Labour Codes 2025 (Pacta)

- An overview of the four Labour Codes

- Code on Wages, 2019

- Code on Social Security, 2020

- Industrial Relations Code, 2020

- Occupational Safety, Health and Working Conditions Code, 2020

An overview of the four Labour Codes

This resource was originally created by Pacta. We’re thankful for the time and care they’ve put into making this information accessible.

You can read the information below in over 15 languages! Simply use the translation tool in the top-left corner of the screen to select your preferred language, including অসমীয়া, বাংলা, ગુજરાતી, हिन्दी, ಕನ್ನಡ, മലയാളം, मराठी, মৈতৈলোন্, नेपाली, ଓଡ଼ିଆ, ਪੰਜਾਬੀ, संस्कृतम्, தமிழ், తెలుగు, and اُردُو.

Background

The Labour Codes aim to create a unified and streamlined labour framework by consolidating 29 Central labour laws into four comprehensive codes. Notified on 21 November 2025, they introduce a structured approach to wage regulation, social security, industrial relations, and workplace safety. By doing so, the Codes seek to reduce compliance complexity, clarify obligations for employers, expand worker coverage, and bring greater consistency across labour practices, without positioning any single interest above another.

They comprise:

-

The Code on Wages, 2019 standardises wage definitions and governs minimum wages, floor wages, and payment of wages and bonuses.

-

The Industrial Relations Code, 2020 regulates trade unions, standing orders, industrial disputes, and mechanisms for ensuring industrial peace.

-

The Code on Social Security, 2020 integrates nine social security laws to extend EPF, ESI, gratuity, maternity benefits, and welfare schemes to organised, unorganised, gig, and platform workers.

-

The Occupational Safety, Health and Working Conditions (OSH) Code, 2020 consolidates 13 laws relating to workplace safety, health, welfare standards, working conditions, and protections for migrant and contract workers.

Overview of the four labour codes

1. Code on Wages, 2019

-

Payment of Wages Act, 1936

-

Minimum Wages Act, 1948

-

Payment of Bonus Act, 1965

-

Equal Remuneration Act, 1976

2. Industrial Relations Code, 2020

-

Industrial Disputes Act, 1947

-

Trade Unions Act, 1926

-

Industrial Employment (Standing Orders) Act, 1946

-

Employees' Provident Funds & Miscellaneous Provisions Act, 1952

-

Employees' State Insurance Act, 1948

-

Employees' Compensation Act, 1923

-

Maternity Benefit Act, 1961

-

Payment of Gratuity Act, 1972

-

Cine Workers Welfare Fund Act, 1981

-

Building and Other Construction Workers Welfare Cess Act, 1996

-

Unorganised Workers' Social Security Act, 2008

-

Employment Exchanges (Compulsory Notification of Vacancies) Act, 1959

4. Occupational Safety, Health and Working Conditions (OSH) Code, 2020

-

Factories Act, 1948

-

Mines Act, 1952

-

Dock Workers (Safety, Health and Welfare) Act, 1986

-

Building and Other Construction Workers (Regulation of Employment and Conditions of Service) Act, 1996

-

Plantations Labour Act, 1951

-

Contract Labour (Regulation and Abolition) Act, 1970

-

Inter-State Migrant Workmen (Regulation of Employment and Conditions of Service) Act, 1979

-

Working Journalists and Other Newspaper Employees (Conditions of Service and Miscellaneous Provisions) Act, 1955

-

Working Journalists (Fixation of Rates of Wages) Act, 1958

-

Motor Transport Workers Act, 1961

-

Sales Promotion Employees (Conditions of Service) Act, 1976

-

Beedi and Cigar Workers (Conditions of Employment) Act, 1966

-

Cine Workers and Cinema Theatre Workers (Regulation of Employment) Act, 1981

Compliance checklist

This table outlines all organisational obligations arising after the enactment of the four Labour Codes, including several legal requirements that already existed under the previous statutes. Please also refer to the colour codes used to indicate the specific Acts.

- → Code on Wages, 2019

- → Industrial Relations Code, 2020

- → Code on Social Security, 2020

- → Occupational Safety, Health and Working Conditions (OSHWC) Code, 2020

| Key Themes | Compliance Requirements |

|

Workers/Employees |

|

| Wage Entitlements |

i. Receive at least minimum wages applicable to skill & region. ii. Confirm wages are national floor wage. iii. Check wage slip received monthly. iv. Ensure overtime rate which shall not be less than twice the normal rate of wages. v. Fixed-term employees receive parity in wages & benefits, and gratuity after 1 year. vi. Right to Equal Remuneration (no gender-based discrimination in wages & recruitment). vii. Right to Claim Unpaid Wages / Wrongful Deductions / Bonus. viii. Eligible for bonus 8.33%-20% if below wage ceiling. |

| Social Security Eligibility |

i. Covered under EPF if establishment $\ge$ 20 employees (or voluntary). ii. Covered under ESIC if applicable, check if hazardous occupation. iii. Gig/platform workers registered on National Database. iv. Migrant workers registered for benefit portability. |

Leave & Benefits |

i. Eligible for bonus 8.33%-20% if below wage ceiling |

|

ii. Maternity benefits (women workers): a) 26 weeks paid leave. b) Nursing breaks. c) ₹3,500 medical bonus (if facilities not provided). d) Work-from-home option after childbirth (if agreed). |

|

| Workplace Safety & Welfare |

i. Access to safe workplace & protective equipment. ii. Annual health check-up provided. iii. Crèche facility if establishment has $\ge$ 50 workers. iv. Safety committee present (if thresholds met). v. Right to report accidents including commuting accidents. vi. Women are allowed to work between 6 AM to 7 PM subject to conditions. The Government may also prohibit women from working in certain establishments that could pose danger to their safety and health. |

| Rights & Industrial Relations |

i. 14 days' notice before participating in a strike. ii. Protected from discrimination based on gender/trans identity. iii. Representation in Grievance Redressal Committees (women proportionate to workforce). |

|

Employers |

|

| Wage & Payroll Compliance (Employers) |

i. Ensure "Wages" = minimum 50% of total CTC (cap on exclusions). ii. Pay wages within statutory timelines: a) Daily: end of shift; b) Weekly: before weekly holiday; c) Fortnightly: within 2 days; d) Monthly: within 7 days; e) Termination dues: within 2 days. iii. Issue wage slips every month. iv. Ensure payment to piece-rate workers meets minimum time rate. |

| Organisational Compliance (Employers) |

i. Prepare Standing Orders if workforce $\ge$ 300. ii. Union recognition: if 51% membership $\rightarrow$ negotiate with that union. iii. Maintain digital registers, single annual return, e-records. iv. Use Inspector-cum-Facilitator mechanism for cooperative compliance. v. File for single registration & 5-year unified licence. vi. Maintain registers of wages, deductions, fines, overtime, and bonus, in formats prescribed by rules. vii. Provide wage slips and records electronically, where applicable. viii. Display or provide notices wherever required (e.g., wage rates, working hours, payment dates). |

| Social Security (Employers) |

i. Register employees under EPFO & ESIC as applicable. Register any person before taking him into employment. Registration shall be completed on an online portal (to be specified) through Aadhaar. ii. Ensure ESIC for hazardous occupations regardless of establishment size. iii. Ensure EPF inquiries completed within 2 years (limitation). iv. Provide contribution details transparently to workers. v. Fails to provide insurance to its employee, he shall be liable to pay the exact amount of benefit to the employee is as if the negligence or failure did not occur. vi. Maintain records and register the details, electronically or otherwise, the number of employees, wages, number of days and hours worked, number of leaves, deductions, any accidents or bodily injuries, cess paid, vacancies and other details. |

| Health, Safety & Welfare (Employers) |

i. Conduct risk assessments, exposure monitoring & medical exams. ii. Provide free annual health check-ups. iii. Set up crèche if 50 workers. iv. Establish Safety Committee if thresholds met: a) Factories 500; b) BOCW 250; c) Mines 100. v. Provide protective equipment, safety protocols, emergency drills. vi. Provide uniform and adequate measures by employers for the welfare of employees. It includes hygienic work environment with ventilation, temperature and humidity, sufficient space, drinking water. vii. Ensure suitable and hygienic facilities for washrooms, medical examinations, creches, first-aid boxes, sitting arrangements, canteens, locker rooms etc. viii. Ensure there is an ambulance room in every factory, mine and construction site employing 500 workers or more; and welfare officer in every factory, mine or plantation employing 250 workers or more. |

| Contractor & Migrant Worker Management |

i. Ensure contract labour threshold compliance (now 50). ii. Provide welfare facilities & ensure unpaid wages of contractors are settled. iii. Register & support migrant workers for benefit portability. iv. Ensure journey allowance for inter-state migrant workers. v. Verify that contractors follow minimum wage, payment deadlines, permitted deductions, and bonus rules. vi. Employers can later recover amounts from the contractor but cannot delay payments to workers. |

