks being realised and limit harmful consequences.

-

Enterprise/Integrated risk Management (ERM): An organisational management that considers, combines, and prioritises assessed risks in all risk areas (security, fiduciary, operational, informational, and reputational) in order to strategize and implement mitigation measures.

Risk mitigation is risk reduction - it cannot be made zero.

Risk Management Policy - Need

-

Need for a policy-based on donor audits/due diligence by prospective donors

-

Instil a sense of identifying, understanding and addressing risks in the organisation as it grows

-

Create awareness about risk mitigation strategies when faced with risks in our respective areas of work.

-

Staff embrace and own risk management process

-

Act as a tool for governance and control

Risk Management Process

-

Risk universe analysis

-

Risk identification

-

Risk assessment-risk assessment matrix based on likelihood and impact of identified risks

-

Prioritise risks to be taken up for mitigation

-

Risk Response-Risk Registers with Roles and responsibilities of staff

-

Monitoring

-

Reporting

|

Almost Certain |

(5) |

Low |

Medium |

High |

High |

High |

|

Likely |

(4) |

Low |

Low |

Medium |

High |

High |

|

Possible |

(3) |

Low |

Low |

Medium |

Medium |

High |

|

Unlikely |

(2) |

Low |

Low |

Low |

Low |

Medium |

|

Remote |

(1) |

Low |

Low |

Low |

Low |

Low |

|

⬆️ Probability ⬆️ |

(1) |

(2) |

(3) |

(4) |

(5) |

|

|

➡️ Consequence ➡️ |

Insignificant |

Minor |

Moderate |

Major |

Catastrophic |

|

[0-8 = Low; 9-14 = Medium; 15-25 = High]

Internal Controls

Business practices that serve as “checks and balances” on internal stakeholders (staff/key functionaries) and/or external stakeholders (vendors) in order to reduce the risk.

Internal controls are mechanisms or procedures or rules to mitigate or reduce the risks and loss to an acceptable level.

Internal Controls are of 3 types:

-

preventive controls: in place to prevent adverse events

-

detective controls: detect error/problem after it has occurred- internal audits, Reconciliations, physical inventorying

-

Corrective controls-based on error detected

Benefits and Limitations of Internal Controls

|

Benefits |

Limitations |

|

Early warning system |

Collision |

|

Prevents fraud |

Human error |

|

Avoids external audit findings |

Unforeseen circumstances |

|

Avoids statutory and regulatory penalties and actions |

— |

Key Areas of Internal Controls for Charitable Organisations

-

Legal compliance

-

Governance

-

Budget

-

Income

-

Expenditure

-

Purchase/Procurement

-

Human Resource Management

-

Assets/Inventory Management

-

Accounting

-

Cash and Bank

-

Donor Reporting

-

Program Implementation

1. Internal Controls around Legal compliance

Statutory and regulatory compliance-difference

-

All applicable statutory registrations are in order and valid (entity registration, 12AB, 80G, PAN, TAN, FCRA, NGO Darpan, MCA, EPF, ESIC, PT, Shops & Establishments Act etc).

-

All annual/periodic regulatory filings up to date (ITR, TDS, EPF, ESI, PT RoS/ROC etc).

-

Proactively check adverse proceedings/pending matters under various laws.

-

Aware that a statute or rule applies to NPOs.

-

Continued education/awareness/knowledge for changes happening in the statutory and regulatory landscape.

2. Internal Controls around Governance

-

Governance structure as per bye laws/rules

-

Meetings as per bye laws, proceedings documented as minutes of meeting

-

Changes notified & approvals obtained from statutory bodies

-

Board to put in place risk management/mitigation system

-

All statutory and other business as per timeline after proper scrutiny and review

-

Legal action against/violations by board members

-

Section 13 disallowances for transactions with board members

-

Approval of P&Ps and sub committees

3. Internal controls around Budgeting & Budgetary Controls

-

What is a budget?

-

How budget helps organisation in planning and execution of grant projects

-

What is Budgetary Controls-process, periodicity, ownership of program and finance teams

-

Course correction/Budget revision to address deviation/variance (favourable or adverse)

(Note: Participants, we have studied this in detail in the session on Principles of Grant Accounting and Management)

4. Internal controls around Grants and other Incomes

- Grant funds credited in designated Bank account Grant-proper safety and record keeping Treatment of interest

- Periodic grant Reconciliation

- Segregation of duties in Finance

- issuance of money Receipt and donation certificate to donor Timely reporting

- Proper receipt and recording of income other than grants which include rent, interest, incidental business activity etc.

5. Expenditure

Types of Expenditure:

-

Programme Expenditure or Administrative Expenditure

-

Revenue or Capital Expenditure

-

Head Office Expenditure or Field Level Expenditure

Internal Controls around Expenditure:

Expenditure plan aligned with field requirement and project plan Monitoring to prevent misappropriation/excessive spend/fraud Qualified Finance Staff to avoid inaccurate/delay in payments Proper recording of transactions, report and invoices.

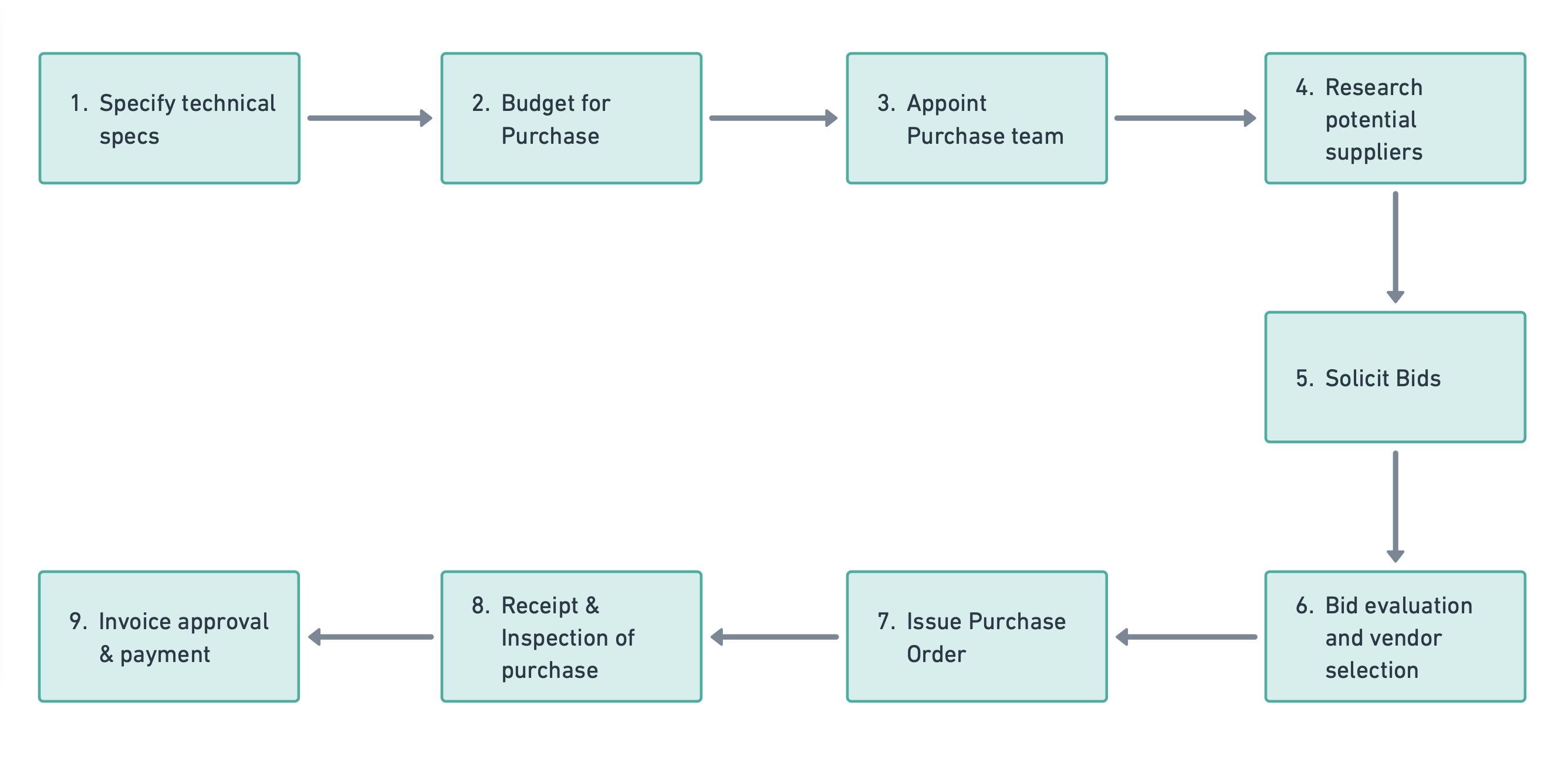

6. Internal Controls around Purchase/Procurement

-

Procurement is the act of buying or obtaining goods/services. It includes preparation and processing of a demand until the end receipt is obtained and payment is approved and released.