Gender & Inclusion |

i. No gender or transgender discrimination in employment or wages. |

|

ii. Women allowed night work with safeguards (transport, security). iii. Ensure women representation in advisory & grievance committees. iv. Equal opportunity in hiring, wage rates, and bonus entitlement for men, women, and transgender persons if applicable under rules. |

|

|

v. Provide maternity benefits (26 weeks). |

|

| Disputes & Offences |

i. Respond to improvement notices within 30 days. ii. Compounding procedures (50%-75% of fine) for minor offence. s. iii. Maintain documentation for time-bound dispute mechanisms. iv. Ensure compensation payment from 50% of fines where applicable. |

|

Contractors |

|

| Registration & Licensing |

Registration & Licensing i. Register under the OSHWC Code if employing 50 contract workers. ii. Obtain required contractor licence (now digitised & centralised). iii. Maintain single annual return digitally. |

| Wage & Social Security Compliance |

i. Pay wages at minimum wage or above. ii. Ensure wages comply with the 50% wage structure rule. iii. Provide wage slip or passbook to contract workers. iv. Ensure timely wage payment; employer is liable if contractor defaults. |

|

v. Deposit EPF/ESIC contributions for eligible contract labour. |

|

| Work Conditions & Safety |

i. Provide PPE, safety training & adherence to employer's safety rules. ii. Ensure contract workers are included in workplace safety committees where applicable. iii. Report accidents immediately (including commuting accidents). |

| Inter-State Migrant Workers |

i. Register all migrant workers on portals. ii. Provide journey allowance & ensure portability of benefits. iii. Provide boarding, lodging & helpline awareness. |

|

Worker Rights & Inclusion |

i. No discrimination based on gender or transgender identity. ii. Provide equal wages for equal work. iii. Ensure maternity, overtime & leave benefits are honoured if applicable. |

|

Documentation & Transparency |

i. Maintain records of deployment, attendance, wages, EPF/ESIC. |

|

ii. Share documentation with principal employer for audits. Comply with inspections via inspector-cum-facilitator. |

|

Implementation roadmap of the four labour codes

The table below reflects the new obligations introduced by the Labour Codes however, many of them will come into force only through rules and notifications issued by the Central Government and the respective State Governments. We will continue sharing updates. In the meantime, it is important for organisations to familiarise themselves with the new legal framework so they are prepared, aware, and compliant once the provisions take effect. Please note that the Industrial Relations Code, 2020 does not apply to institutions owned or managed by organisations wholly or substantially engaged in charitable, social, or philanthropic services.

Code on Wages, 2019

| Area | Compliance Requirements |

| Applicability and Regulation | The Code applies to all establishments, employers and employees. Regulates wage and bonus payments in all employments where any industry, trade, business, or manufacture is carried out. |

| Wage Definition | Definition of "wages" include basic pay, dearness allowance and retaining allowance. It does not include bonus, travelling allowance, housing allowance or contributions made to provident fund/pension, gratuity etc.,. |

| Floor Wage | The central government will fix a floor wage, taking into account living standards of workers. Further, it may set different floor wages for different geographical areas. Before fixing the floor wage, the central government may obtain the advice of the Central Advisory Board and may consult with state governments. The minimum wages decided by the central or state governments must be higher than the floor wage. In case the existing minimum wages fixed by the central or state governments are higher than the floor wage, they cannot reduce the minimum wages. |

| Payment of Wage | No employee shall pay less than minimum wages fixed in accordance with Section 9. normal working day shall comprise of eight hours of work with one or more intervals for rest which shall not exceed one hour (in total). In case employees work in excess of a normal working day, they will be entitled to overtime wage, which must be at least twice the normal rate of wages. |

| Wage Period | Wage period for employees shall be either as daily or weekly or fortnightly or monthly subject. |

| Appointment of Committees | Appropriate Committees shall be appointed for revision of Minimum Wages. Revision of pay every 5 years. |

| Registers | Register containing the details of the employees, muster rolls and wages shall be maintained. |

| Penalties |

The Code specifies penalties for offences committed by an employer, such as (i) paying less than the due wages, or (ii) for contravening any provision of the Code. Penalties vary depending on the nature of offence, with the maximum penalty being imprisonment for 3 months along with a fine of up to INR 1,00,000. |

| Inspections | Engage with Inspector-cum-Facilitators for advisory inspections. |

Industrial Relations Code, 2020

| Area | Compliance Requirements |

| Applicability | Applicable to all industrial establishments. Not applicable to establishments which are set up to carry out charitable activities. |

| Works Committee | Works Committee shall be constituted in an Industrial Establishment where more than one hundred workers work. |

| Grievance Redressal Committee | Grievance Redressal Committee shall be constituted in an Industrial Establishment where more than twenty workers work. Ensure women's representation in grievance committees. |

| Formation and Registration of Trade Union | A Trade Union shall be formed and shall be registered by seven or more members of the Trade Union. |

| Industrial Tribunal | The industrial tribunal will consist of two members out of whom one shall be a judicial member, and the other will be an administrative member. |

| Standing Orders | Model Standing Orders for establishments with 300+ workers. Adopt/update. |

| Reskilling Fund | Deposit 15 days' wages per retrenched worker; maintain documentation. |

| Penalties | Penalties are upto INR 2,00,000. In case of non-certification of standing orders, an additional fine of INR 2,000 per day during which the contravention continues. |

| Strikes/Lockouts | Systematise notice periods, track conciliation timelines. |

Code on Social Security, 2020

| Area | Compliance Requirements |

| Applicability |

The Code incorporates a number of social security measures for employees and lays down different thresholds. • For Employees' Provident Fund: Applicable on establishments that employ 20 or more employees. • For Employees' State Insurance: Applicable on establishments (other than a seasonal factory) that employ 10 or more employees. Threshold shall not be applicable if the establishment carries on hazardous or life-threatening occupation. • For Gratuity: Applicable on shops or establishments that employ 10 or more employees. There is no such threshold for factories, mines, oilfield, plantation or railway company. • For Maternity Benefit: Applicable on shops or establishments that employ 10 or more employees. Also applicable on factory, mine, plantation and establishment belonging to government. • For Employees' Compensation: Applicable to employees as mentioned in Second Schedule of the Code. |