-

Procurement process cycle.

Illustrated:

- Specify technical specs

- Budget for Purchase

- Appoint Purchase Team

- Research potential suppliers

- Solicit Bids

- Bid evaluation & vendor selection

- Issue Purchase Order

- Receipt Inspection of purchase

- Invoice approval & payment

Internal Controls around Purchase/Procurement

-

Initiate procurement after checking budget provision

-

Identify vendors after proper assessment.

-

Vendor database

-

Obtaining appropriate bids/tenders

-

Competitive bids for price discovery

-

Proper scrutiny of bids by the PC

-

Terms and conditions in PO/contract

-

Issue of Purchase Orders (PO) by authorised staff only

-

Accurate and complete information in the PO

-

Procurement tracker

7. Human Resource (HR) Management

-

Management of people who work in an organisation is HR Management

-

Need to manage HR

-

For better management of an organisation

-

For better performance and results

-

For better resource mobilisation and funding for the organisation

-

Controls around HR Management

-

HR Planning

-

Recruitment of staff as per JD

-

Proper orientation for new recruits

-

Avoid Nepotism

-

Identification of capacity building needs and training of HR

-

Objective performance appraisal

-

Proper handing over for exiting employee

-

Discontinue access to database for resigned employee

-

Maintaining Employee personal information

-

Salary structure

-

Grievance and complaints redressal mechanism

-

Compliance with social security laws for employees

8. Fixed Assets & Inventory Management

-

FA is an item of economic value which has a life of more than 1 year.

-

Inventory refers to items such as consumables, durables that are normally consumed within a year.

Controls around Fixed Assets & Inventory

-

Asset & Inventory management section in finance policy

-

Indent for assets and consumables based on need and budget

-

Purchase approved by PC and as per grant budgets

-

Specification of assets/inventory captured in PO

-

FA Register, Asset Identification No. marking on assets

-

Stock Register of consumables

-

Annual verification of fixed assets and consumables

-

Assets which are disposed off are removed from FA Register

-

Sale of FC assets

-

Disposal of building, land or higher value assets after Board approval and treatment of CG

9. Internal Controls around Accounting

Accounting is the process of recording, summarising, analysing and reporting financial transactions

Area of internal control in accounting:

-

Compliance with new Rule regarding maintenance of books of accounts

-

Compliance with new Rule regarding maintenance of Other documents

Accounting Software

Controls in accounting:

-

Accuracy

-

Standard formats for recording

-

Evidence and supportings

-

Complete and transparent

-

Audit

10. Controls around Cash and Bank transactions

- Cash is kept in cash box (fixed to wall)

- Reduce cash transaction with online options/universal banking

- Cash Receipts duly signed by receiver and approved

- Cash vouchers are numbered

- Monthly bank reconciliation

- Control on cash withdrawal transactions

- Bank accounts in name of organisation

- Signatories per delegation

- Update KYC of signatories

- Promote online banking

11. Controls around Donor compliances

- Timely and accurate preparation of reports.

- Activities are in line with the activity schedule.

- Data properly collected with reference to objectives of the program.

- Donor reporting guidelines and formats are adhered to.

(Note: Participants refer to the session on Grant Accounting and Management for this area of control)

12. Controls around Program Implementation

- Project Implementation plan carried out as per proposal

- No/ minimal mismatch between LFA and budget

- Impact of adverse events are effectively monitored

- Program implementation is effectively monitored in audit

- Appropriate tools of assessment are used

- Data presentation is properly done

- Outcome of program is properly reported

Please note: Information is for reference only. Read our disclaimer here.

FAQ: ESIC

Key Words and Definitions

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Wages

Q1. How are wages computed for payment of contribution?

The following wage components are taken into account for computation of wages for payment of contribution.

-

Basic Pay/Wages/Salary;

-

D.A/ HRA/ CCA/ Overtime/ officiating allowance/ Night shift allowance/ efficiency allowance/ Heat, Gas, Dust allowance/ Education allowance/ Food & Tea allowance/ conveyance allowance;

-

Wages/ salary/ pay for weekly off and public holidays;

-

Commission paid to sales staff;

-

Subsistence allowance paid to an employee during the period of suspension;

-

Attendance Bonus or incentive or exgratia in lieu of Attendance Bonus or production incentive;

-

Regular Honorarium or salary or remuneration paid to a Director;

-

Collection Bhatta paid to running staff.

-

Actual payments made towards leave salary, lay off compensation, or wages for strike period.

-

Any other remuneration paid or payable in cash to an employee if the terms of contract of employment, expressed or implied were fulfilled.

The above are only indicative.

Q2. What is 'Contribution'?

Contribution is the sum of money payable to the Corporation by the Principal employer in respect of an employee and includes any amount payable by or on behalf of the employee in accordance with the provisions of the Act (Section2(4)).

Q3. What is the Present Rate of Contribution?

- Employer’s contribution: A sum equal to 4.75% of the wages payable to an employee, rounded off to the next higher rupee;

- Employee’s contribution: A sum equal to 1.75% of the wages payable to an employee, rounded to the next higher rupee;

Q4. What is ‘Sickness Benefit'?

If an insured person requires medical treatment and attendance and needs abstention from work on medical grounds, Sickness benefit is paid for the period of abstention duly certified by the Authorized Medical Officer, for a period not exceeding 91 days in two consecutive benefit periods (say one year) @ 70% of standard benefit rate, subject to payment of contribution for not less than 78 days in the corresponding contribution periods.

Q5. What is Extended Sickness Benefits?

This is an additional sickness benefit provided by the Corporation in exercise of its powers under Section 99 of the Act. An insured person who has completed two years of insurable employment and contributed for not less than 156 days during this period is entitled to extended sickness benefit for a period of 309 days for the 34 specified long term diseases. This period can be extended up to 730 days or till the insured person attains the age of 60 years whichever is earlier. The insured person and his family are also entitled to Medical Benefit during this extended period. The daily rate of extended sickness benefit shall be equal to eighty percent of the standard benefit rate.

Q6. What is 'Enhanced Sickness Benefit'?

To promote the norms of small family, this cash benefit is paid to the insured person for undergoing vasectomy/ tubectomy operation. This is paid for a period of 7 days for vasectomy operation and for 14 days for tubectomy operation. This period can be extended in case of any post operative complications. The daily rate of enhanced sickness benefit shall be equal to the standard benefit rate.

Q7. What is Disablement?

Disablement is a condition resulting from employment injury, which may render the insured person temporarily incapable of doing his work and necessitating medical treatment (temporary disablement). It may reduce his earning capacity (permanent partial disability) or it may totally deprive the insured person from the capacity of doing any work (permanent total disability).

Q8. What is 'Employment Injury'?

It is a personal injury to an employee caused by an accident or occupational disease arising out of and in the course of his insurable employment within or outside territorial limits of India.

Q9. What is Occupational Disease?

Contracting any disease, while in employment for a specified period in any of the industries listed in Part A, B, or C of Schedule III to the Act is called Occupational disease. Occupational health hazards can be of two main types. Short term and high dose with acute on set, synonymous with acute poisoning, included by large dose of a toxic substance in an industrial environment, and the other one is chronic on set, which is the result of repeated or continuous exposure of small doses of substances.

Q10. What is 'Temporary Disablement Benefit'?

It is a periodical payment to an insured person suffering from Disablement as a result of 'Employment injury' for the period of abstention from work duly certified by an authorized Medical Officer. This is paid till the temporary disability lasts and the employee is able to resume his normal duties, @ 90% of standard benefit rate.

Q11. What is Permanent Disablement Benefit?

If there is any residual disability of permanent nature due to employment injury, the insured person is examined by a Medical Board to access the loss of earning capacity if any and its percentage. The insured person is paid monthly periodical payments of permanent disablement for life from the date following the date of termination of temporary disablement at that percentage out of full daily rate of disablement benefit. Periodical increase in the benefit is also admissible due to erosion in the cost of living. The benefit can be drawn in cash at the Branch Office, by Money Order at the cost of the Corporation, or credited to the Bank Account of the insured person every month. The insured person can also opt for the payment in lump sum if his daily rate of PDB does not exceed rupees ten or even if it exceeds ten per day, but the commuted value does not exceed Rupees 60000.