| Registrations |

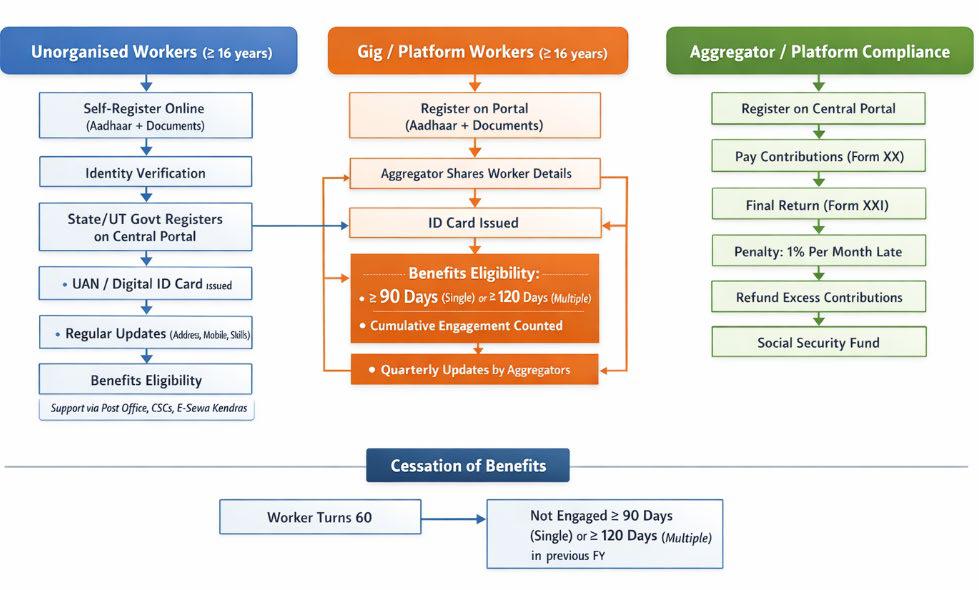

• Register under EPFO/ESIC; maintain digital records. All establishments that are covered under the Act shall apply for registration via Shram Suvidha Portal. If the establishment is already registered under any Central labour law, it shall update the information on the portal. • Registration for Insurance of Employees: An employer, to which obligations under Employees' State Insurance applies, shall register any person before taking him into employment. Registration shall be completed on an online portal (to be specified) through Aadhaar. • Registration of building workers: A building worker, between the age of 18-60 years, who has engaged in any building or other construction work for at least 90 days shall be registered as a beneficiary by the State government or State Building Workers' Welfare Board. • Registration of Unorganised, Gig and Platform Workers: An unorganised/gig/platform worker, who has completed the age of 16 years, shall apply for registration. |

| Aggregator Contributions | Compute and remit 1-2% of turnover (capped at 5% of payouts). |

| Fixed-Term Employees | Provide gratuity after 1 year of continuous service. |

| Maternity & Welfare | Provide maternity benefits, crèches, flexible work where required. |

| Digital Integration | Aadhaar/UAN linking; onboard unorganised workers on e-Shram. |

| Penalties | The Code specifies penalties for offences committed by an employer, such as (i) paying less than the due wages, or (ii) for contravening any provision of the Code. Penalties vary depending on the nature of offence, with the maximum penalty being imprisonment for 3 months along with a fine of up to INR 1,00,000. |

| Inspections | Cooperate with technology-based inspections. |

Occupational Safety, Health and Working Conditions Code, 2020

| Area | Compliance Requirement |

| Applicability | Applicable to all establishments employing 10 or more workers. It will also be applicable to mines and docks even if they employ just one worker. The Code shall not apply to the offices of the Central government, offices of the State government and any ship of war of any nationality. However, within the exception, the Code shall apply in case of contract labour employed through a contractor wherein the Central/State government is the principal employer. |

| Applicability of Part on Contract Labour | Applicable on establishments or manpower supply contractors in which 50 or more contract labour are employed. Not applicable on establishments where work of intermittent or casual nature is performed. |

| Applicability of Part on Inter-State Migrant Workers | Applicable on establishments in which ten or more inter-State migrant workers are employed. |

| Applicability of Part on Mines | The Code is generally applicable on mines. However, the Code is not applicable on: Any mine in which excavation is being made for prospecting purposes only; Any mine engaged in the extraction of kankar, murrum, laterite, boulder, gravel, shingle, ordinary sand, ordinary clay, building stone, slate, road metal, earth, fullers earth and limestone. |

| Applicability of Part on Beedi and Cigar Workers | This Part shall not be applicable to owner or occupier of a private dwelling house where manufacturing process is being carried out with the assistance of the family members. |

| Registration | Employers of all establishments, employing 10 or more employees or any other notified establishment must register within 6 months. Application for registration has to be made in Form II at Shram Suvidha Portal. Documents related to Registration of the establishment; proof of Identity and address of the employer(s) are required for registration. If the establishment is already registered under any central labour law shall update the information on the portal. |

| Registration of Inter-State Migrants | Inter-state migrants have to be registered on an online portal (to be specified) on the basis of self-declaration and Aadhaar. |

| Appointment Letters | Mandatory Letter of Appointment for all workers. |

| Levy of Charge | No Charge should be levied on any employee with regards to maintenance of safety and health of workers. |

| Right to obtain Information | Employee has the Right to obtain information regarding Employee's health and safety at work. |

| Formation of Board | National and State Occupational Safety and Health Advisory Board are constituted to frame Rules and Regulations and implement the provisions of the Code. |

| Work Hours | 8 Hours a day, twice the wages in case of overtime with consent. Overtime wages are payable at twice the ordinary rate of wages. The period of overtime shall be calculated on a daily or weekly basis, whichever is more favourable to the worker. |

| Welfare Facilities | Bathing places, Locker Rooms, Place of keeping clothing, Sitting Arrangement, Canteen, First Aid Boxes, Medical Examinations. |

| Employment of Women | Women shall be employed in all kinds of work and shall be employed before 6 am and beyond 7 pm, only with consent. |

| Contract Labour | Register contractors; ensure welfare; make wage payments if contractor defaults. |

| Safety Systems | Allow third-party audits; implement safety committees for large establishments. |

| Penalties | For contraventions of Code, rules, regulations or by-laws, the employer is liable for a penalty of Rs. 2-3 lakhs. A number of other penalties are prescribed for specific offences. |

Code on Wages, 2019

This resource was originally created by Pacta. We’re thankful for the time and care they’ve put into making this information accessible.

You can read the information below in over 15 languages! Simply use the translation tool in the top-left corner of the screen to select your preferred language, including অসমীয়া, বাংলা, ગુજરાતી, हिन्दी, ಕನ್ನಡ, മലയാളം, मराठी, মৈতৈলোন্, नेपाली, ଓଡ଼ିଆ, ਪੰਜਾਬੀ, संस्कृतम्, தமிழ், తెలుగు, and اُردُو.

Background

The Code on Wages, 2019 is a landmark labour law reform aimed at simplifying and strengthening India’s wage regulation framework. Effective from 21 November 2025, it applies uniformly across sectors and categories of employment, marking a decisive shift towards universal wage regulation. Prior to the enactment of the Code, wage-related matters were governed by multiple central laws, each operating with different definitions, thresholds, and enforcement mechanisms. This fragmented framework often led to ambiguity, uneven application, and exclusion of workers, particularly in the unorganised sector. Drawing from the recommendations of the Second National Commission on Labour and subsequent policy deliberations, the Code on Wages, 2019 was enacted to consolidate and rationalise wage laws, ensure consistency in wage standards, and balance worker welfare with ease of doing business.

Subsumed Laws

-

Payment of Wages Act, 1936

-

Minimum Wages Act, 1948

-

Payment of Bonus Act, 1965

-

Equal Remuneration Act, 1976

Applicability

-

Applies to all establishments, irrespective of size, sector, or nature of operations

-

Covers both organised and unorganised sectors

-

Applicable to:

i. Permanent employees

ii. Fixed-term and contractual workers

iii. Daily wage and piece-rate workers

iv. Other categories of workers recognised under the Code

Key Structural Reforms

-

Introduction of a uniform statutory definition of “wages”

-

Extension of minimum wages to all employments

-

Provision for fixation of a national floor wage

-

Strengthened prohibition on gender-based discrimination in recruitment and wage payment

-

Establishment of a unified, facilitative inspection and compliance mechanism

-

Enhanced focus on transparency, consistency, and ease of compliance

Comparison of Key Legal Provisions between Old Regimes and New Code on Wages, 2019