Q12. What is Dependants' Benefit?

Dependants' benefit is a monthly pension payable to the eligible dependants of an insured person who dies as a result of an employment injury or occupational disease. The benefit is paid through Branch Offices.

Q13. What is maternity benefit?

Maternity benefit is periodical payments to an insured woman for specified period of abstention from work, due to confinement, miscarriage or sickness out of pregnancy, pre- mature birth of child or miscarriage or confinement. The rate of maternity benefit shall be equal to the standard benefit rate.

Q14. What is confinement? How long is the maternity benefit admissible in case of confinement?

Confinement means labour resulting in the issue of a living child or labour after 26 weeks of pregnancy resulting in the issue of a child whether alive or dead. Maternity benefit is payable for 84 days, subject to payment of contribution for not less than 70 days in the immediately preceding two contribution period. The benefit can be claimed at any time prior to six weeks before the expected date of confinement or from the date of confinement as per the condition and requirement of the insured woman.

Q15. What is 'miscarriage' and how long is the benefit admissible?

'Miscarriage' means the expulsion of the contents of a pregnant uterus at any time prior to or during the 26th week of pregnancy, but does not include a miscarriage, the cause of which is punishable under the Indian penal code. Maternity benefit is payable for miscarriage for a period of 6 weeks (42 days) from the date following the date of miscarriage subject to fulfillment of the contributory condition prescribed.

Q16. What is sickness arising out of pregnancy etc? How long the Maternity benefit is admissible for it?

If the insured woman needs medical treatment and attendance and abstention from work due to sickness arising out of pregnancy, miscarriage, premature child birth or confinement, duly certified by an authorized Medical Officer, Maternity Benefit at is payable for a period one month.

Q17. What is Confinement Expenses?

Confinement Expenses is lump sum payment made to an insured woman or an insured person in respect of his wife for two confinements to meet the confinement expenses, if the confinement occurs at a place where necessary facilities under the ESI Scheme are not available. At present the confinement expenses paid is Rs. 2500/- per confinement.

Q18. What are funeral expenses? Who is to be paid?

A lump sum payment not exceeding Rs. 10000/- towards expenditure on the funeral of a deceased insured person, is paid either to the eldest surviving member of the family or if he has no family or not residing with his family at the time of death, to the person who actually performs the funeral of the deceased insured person.

Q19. What is Standard Benefit Rate?

Means average daily wages obtained by dividing the total wages paid during the contribution period by the number of day for which these wages were paid.

Employer and Employee related

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. What is ESI Scheme?

It is a comprehensive Social Security Scheme designed to accomplish the task of socially protecting the 'employees' in the organized sector against the events of sickness, maternity, disablement and death due to employment injury and to provide medical care to the insured employees and their families.

Q2. How does the scheme help the employees?

The scheme provides full medical care to the employee registered under the scheme during the period of his incapacity for restoration of his health and working capacity. It provides financial assistance to compensate the loss of his/ her wages during the period of his abstention from work due to sickness, maternity and employment injury. The scheme provides medical care to his/her family members also.

Q3. Who administers the ESI Scheme?

The ESI Scheme is administered by a corporate body called the 'Employees' State Insurance Corporation' (ESIC), which has members representing Employers, Employees, the Central Government, State Government, Medical Profession and the Parliament. The Director General is the Chief Executive Officer of the Corporation and is also an ex-officio member of the Corporation.

Q4. How is the Scheme funded?

The ESI scheme is a self financing scheme. The ESI funds are primarily built out of contribution from employers and employees payable monthly at a fixed percentage of wages paid. The State Governments also contribute1/8th share of the cost of Medical Benefit.

Q5. Implemented Area

ESI Scheme is implemented in phases in different part of the country through Gazette notification after making the infrastructure available towards dispensation of medical as well as other benefits provided under the provisions of the Act to the prospective beneficiary.

Q6. What are the establishments that attract coverage under ESI?

According to the notification issued by the appropriate Government (Central/State) concerned under Section 1(5) of the Act, the following establishments employing 10 or more persons attracts ESI coverage.

-

Shops

-

Hotels or restaurants not having any manufacturing activity, but only engaged in 'sales'.

-

Cinemas including preview theatres;

-

Road Motor Transport Establishments;

-

News paper establishments.(that is not covered as factory under Sec.2(12));

-

Private Educational Institutions (those run by individuals, trustees, societies or other organizations and Medical Institutions (including Corporate, Joint Sector, trust, charitable, and private ownership hospitals, nursing homes, diagnostic centers, pathological labs).

In some states coverage is for 20 or more employees for wages. A few State Governments have not extended scheme to Medical & Educational Institutions.

Registration Procedure

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. Is it mandatory for the Employer to register under the scheme?

Yes, it is the statutory responsibility of the employer under Section 2 –A of the Act read with Regulation 10-B, to register their Factory/ Establishment under the ESI Act within 15 days from the date of its applicability to them.

Q2. What is the procedure for Registration of an employer?

The Factory or Establishment to which the Act applies is to be registered by logging into ESIC Portal i.e. www.esic.in The employer is supposed to sign up, providing company name, principle employer’s name, State and region as well as e mail address. The employer trying to register would get a password into his mail id. The employer can log in to www.esic.in and his mail ID can be used as user ID and the password received has to be accessed from the mail box to be used to register his unit by providing information in the Portal. Automatically a 17 digit code number is generated after successful registration.

Q3. What is a Code number?

It is a 17 digit unique identification number allotted to each of the factory/establishment registered under the provisions of the Act. Such a number is generated through ESIC portal on submission of the pertinent information by the employer or generated on receipt of Survey report from the Social Security Officer.

Q4. What is a Sub-code number?

This is also a unique identification number allotted to a sub-unit, branch office, sales office or Registered Office of a covered factory or establishment located in the same State or different State. The employer can register any Branch or Sales Office through ESIC Portal using his credentials.

Q5. Can a factory or establishment once covered go out of coverage if the number of persons employed therein goes down to the minimum limit prescribed?

Once a factory or an Establishment is covered under the Act, it continues to be covered notwithstanding the fact that the number of persons/ coverable employees employed therein at any time falls below the required limit or there is a change in the manufacturing activity.

Q6. Is there any provision for 'exemption of a factory or establishment' from ESI coverage?

Of course exemption is permissible from operation of provisions of the Act subject to the condition that the employees in a factory or establishment covered are other-wise in receipt of benefits substantially similar or superior to those provided under the ESI Act. The appropriate Government may grant exemption to such factory or establishment for a period of one year at a time prospectively in consultation with ESI Corporation. Application for renewal is to be made three months before the date of expiry of the period exemption.

Q7. If the wages of an employee exceeds Rs. 21,000 in a month, can he be treated as not covered and deduction of contribution from his wages is stopped?

If the wages of an employee (excluding remuneration for overtime work) exceeds the wage limit prescribed by the Central Government after the start of the contribution period, he continues to be an employee till the end of that contribution period and hence contribution is to be deducted and paid on the total wages earned by him.

Q8. What is the effect of an increase in wages from a retrospective date?

In case the wages of an employee is increased from a retrospective date resulting in crossing the wage limit prescribed, its effect on coverage of that employee is only after expiry of the Contribution period during the currency of which such increase is announced or declared. The contribution on enhanced wages is also payable from the month in which such increase is announced. There is no need to pay the contribution on the arrears for the period prior to the month of declaration/ announcement/ agreement.

Q9. Why should be paid on the total wages beyond the wage ceiling limit when an employee crosses the wage limit prescribed by the Central Government?

An employee who crosses the prescribed ceiling limit in any month at any time after commencement of the contribution period, he/she would continue to be an employee till the end of that contribution period.

Though there is a ceiling limit of wages for coverage of an employee, there is no ceiling limit in the definition of wages for payment of contribution. Hence, contribution is payable on the total wages without any ceiling limit.

Q10. Is there any provision for exemption from payment of Employer's contribution?

With effect from 1-4-2008, the wage ceiling limit for coverage of employees with disability has been raised to rupees twenty five thousand a month. To encourage the employers for employing more employees with disability, the employer is exempted from payment of Employer's share of contribution on the wages paid to the employees with disability for a maximum period of three years from the date of commencement of the contribution period in which such employee with disability is employed. The Central Government shall reimburse this Employer's contribution to the ESI Corporation.

Q11. What is the time limit for payment of contribution?