Table 1: Comparison Of Key Legal Provisions Between Old Laws (Pertaining to Wages) And New Code on Wages, 2019

| Old Regime (Previous Acts) | New Regime (Code on Wages, 2019) | Impact |

|---|---|---|

| Coverage: Restricted to “Scheduled Employments” (approx. 30% of workforce) and specific wage ceilings. | Applies to all employees in all establishments (organised & unorganised), irrespective of wage ceilings or sector. | Expands the compliance universe to cover all categories of workers, including contractual and project-based personnel, reducing ambiguity on applicability. |

| Definition of Wages: Varied across the four different Acts. Led to confusion and litigation regarding what constitutes “basic wage” for PF/Gratuity. | Standardised across all provisions. “Wages” refers to all remuneration payable to an employee for employment or work done, whether described as salary, allowance, or otherwise, and whether paid in money or capable of being expressed in money, provided the employee has fulfilled the terms of employment. | Introduces the “50% Rule” that allowances cannot exceed 50% of total remuneration. (See Box 1). Requires review and possible restructuring of remuneration components to align with the statutory wage definition, with implications for statutory contributions. |

| Minimum Wage: Fixed by States for “Scheduled Employments” only. Rates varied wildly between states for similar work. | The Central Government fixes a “Floor Wage.” State fixed minimum wages cannot be lower than this Floor Wage. | Introduces a uniform minimum wage, improving wage predictability, while potentially increasing payroll costs in lower-wage states. |

| Bonus Eligibility: Applicable at 8.33% - 20% of the salary or wage earned during that year. Payable only to employees earning up to ₹21,000/month and worked at least 30 days in that year. Exempts not for profit organisations from payment of bonus. | Applicable at 8.33% - 20% of annual wage/ salary. Payable to employees who have worked at least 30 days in that year (Wage ceiling for eligibility is to be notified by the appropriate Government.) Exempts not for profit organisations from payment of bonus. | Retention of exemption avoids additional financial burden while maintaining statutory clarity on eligibility thresholds. |

| Gender Discrimination: Limited to “Equal Pay for Equal Work” for men and women. | Prohibits discrimination in recruitment and conditions of employment, not just pay. Includes transgender individuals. | Employers must audit hiring practices, role classification, and pay parity frameworks. |

| Weekly Day of Rest: Required provision of one day of rest in every seven days, with payment of remuneration, subject to applicable rules. | Retains the same requirement to provide one paid day of rest in every period of seven days to employees or specified classes. | Requires uniform scheduling of weekly rest days and ensuring paid rest, impacting workforce planning and wage budgeting. |

| Timeline for Full & Final Settlement: Dismissal/Removal: Within 2 working days. Resignation: No specific timeline (usually paid in the next wage cycle). | Wages must be paid within 2 working days for all separations, such as resignation, dismissal, retrenchment, or closure (See Table 3). | Requires employers to streamline and expedite their exit payroll and settlement process. |

| Inspection: “Labour Inspectors” with a focus on policing and penalties. Physical inspections were common. | “Inspector-cum-Facilitators” Focus on enabling compliance. Inspections can be web-based, randomised, and transparent. | Reduces adversarial enforcement and promotes compliance through guidance and technology-driven oversight. |

| Penalties: Complex mix of fines and imprisonment; often outdated low monetary fines. | Decriminalised for many first-time offenses. Fines are significantly higher, up to ₹50,000 or ₹1 Lakh. Imprisonment is generally reserved for repeat offenders. Compounding of offence is allowed even after the process of prosecution has been initiated. | Shifts the compliance approach from punitive to corrective, encouraging timely rectification while strengthening deterrence for persistent non-compliance. |

Implication of Code on Wages, 2019 for Non-profit Organisations

A. On amount of wages payable:

-

Under the old regime, minimum wages only applied to specific “scheduled employments.” This left large sections of workers uncovered. The new Wages Code extends the right to minimum wages to all employees across all establishments, regardless of the sector or the wage ceiling. The minimum wages are expected to be notified by the state governments from time to time and shall be the wages payable for various types of roles.

-

The States had varied minimum wages under the old regime. Now, the Central Government will fix a “National Floor Wage” based on minimum living standards. State governments cannot fix minimum wages lower than this floor wage. However, this is yet to be notified. Until it is so notified, the existing minimum wages notifications shall apply.

-

The Wages Code also introduces a unified definition of wages. Earlier, various allowances, such as HRA or conveyance, often constituted the bulk of the salary, keeping the basic wage low to reduce Provident Fund (PF) or gratuity liabilities. Under the Wages Code, if “other benefits” exceed 50% of the total remuneration, the excess amount will be added back to the “wages” for calculating social security contributions. The new Code prevents employers from structuring salaries with low basic pay and is likely to have the impact of increasing contributions to PF and gratuity (See Box 1).

-

First non-compliance with provisions on wages would attract fine of INR 50000/-. Hence non-profits must revisit their salary structures and ensure compliance.

Computation of Wages Compliant with Code on Wages

Typical Components Included in Wages

The following elements usually form part of wages:

-

Basic Pay

-

Dearness Allowance (DA)

-

Retaining Allowance, if applicable

Typical Components Excluded from Wages

The following payments are generally excluded from the computation of wages:

a. Statutory or non-contractual bonus not forming part of employment terms

b. Value of house accommodation or amenities such as light, water, medical facilities, or services excluded by government order

c. Employer’s contribution to provident fund or pension, including accrued interest

d. Conveyance allowance or travel concessions

e. Reimbursement of special employment-related expenses

f. House Rent Allowance (HRA)

g. Payments under awards, settlements, or court/tribunal orders

h. Overtime allowance

i. Commission

j. Gratuity payable on termination

k. Retrenchment compensation, retirement benefits, or ex gratia payments on termination

Ceiling on Exclusions (50% Rule)

If the total of payments made under the excluded categories (a to i) exceeds 50% of the total remuneration (or any other percentage notified by the Central Government):

-

The excess amount beyond such limit shall be treated as wages, and

-

This excess will be added back to the wage calculation.

Remuneration in Kind

Where an employee receives remuneration in kind (instead of money, wholly or partly), The value of such remuneration up to 15% of total wages shall be deemed to form part of wages.

Illustration: NPO X employs Ravi as a senior programme manager. His monthly remuneration is:

Basic Pay: ₹25,000

Dearness Allowance (DA): ₹5,000

House Rent Allowance (HRA): ₹30,000 (excluded from wages)

Conveyance Allowance: ₹10,000 (excluded from wages)

Performance Incentive: ₹15,000 (excluded from wages)

Step 1: Total Remuneration

25,000 + 5,000 + 30,000 + 10,000 + 15,000 = ₹85,000Step 2: Total of Excluded Payments

HRA + Conveyance + Incentive = 30,000 + 10,000 + 15,000 = ₹55,000Step 3: Threshold (50% of total remuneration)

50% of 85,000 = ₹42,500Step 4: Excess over threshold

Excluded payments = 55,000 → Threshold = 42,500 → Excess = 55,000 – 42,500 = ₹12,500Step 5: Wages for statutory purposes

Basic + DA + excess excluded payments = 25,000 + 5,000 + 12,500 = ₹42,500Even though Ravi’s total pay is ₹85,000, for statutory purposes like minimum wages, PF, or gratuity calculation, his wages are considered ₹42,500, because the excess of excluded payments over 50% of total remuneration is added back.

B. On bonus and overtime

-

All employees in respect of whom minimum wages are notified are entitled to receive overtime wages at a rate of at least twice the rate of normal wages if they work beyond normal hours. Previously, overtime wage rates varied depending on specific state discretion.

-

It also enforces a strict cap on deductions (PF, ESI, income tax, court orders, cooperative society dues) on pay at 50% of the employee’s total wages in all cases. Earlier, under the Payment of Wages Act, 1936, deductions could go up to 75% for payments to cooperative societies, and 50% in other cases.

C. On record keeping by employer

Table 2 - Statutory Wage & Payroll Registers – Compliance Overview

| Category / Parameter | Requirement / Rule | Illustrative Example / Notes |

|---|---|---|

| Wage Register | Mandatory for all establishments | From date of last entry |

| Wage slips | To be issued to every employee | Digital or physical |

| Fine Register | Required if fines are imposed | Mandatory where applicable |

| Deduction Register | Records all wage deductions | Covers all authorised deductions |

| Overtime Register | Required where overtime applies | Applicable establishments only |

D. On time for wage payment and mode of wage payment

-

The Code mandates that wages be paid timely, by the 7th of the next month, and that a full and final settlement be done within two days of an employee’s resignation or removal.

-

The new Code also recognises the payment of wages through electronic modes, in addition to the traditional coins, currency notes, cheques, and bank credits.

Table 3: Timelines for Payment of Wages Based on Mode of Engagement and Separation

| Basis of Engagement / Situation | Statutory Time Limit for Payment of Wages | Illustrative / Clarificatory Note |

|---|---|---|

| Daily basis employees | At the end of the shift | Wages payable immediately after completion of the shift |

| Weekly basis employees | On the last working day of the week (before the weekly holiday) | Payment to be made prior to the weekly off |

| Fortnightly basis employees | Before the expiry of the second day after the end of the fortnight | Two-day outer limit after the fortnight ends |

| Monthly basis employees | Before the expiry of the seventh day of the succeeding month | Example: October wages payable by 7 November |

| Removal or dismissal from service | Within two working days of removal or dismissal | Final wage settlement within two working days |

| Retrenchment, resignation, or closure of establishment | Within two working days of retrenchment, resignation, or closure | Applies regardless of reason for separation |

Table 4: Permitted Modes of Wage Payment and Compliance Requirement

| Permitted Mode of Wage Payment | Status | Timeline / Condition | Compliance Note |

|---|---|---|---|

| Electronic Transfer (preferred) | Permitted | Ongoing compliance | Direct credit to employee’s bank account with wage slip; digital wage slip encouraged |

| Cash Payment | Permitted with safeguards | During working hours | Payment at workplace with proper documentation |

| Cheque / Demand Draft | Permitted with employee consent | As agreed | Proper records mandatory |

E. On offences and penalties

-

Compounding of offences is a legal mechanism that allows an employer to settle certain non-serious statutory violations by paying the prescribed fine instead of facing prosecution. It is generally permitted only for offences not punishable with imprisonment and is intended to reduce litigation while ensuring regulatory compliance. Earlier, compounding offences was only allowed in certain states. The new Code provides for the compounding of offences which are not punishable by imprisonment, and this is applicable everywhere.

Compounding is only allowed for a sum of 50% of the maximum fine provided for the relevant offence. However, this option is not available to employers who commit an offence for the second time or within a period of five years from either (i) commission of a similar offence which was earlier compounded; or (ii) commission of a similar offence for which such person was earlier convicted.

What lies ahead?

Although the Code on Wages, 2019 has been enacted, its practical operation depends on detailed Central and State notifications. Several critical aspects of day-to-day compliance are yet to be fully notified.

-

Fixation of National Floor Wage by the Government

-

Prescription of daily and weekly working hour limits, beyond which overtime wages will become payable

-

Working hours for certain classes of employees, including those engaged in unforeseen emergency work outside normal working hours as under Section 13(2) of the Code

-

Weekly day of rest and conditions for payment where employees work on rest days

-

Conditions governing intermittent work, emergency work, and employment in specific sectors

-

Determination of normal working day hours, entitlement to a day of rest, and conditions for payment where employees are required to work on rest days

-

Stipulation of the period for preservation and retention of wage and employment records

Pacta will continue to track developments and update this section as and when the Central and State Governments notify the relevant Rules.

Code on Social Security, 2020

This resource was originally created by Pacta. We’re thankful for the time and care they’ve put into making this information accessible.

You can read the information below in over 15 languages! Simply use the translation tool in the top-left corner of the screen to select your preferred language, including অসমীয়া, বাংলা, ગુજરાતી, हिन्दी, ಕನ್ನಡ, മലയാളം, मराठी, মৈতৈলোন্, नेपाली, ଓଡ଼ିଆ, ਪੰਜਾਬੀ, संस्कृतम्, தமிழ், తెలుగు, and اُردُو.

Background

Laws Subsumed under the SS Code

- Employees' Compensation Act, 1923

- Employees' State Insurance Act, 1948

- Employees' Provident Funds and Miscellaneous Provisions Act, 1952

- Employment Exchanges (Compulsory Notification of Vacancies) Act, 1959

- Maternity Benefit Act, 1961

- Payment of Gratuity Act, 1972

- Cine-Workers Welfare Fund Act, 1981

- Building and Other Construction Workers Welfare Cess Act, 1996

- Unorganised Workers' Social Security Act, 2008

Objectives of the SS Code

- Consolidation of Existing Laws: To streamline multiple central labour laws relating to social security into a single comprehensive framework.

- Universalisation of Social Security: To extend social security coverage to all employees and workers, irrespective of whether they belong to the organised or unorganised sector.

- Inclusion of Diverse Categories of Workers: To bring within its ambit self-employed workers, home workers, wage workers, migrant workers, unorganised sector workers, gig workers and platform workers.

- Provision of Comprehensive Benefits: To provide access to schemes relating to life and disability insurance, health and maternity benefits, provident fund, gratuity and other welfare measures.

- Recognition of New Forms of Employment: To acknowledge evolving work arrangements and ensure protection even in non-traditional employment relationships.

- Simplification and Rationalisation of Compliance: To create a uniform and technology-driven framework for registration, contribution and administration of social security schemes.

Comparison of Key Legal Provisions between Old Regimes and Code on Social Security 2020

| Feature | Old Labour Laws | Code on Social Security, 2020 | Impact |

|---|---|---|---|

| Social Security Benefits Accessibility | Earlier, social security benefits were governed by multiple sector-specific statutes such as the EPF Act, 1952, ESI Act, 1948, Payment of Gratuity Act, 1972 and Unorganised Workers' Social Security Act, 2008, with applicability dependent on workforce thresholds, wage ceilings and existence of a traditional employer-employee relationship. | The Code on Social Security, 2020 adopts an expanded and inclusive approach by extending coverage to employees, unorganised workers, gig workers, platform workers and fixed-term employees | Universalisation of social security coverage across workforce |

| Unified Definitions | Under the earlier labour law regime, key terms such as wages, employee, employer and establishment were defined differently across statutes like the EPF Act, ESI Act and Payment of Wages Act, resulting in interpretational inconsistencies | The Code on Social Security, 2020 introduces standardised definitions under Section 2, particularly Section 2(88) for wages, thereby reducing ambiguity and facilitating uniform enforcement. | Reduces litigation and interpretational confusion |

| Definition of Wages | Different definitions across statutes (EPF Act, ESI Act, Payment of Wages Act etc.). Generally included basic wages and certain allowances while excluding HRA, bonus, overtime, commission and several other allowances -- but scope varied under each law leading to litigation. | Uniform definition under Section 2(88). Wages include all remuneration expressed in monetary terms payable to an employee if terms of employment are fulfilled, including basic pay, dearness allowance and retaining allowance. Excludes bonus, HRA, overtime, commission, conveyance allowance and other prescribed exclusions subject to the 50% cap rule (if exclusions exceed 50% of total remuneration, the excess is added back to wages) | Higher contribution base & clarity |

| Unified Social Security Organisations | EPFO, ESIC, Welfare Boards operated independently | Integrated framework with expanded role of National & State Social Security Boards | Better coordination and accountability |

| Digitalisation of Infrastructure | Paper-based compliance; separate forms, registers and inspections | Aadhaar-linked digital records and portability across states and employers | Transparency and portability, especially for migrant workers |

| Worker Facilitation & Grievance Support | No formal system | Toll-free helplines and facilitation centres mandated | Improved accessibility and grievance redressal |

| Compounding of Offences | The compounding of offences was not uniform -- it existed in some Acts but not all, and there was no concept of enhanced punishment for repeat offences. | The SS Code permits the compounding of certain offences (in case of first convictions) in following manner: for an offence punishable with fine only: with payment of 50% of the maximum fine provided for that offence; for an offence punishable with imprisonment for a term which is not more than 1 year and also with fine: with payment of 75% of the maximum fine provided for that offence. Once an offence is compounded, no prosecution will be instituted against the offender for that offence | Encourages compliance |

| Career Centres | Under Employment Exchanges (Compulsory Notification of Vacancies) Act, 1959 (EE Act) private employers employing at least 25 employees were to notify certain vacancies to employment exchanges. Noncompliance with EE Act may lead to a monetary penalty of up to INR 1000. | SS Code introduces concept of career centres replacing employment exchanges. They are offices (including employment exchanges, places, or portals) established and maintained by the Central Government for providing career services by maintaining information on recruiting employers, candidates seeking recruitment, occurrence of vacancies and individuals seeking vocational guidance or counselling to start self-employment etc. Failure to report vacancies (as may be notified by the labour authorities) to career centres may lead to a monetary penalty of up to INR 50,000. | Modern employment services |

| Contribution Flexibility | No provision | Govt may reduce/defer contributions during disasters | Economic relief during crises |

| Employee State Insurance Coverage | Mainly factories and notified establishments | Extendable to wider sectors | Expanded healthcare coverage |

| ESI Registration | Office-centric | Mandatory online registration via portal | Ease of compliance |

| ESI Contributions | Employer 3.25%, Employee 0.75% | Same but digitally tracked, facilitated though Shram Suvidha Portal | Transparency |