Contribution shall be paid in respect of an employee in to a bank duly authorized by the Corporation within 21 days of the last day of the calendar month in which the contribution falls due for any wage period (Reg. 29 & 31).

Q12. What is the manner of working out & payment of contributions?

The employer needs to file monthly contributions online through ESIC portal on a monthly basis in respect of all its employees after duly registering them. Through this exercise, the employer has to file employee wise number of days for which wages paid & the amount of wages paid respectively to ascertain the amount of contributions payable.

The total amount of contribution (both the shares) in respect of all the employees for each month is to be deposited in any branch of SBI in cash or by cheque or demand draft on generation of such a challan through ESIC portal using credentials. Contributions can be paid online through SBI internet banking too.

Q13. What are consequences of non / late payment of employees' contribution deducted but not paid?

Any sum deducted by the Principal employer from wages under the ESI Act shall be deemed to have been entrusted to him by the employee for the purpose of paying the contribution in respect of which it was deducted (Sec. 40(4). Non-payment or delayed payment of the Employee's contribution deducted from the wages of the employee amounts to ' Breach of trust' and is punishable under IPC 406.

Q14. Will the delayed payment attract any interest?

An employer who fails to pay the contribution within the limit prescribed under Regulation 31, shall be liable to pay simple interest at the rate of 12% per annum in respect of each day of default or delay in payment of contribution ( Regulation 31-A).

-

What are the penal provisions for non-payment or delayed payment contribution?

-

The employer is liable for prosecution under Section 85(a) and 85 A of the Act. B.

-

The Corporation may levy and recover damages at the following rates, not exceeding the amount of contribution payable for default or delay in payment of the contribution.

|

Period of delay |

Rate of damages in % p.a. |

|

i) Less than 2 months |

5 % |

|

ii) 2 to 4 months |

10 % |

|

iii) 4 to 6 months |

15 % |

|

iv) 6 months and above |

25 % |

Maintenance of Records and Registration of Employees

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Maintenance of Records

Q1. What are the records to be maintained for ESI purpose?

In addition to the Muster roll, wage record and books of Account maintained under other laws, the employer is required to maintain the following registers for ESI:-

-

Accident Register in new Form-11 and

-

An inspection book.

-

The immediate employer is also required to maintain the Employee's Register for the employees deployed to the principal employer.

Q2. What are the returns/ reports to be submitted by the employer?

- Reports: Accident report in Form 12 in case any accident takes place, to the notice of the Accident.

- Abstention verification report as and when sought by the branch Manager in respect of any IP.

- Records including attendance, wages and books of accounts sought by Social Security Officer on visit to the factory/establishment for inspection with due intimation.

Registration of Employees

Q3. The employees registered under the Scheme?

At the time of joining the insurable employment, an employee is required to provide his and his family details to the employer along with a family photo so that the employer can register the employee online. This exercise of registering an employee has to be a onetime exercise in life time of an employee. The insurance number generated on the first occasion of registration is to be used throughout his life time irrespective of change of employment including change of place.

Q4. What is an identity card?

On registration under the scheme the employer can take a print out of the temporary identity certificate, affix the photo provided by the employee and authenticate it for use which is valid for a period of 3 months. As soon as possible but not later than a month, the insured person along with his entire family should get themselves enrolled to obtain a “Pehchan Card”. This identity card serves as a means of identification both for availing medical benefit at dispensary/ hospital and availing cash benefits at the ESI branch Office. Any changes in his residence/ dispensary/ employment can be carried out by the employer in the Portal as and when arises.

Medical Benefit

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. What is Medical Benefit?

Medical benefit means the medical attendance and treatment to the insured persons covered under the Act and their families as and when needed. This is the only benefit provided in kind through the State Governments (except in Delhi), and uniform to all as per their requirement without linking it to their wages and contributions.

Q2. What is the scale of Medical Benefit?

Full range of Medical, surgical & obstetric treatment consisting of out-door treatment, in- patient treatment, supply of all drugs and dressings, pathological and radiological investigations, prenatal and post-natal care, super specialty consultation & treatment, ambulance services, provision of artificial appliances etc.

Q3. How long is Medical benefit available?