| ESI Contribution Revision | Difficult revision | Easier revision via rules | Administrative flexibility |

| Provident Fund Applicability | Applicable to notified establishments with >=20 employees | Applicable establishments with >=20 employees across all types including Gig Workers, Self Employed Workers, FTE etc. | Broader coverage |

| PF Membership Flexibility | No option for small establishments | Establishments with <20 employees may voluntarily join | Increased participation |

| PF Penalties | Up to Rs.5,000 fine and 1-6 months imprisonment | Rs.1,00,000 fine and 1-3 years' imprisonment; repeat offence Rs.3,00,000 or 2-5 years' imprisonment | Stronger enforcement |

| Voluntary PF & ESI Coverage | No provision on the same | PF/ESI chapters may apply on employer application with majority employee consent; exit allowed with conditions | Flexibility for establishments to opt-in/out |

| Gratuity Eligibility | After 5 years continuous service | Includes fixed-term employees and notified events | Expanded employee protection |

| Gratuity Calculation | Standard formula | Pro-rata formula to calculate Gratuity for FTE: (Wages x 15/26 x Pro-rated fraction & completed years of service) | Fair compensation |

| Gratuity Insurance | Not mandatory | Mandatory insurance (except Govt establishments) | Ensures payment security |

| Platform Workers | Not recognised | Introduces the concept of platform workers who undertake 'platform work'. Platform work means any work arrangement outside of a traditional employer employee relationship in which organisations or individuals can use an online platform to access or provide specific services against payment. | Legal recognition of new labour category |

| Aggregators | Not recognised | Defines aggregators in context of gig and platform workers. It states that an aggregator means a digital intermediary or a market-place for a buyer or user of a service to connect with the seller or the service provider | Brings platform economy under regulation |

| Legal Recognition of Gig Work | Not recognised | Separate recognised labour category (gig and platform workers). Gig-worker means a person who performs work or participates in a work arrangement and earns from such activities outside of traditional employer-employee relationship. | |

| Welfare Schemes for Unorganised/Gig Workers | No structured scheme framework | Central & State Governments empowered to frame schemes | Extends protection to informal economy |

| Social Security Fund | No dedicated fund | Separate fund for unorganised, gig and platform workers | Financial security framework |

| Responsibility for Benefits (Unorganised Sector) | Mainly Government | Shared among Govt, aggregators and workers | Shared accountability model |

Implication of The Code on Social Security, 2020 for Not-for-Profit Organisations

A. Employees' Provident Fund

Applicability: The provisions relating to EPF apply to every establishment in which 20 or more employees are employed. The Central Government may also extend coverage to other establishments or classes of establishments through notification. More workplaces and workers will be covered under the Provident Fund system, allowing a larger number of employees to receive social security benefits like retirement savings. Since applicability issue is resolved, it shall reduce litigation.

Voluntary Coverage: Even establishments employing less than 20 employees may opt for PF coverage if there is an agreement between the employer and majority of employees. This promotes wider social security coverage.

Employer Contribution: The employer is liable to contribute 10% of the wages payable to each employee to the Provident Fund. The Central Government may, by notification, enhance this rate to 12% of wages for any establishment or class of establishments. Until the new scheme is introduced, 12% can be followed.

Employee Contribution: The employee is required to contribute an amount equal to the employer's contribution, i.e., 10% of wages. The employee may voluntarily contribute more than 10% of wages. However, the employer is not obligated to match any contribution exceeding the statutory rate.

Key points:

- The Central Government may notify different rates for specific classes of employees.

- Employees may contribute more than the statutory rate (voluntary higher contribution).

- Employers are not required to match contributions beyond the statutory rate.

Pension and Insurance Components: In addition to the Provident Fund Scheme, the Central Government may frame Employees' Pension Scheme (EPS). Provides for:

- Superannuation pension

- Retiring pension

- Permanent total disablement pension

- Widow/widower pension

- Children pension

- Orphan pension

- Nominee pension

Out of the employer's contribution, up to 8.33% of wages (or such percentage as notified) is allocated towards the Pension Fund.

Will your take-home salary reduce under the new labour codes? No not necessarily, if your Provident Fund (PF) contribution is calculated only up to the statutory wage ceiling of Rs.15,000, your take-home salary will remain unchanged. Only when both employer and employee voluntarily agree to contribute PF on wages above Rs.15,000 can the take-home pay change. PF beyond the statutory limit is voluntary. Salary restructuring alone does not automatically reduce take-home pay.

Employees' Deposit Linked Insurance Scheme (EDLI): The Central Government may establish an EDLI Fund. It provides life insurance benefits to employees. The employer contributes up to 1% of wages (or such percentage as notified) towards the Insurance Fund, along with prescribed administrative charges.

Contributions for Contract Workers: Employer can recover PF paid for contract labour from contractor. Contractor can deduct employee contribution from wages. Employer contribution cannot be recovered from employee.

- Is subject to prescribed conditions under the Provident Fund Scheme.

- Cannot be granted if the employer has committed default in payment of contributions or any offence under the Code in the preceding three years.

- May be cancelled if conditions are violated, after giving the employer a reasonable opportunity of being heard.

Transfer of Accounts: Where an employee resigns employment and obtains employment in another establishment, the accumulated amount in the Provident Fund or Pension Fund account shall be transferred or otherwise dealt with in the manner specified in the respective schemes. This ensures continuity of social security benefits.

Exemptions: Establishments registered under the Co-operative Societies law employing less than fifty persons and working without the aid of power; establishments of the Central or State Government whose employees already receive contributory provident fund or old-age pension benefits under government rules; establishments created under any other law where employees are covered by their own provident fund or pension scheme; and employees who were already receiving provident fund benefits under a Central or State enactment before the commencement of the Code. Additionally, the Central Government may exempt any class of establishments for a specified period, subject to conditions, considering their financial position or other relevant circumstances.

Self-Employed Workers: The Central Government may frame schemes for providing social security benefits to self-employed workers or any other class of persons, thereby expanding coverage beyond traditional employer-employee relationships.

Contractor Engagements: The law fixes primary responsibility on the principal employer (the establishment where the work is performed). Accordingly, the principal employer must deposit the entire PF contribution comprising both the employer's share and the employee's share, along with administrative charges with the authorities in the first instance, even though the workers are engaged through a contractor. After making the payment, the principal employer is legally entitled to recover the total amount from the contractor, either by deducting it from the contractor's bills or treating it as a recoverable debt. The contractor may then deduct only the employee's PF contribution from the wages of the concerned worker. The employer's contribution and related charges can never be recovered from the employee, irrespective of any contractual arrangement to the contrary.

Illustration 1

A company engages housekeeping staff through a contractor, each earning Rs.18,000 per month. The total PF payable per worker at 12% employer + 12% employee equals Rs.4,320. The company must first deposit Rs.4,320 with the PF authorities. It may then recover Rs.4,320 from the contractor. The contractor can deduct only Rs.2,160 (employee share) from the worker's salary.

Priority of EPF Dues: Any amount due under the EPF provisions constitutes a first charge on the assets of the establishment and is payable in priority in accordance with the Insolvency and Bankruptcy Code, 2016. This safeguards employees' statutory contributions in cases of insolvency.

Continuity of Existing Schemes and Rules: The following schemes, rules, regulations and procedures framed under the earlier social security legislations shall continue to remain in force for a period of one year from the commencement of the Code to the extent they are not inconsistent with the provisions of the Code on Social Security, 2020:

Schemes under the Employees' Provident Funds and Miscellaneous Provisions Act, 1952:

- Employees' Provident Funds Scheme, 1952

- Employees' Deposit Linked Insurance Scheme, 1976

- Employees' Pension Scheme, 1995

- Tribunal (Procedure) Rules, 1997

Schemes under the Employees' State Insurance Act, 1948:

- All rules, regulations and schemes framed thereunder

These provisions operate as transitional arrangements to ensure administrative continuity and uninterrupted delivery of social security benefits until new schemes are framed under the Code.

Recognition under Income Tax Act: The Provident Fund is deemed to be a Recognised Provident Fund under the Income Tax Act, 1961, thereby ensuring tax benefits subject to statutory limits.

Appeal Mechanism: An employer aggrieved by determination of dues or levy of damages may file an appeal before the prescribed Tribunal, subject to depositing 25% of the amount due as determined.

Penalty: Penalty has been increased from Rs. 10,000 to 1,00,000 and 1 to 3 years imprisonment. Similarly subsequent failure attracts fine of 3,00,000 rupees or 2 to 5 years imprisonment.

B. Gratuity

Applicability: The gratuity provisions apply to: i. Every factory, mine, oilfield, plantation, port and railway company; and ii. Every shop or establishment in which 10 or more employees are employed or were employed on any day in the preceding 12 months; and iii. Any other establishment notified by the appropriate Government.

A key feature of applicability is its continuing nature. Once an establishment becomes covered by virtue of meeting the threshold of ten employees, it remains governed by the gratuity provisions even if the number of employees subsequently falls below ten. Coverage, therefore, is permanent once triggered.

Eligibility: Gratuity becomes payable on termination of employment after continuous service of not less than 5 years in the following cases:

- Superannuation

- Retirement or resignation

- Death or disablement due to accident or disease

- Expiry of fixed-term employment contract

- Any other notified event by Central Government

The five-year qualifying condition does not apply in cases of death, disablement, or expiry of fixed-term employment. In these circumstances, gratuity becomes payable irrespective of length of service.

Continuous Service and Deemed Service Rule: An employee is regarded as being in continuous service if the service is uninterrupted. However, interruptions caused by sickness, accident, leave, lay-off, strike, lock-out, or cessation of work not attributable to the employee do not break continuity. Maternity leave (up to twenty-six weeks) is also included within continuous service.

Even where uninterrupted service cannot be strictly established, the law provides a deeming fiction. Service is treated as continuous if the employee has actually worked for the minimum number of days during the relevant period:

| Period | Minimum Days Worked |

|---|---|

| 12 months | 240 days |

| 6 months | 120 days |

In calculating the number of days actually worked, the following are included:

- Paid leave

- Maternity leave (up to 26 weeks)

- Lay-off days

- Absence due to temporary disablement arising out of employment injury

This deeming rule ensures that employees are not deprived of gratuity due to technical breaks in service.

Will your gratuity increase because of bonuses and perks?

Included in Wages: Basic pay, Dearness allowance, Retaining allowance

NOT Included in Wages (excluded while computing gratuity): performance bonus, stock options, reimbursements, meal vouchers, telephone reimbursement, creche allowance

Calculation of Gratuity: Gratuity is calculated at the rate of fifteen days' wages for every completed year of service or part thereof exceeding six months. For monthly-rated employees, the formula is:

Gratuity = (Last Drawn Monthly Wages / 26) x 15 x Years of Service

The calculation is based on last drawn wages. The total amount payable is subject to the maximum ceiling notified by the Central Government.

Special Cases:

- Piece-rated employees: Daily wages are computed based on the average wages of the preceding three months (excluding overtime).

- Seasonal establishments: Gratuity is payable at the rate of seven days' wages per season.

- Pre-disablement wages: The wages the employee received before becoming disabled are considered at their actual full amount. This ensures that the employee's service prior to disablement is fully recognised in the gratuity calculation.

- Post-disablement wages: Any wages received after the disablement, which may be reduced due to inability to perform full duties, are taken as actually paid, i.e., the reduced rate. This reflects the real earnings of the employee after the accident or disablement, avoiding overpayment relative to current work capability.

Fixed-Term Employees (FTE): Gratuity is payable to fixed-term employees upon expiry of their contract. Unlike permanent employees, fixed-term employees are eligible after completion of at least one year of service, and the five-year requirement does not apply. The method of computation also differs. For permanent employees, service beyond six months is rounded up and treated as one full year. For fixed-term employees, gratuity is calculated strictly on a proportional basis without rounding off. For example, a service period of 2 years and 7 months is treated as 2.58 years, not 3 years.

Gratuity = (Last Drawn Monthly Wages / 26) x 15 x Years of Service

Does gratuity eligibility start after one year of service for all employees? The reduced eligibility period of one year is a special statutory benefit introduced only for Fixed-Term Employees engaged for a defined contractual period. Permanent employees continue to be governed by the traditional five-year continuous service requirement for gratuity eligibility.

Payment on Death: When an employee dies, gratuity is paid to the nominee. If no nomination has been made, it is paid to the legal heirs. If the nominee or heir is a minor, the minor's share must be deposited with the competent authority and invested until the minor attains majority.

Nomination: Nomination is mandatory after completion of one year of service. If the employee has a family, nomination must be made in favour of one or more family members. The nomination may be modified at any time. Employers are required to maintain nominations safely and securely.

Application for Gratuity: Any eligible employee, or a person authorised in writing on their behalf, can submit a written application to the employer for gratuity payment. The form and timeline for submission are as prescribed by the appropriate Government. Key point: While employees can apply, this is not mandatory for the employer to act.

Employer's Duty to Determine Gratuity: As soon as gratuity becomes payable, the employer must:

- Determine the amount of gratuity due.

- Give written notice to the employee (or person entitled) and to the competent authority.

Payment must be made within 30 days from the date gratuity is due. Employers cannot delay payment just because the employee has not applied. Gratuity is automatically due once eligibility criteria are met. If there is a delay, interest becomes automatically payable for the period of delay. Financial constraints, internal administrative approvals, or pending misconduct inquiries are not valid grounds for withholding payment once gratuity has become due.

Interest on Delay: If the employer delays beyond 30 days, they must pay simple interest on the unpaid gratuity. No interest if delay is caused by employee's fault, and employer has obtained written permission from the competent authority.

Forfeiture of Gratuity: Gratuity may be forfeited to the extent of damage or loss caused to the employer's property due to the employee's wilful act or negligence. It may also be wholly or partially forfeited if termination is on account of:

- Riotous or violent conduct; or

- An offence involving moral turpitude committed in the course of employment.

Forfeiture is therefore limited to serious misconduct and is not applicable to ordinary termination.

Compulsory Insurance or Gratuity Fund: It is mandatory for employers (except government establishments) to secure their gratuity liability either through insurance from an IRDAI-regulated company or by establishing an approved gratuity fund. Employers who fail to pay premiums or contributions remain liable to pay gratuity immediately, including interest for delays. Registration with the Authority is also necessary. This ensures that employees receive their gratuity even if the employer defaults, and the government notifications are required to define the specific procedures, forms, and management rules for effective implementation.

Employers cannot casually reject gratuity. Payment becomes automatically due once eligible, regardless of whether the employee applies. If an employer unjustifiably denies or delays payment, the employee can approach the Competent Authority, which can order full payment with mandatory interest. Non-compliance can attract a fine of up to Rs.50,000, and wilful defiance of the authority's order may lead to imprisonment up to one year or additional fines.

Priority of Payment: Gratuity enjoys statutory protection and must be paid in priority over certain other liabilities. It cannot be lightly withheld or subordinated to ordinary financial obligations.

Penalty for Non-Compliance: Failure to comply with gratuity provisions may attract monetary fines, imprisonment, and liability to pay interest. The enforcement framework underscores that gratuity is a statutory right and not a discretionary benefit.

Illustration 2

Gratuity calculation for Permanent Employee

Organisation: Helping Hands Foundation (NPO) Role: Program Officer Monthly CTC: Rs.40,000 Service: 8 years Exit: Resignation

Salary Structure:

| Component | Amount (Rs.) |

|---|---|

| Basic Pay | 14,000 |

| HRA | 16,000 |

| Other Allowances | 10,000 |

| Total Salary | 40,000 |

Step 1 -- Determine "Wages" for Gratuity

Under the Code, allowances cannot exceed 50% of total salary. 50% of 40,000 = 20,000 Actual allowances = 40,000 - 14,000 = 26,000 Excess allowances = 26,000 - 20,000 = 6,000 This excess must be added back to wages.

Gratuity Wage = Basic + Excess = 14,000 + 6,000 = Rs.20,000

Step 2 -- Calculate Gratuity

Gratuity = Wage x (15/26) x Years of service = 20,000 x 0.5769 x 8 = Rs.92,304 (approx.)

Gratuity payable: Rs.92,304

Even if an NGO structures salary with higher allowances, the law recalculates wages. Therefore gratuity liability increases compared to older salary structuring practices.