The insured person and his family are entitled to the Medical Benefit from the very first day of his/her joining the insurable employment. A person who is covered under the scheme for the first time is eligible for medical care for self and family for three months. If he/she continues in insurable employment for three months or more, the benefit is admissible till the beginning of the corresponding benefit period. If contributions were paid/ payable for not less than 78 days in the said contribution period, medical benefit is admissible till the end of the corresponding benefit period. If the insured person is in ESI coverage for at least 2 years, and contributed for not less than 156 days, and is suffering from any of the 34 specified long term diseases, the medical benefit is admissible till the incapacity lasts or for a period of 3 years for self and family.

Q4. If the insured person's family is residing in another place in the same State or another State, how the family can avail the medical benefit?

If the family is residing in any other place either in the same State or different State, based on the declaration of the insured person and certified by the employer, the family is provided with a 'family identity card' for receiving medical benefit from ESI Dispensary in the area in which it is residing. After IT rollout, the 'Family' is also issued a separate

'Pehchan card'. By producing this Pehchan card, the family can avail the medical benefit from any ESI Dispensary/ Hospital either at their place of residence or in any other part of the country.

Q5. How to get medical benefit when an insured person is leaving for another station for a temporary period?

Through “Pehchan Card” the employee would get medical benefit across the country in any of the ESIC/ESIS dispensaries subject to entitlement.

Q6. How long is it paid and at what rate?

The rate of dependants' benefit is 90% of standard benefit rate of the wages of the deceased insured person. It is distributed among the dependants as follows: 1) Widow: Till death or remarriage at 3/5th of the full rate. 2) Widowed mother till death @2/5th of the full rate. 3) Sons @2/5th of the full rate each till he attains the age of twenty –five years. 4) Unmarried daughters @2/5th of the full rate till they get married. 5) If the son or daughter is infirm and wholly dependent on the earnings of the insured person at the time of his death, they continue to receive the benefit even after attaining the age of 25 years/ marriage as the case may be. If the total dependants' benefit for all the dependants worked out as above exceeds at any time, the full rate, the share of each of the dependants shall be proportionately reduced, so that the total amount payable to them does not exceed the amountat full rate.

Q7. Whether the TDB/PDB/DB is also admissible in the case of a casual or temporary employee if he meets with an employment injury on the very first day or on any day before he completes his first contribution period?

No qualifying conditions or contributory conditions are attached for payment of temporary disablement benefit, permanent disablement benefit or Dependants benefit. Even if he meets with an employment injury on the very first day of his joining the insurable employment, the benefit is admissible.

Benefit to Family

Q8. What is the benefit admissible to the family members?

- Family members are also entitled to full medical care as and when needed

- The family members are also entitled to artificial limbs, artificial appliances etc. as a part of medical treatment.

- The medical benefit is also admissible to the family during the period the insured person is in receipt of unemployment allowance. In case he dies during the period, his family continues to receive the medical benefit till the end of those twelve months.

- Reimbursement of expenditure incurred on the funeral of the deceased employee.

- In case of the death of the insured employee due to employment injury, the widow, widowed mother and children are entitled to Dependants' benefit.

- Any benefit due to the insured employee at the time of death is paid to the nominee.

Benefit after Retirement to the IPs/WIDOW, etc.

Q9. What is the benefit admissible after retirement of an employee?

An insured person who leaves the insurable employment on attainment of the age of superannuation or retires under a voluntary Retirement Scheme or takes premature retirement, after being an insured person for not less than 5 years, shall be eligible to receive medical benefit for himself and his spouse subject to production of proof thereof, and payment of a nominal contribution of rupees one hundred and twenty for one year. In case the insured person expires, his spouse is entitled to the medical benefit for the remaining period for which the contribution was made, and she can continue to receive the medical benefit on payment of the contribution @ 120/- p.a. for further period.

This medical benefit is also admissible to an insured person who ceases to be in employment on account of permanent disablement caused due to employment injury for himself and his spouse on payment of similar contribution till the date on which he would have vacated the employment on attaining the age of superannuation, had not sustained such permanent disablement.

Further, this medical benefit is also available to widows of insured persons who are in receipt of dependant benefit on payment of contribution as prescribed under rule 60 However, the medical benefit extended under this rule does not include super specialty treatment (SST).

Q10. What is Rajiv Gandhi Sharmik Kalyan Yojana?

In the event of closure of factory/establishment or non-employment injury related unemployment, the insured Person would be entitled to un-employment allowance subject to three years of insurable employment. The un-employment allowance is payable for twelve months in life time.