Illustration 3

Fixed-Term Employee (NGO Project)

Organisation: Helping Hands Foundation (NGO) Role: Project Coordinator (donor-funded project) Contract Period: 2 years | Monthly Wage: Rs.30,000 | Exit: Contract expiry Eligibility: Gratuity payable on expiry of fixed-term contract after completion of at least 1 year.

Calculation: Gratuity = Wage x (15/26) x Completed Years = 30,000 x 0.5769 x 2 = Rs.34,614

Fixed-term employees are eligible for gratuity after 1 year, and computation is strictly proportional to completed service.

C. Employee State Insurance Corporation

Applicability: All employees earning up to Rs.21,000 per month (Rs.25,000 for persons with disability) are eligible. Every establishment in which ten or more persons are employed is covered. Coverage type: Mandatory from date of employment.

Wider scope: Includes factories, service sectors, startups, MSMEs.

Voluntary Coverage and Exemptions: Two other features are worth noting:

- Establishments not automatically covered may voluntarily opt in.

- Employers who already provide benefits that are at least equal to ESIC can apply for exemption.

Unlike under the Employees' State Insurance Act, 1948, exemptions are not indefinite. They require periodic review and renewal, which reduces misuse.

Are Consultants eligible for ESI? Consultants are generally not covered under ESI because ESI applies only to "employees" engaged under a contract of employment. A consultant typically works under a contract for services (independent professional relationship), not a contract of service (employer-employee relationship).

Benefits under the ESI Scheme: The Scheme is contributory in nature and provides a defined set of Employees' State Insurance benefits in India. These include:

- Medical benefits for insured employees and their families through ESI Scheme hospitals and dispensaries.

- Sickness benefit is a cash payment during certified illness.

- Maternity benefit for insured women, aligned with broader maternity legislation.

- Disablement benefit in case of temporary or permanent injury.

- Dependants' benefit payable to family members on the death of an insured person.

- Funeral expenses and certain additional welfare measures in specific cases.

Employee Registration: Every employee in a covered establishment must be insured. This can be done electronically or otherwise, as the Central Government prescribes.

- Register employees on the ESIC portal before or on the day of employment.

- Mandatory details: Aadhaar number, personal details, wage info.

- Insurance number: Automatically generated, valid for 30 days. Becomes invalid if Declaration Form not updated within 30 days. Used for: Filing ESIC contributions and Availing benefits for employee & family.

Contribution

| Party | Rate | Notes |

|---|---|---|

| Employer | 3.25% of wages | Rounded to next rupee |

| Employee | 0.75% of wages | Rounded to next rupee |

| Persons with disability | Employer contribution reimbursed by Central Govt | For up to 3 years or as notified |

- Contributions must be deposited into the Employees' State Insurance Fund within ESIC timelines.

- Failure to deposit attracts fines up to Rs.50,000; repeat defaults can lead to imprisonment (up to 2 years) + fine Rs.3 lakh.

ESIC Benefits

| Benefit Type | Eligibility / Conditions | Rate / Duration / Notes | Remarks / Facilities |

|---|---|---|---|

| Sickness Benefit | Contributions paid >=78 days in a contribution period | 70% of Standard Benefit Rate; Max 91 days in any two consecutive periods | Extended for long-term diseases (up to 2 years) and sterilisation procedures (full wage) |

| Maternity Benefit | Contributions paid >=70 days in previous two periods | 26 weeks (12 weeks in some cases); Medical bonus Rs.7,500 per confinement if ESIC facility unavailable | Available to insured women only |

| Disablement Benefit | Temporary: >=3 days; Permanent: total/partial disablement | 90% of standard benefit rate | Paid as per schedule of injuries |

| Dependant's Benefit | Widow, children, widowed mother, or other dependents | 90% of standard benefit rate | On death of insured person |

| Medical Benefit | Contributions active or during sickness/maternity/disablement benefits | Continuous access | Facilities: Local dispensary -> Secondary panel hospital -> Tertiary ESIC hospital; spouse eligible in case of permanent disablement or death |

| Funeral & Welfare Benefits | -- | Lump sum Rs.15,000; confinement expenses if ESIC facility unavailable | Vocational rehabilitation & re-employment for permanent disability |

Record-Keeping: Organisations are required to maintain comprehensive records, including employee registration and insurance numbers, details of contribution payments, claims and benefits disbursed, and medical benefits provided. All these records must be readily available for inspection by the ESIC authorities.

Reporting & Audit: Establishments must submit returns of contributions and any other required information within the prescribed deadlines. ESIC may audit the accounts of the establishment to ensure compliance. A digital system is in place to track filings, submissions, and inspections, facilitating transparency and timely reporting.

Do You Know? Following the enforcement of the Code on Social Security, 2020 on 21 November 2025, the Employees' State Insurance Corporation, vide Circular No. N-11011/2/2025-BFT-II dated 28.11.2025, clarified that:

- Under Section 2(24)(c), a widower and a grandparent are now included within the definition of "dependant" and are entitled to Dependent Benefit.

- Under Section 2(33)(e), the father-in-law and mother-in-law of a woman employee are now included within the definition of "family" and are entitled to Medical Benefit.

This change applies with effect from 21.11.2025 and must be considered while extending ESI benefits.

D. Employee's Compensation

Applicability: The provisions relating to employee's compensation apply to:

- persons employed in scheduled hazardous occupations (railways, mines, construction, factories, transport etc.)

- additional categories notified by the Central Government

Exclusion: Employees covered under the Employees' State Insurance (ESI) scheme are excluded because they receive parallel benefits under ESI.

Notice of Accident: The employer must notify the Competent Authority within 7 days of any accident, occurring on employer premises or serious bodily injury includes permanent loss of a limb, sight, hearing, fracture, or absence from work exceeding 20 days. Failure to report may attract penalties and adverse inference during proceedings.

Employer's Liability to Pay Compensation: An employer is liable where injury is caused:

- by accident

- arising out of employment

- in the course of employment

- due to occupational disease

The SS Code also expands protection by recognising:

Commuting Accidents: An accident occurring while commuting between residence and workplace is deemed employment-related if a nexus with employment is established.

Occupational Diseases: Diseases listed in the Third Schedule are presumed to be employment related. The Government may add but not remove diseases from this Schedule.

Situations Where Compensation is Not Payable: Employer is not liable if:

- injury causes disablement of less than 3 days

- employee was under influence of drugs/alcohol (except death/permanent disability cases)

- wilful disobedience of safety instructions

- deliberate removal of safety guards

Quantum of Compensation: The SS Code removes old statutory ceilings and links compensation directly to wages and age.

| Nature of Injury | Compensation |

|---|---|

| Death | 50% of monthly wages x relevant factor |

| Permanent total disablement | 60% of monthly wages x relevant factor |

| Permanent partial disablement | Proportionate loss of earning capacity |

| Temporary disablement | Half-monthly payment = 25% of wages |

| Funeral Expenses | Minimum Rs.15,000 |

Payment Timelines and Default: Compensation to an employee must be paid promptly when it becomes due. In cases where the employer disputes liability, a provisional payment should be made to ensure the employee is not left without support. If there is an unjustified delay in payment, the employer is liable to pay interest on the due amount and may also be required to pay additional damages of up to 50% of the compensation.

Monthly Wages Calculation for Compensation

| Length of Service | Wage Calculation for Compensation |

|---|---|

| Continuous service >= 12 months | Monthly wage = 1/12 of total wages earned over the preceding 12 months |

| Service < 1 month | Average wages of employees performing similar work |

| Other cases | Total wages earned over the last period / number of days in that period |

Medical Examination: Employees are required to submit to a medical examination provided free of charge by the employer. If an employee refuses or obstructs the examination, the payment of compensation may be suspended until compliance. Furthermore, if the injury or condition worsens due to the employee's refusal to follow medical advice or attend examinations, the compensation is adjusted as if proper care had been taken, ensuring fairness to both the employer and the employee.

Contracting and Indemnity: Employers are responsible for compensating employees who are engaged through contractors. However, the employer has the right to seek indemnity from the contractor for compensation paid. Employees also have the option to claim compensation directly from the contractor. Additionally, if a third party is responsible for the injury, the employer may recover the compensation already paid from that third party, ensuring that liability is ultimately borne by the party at fault.

Insurance and Insolvency: When an employer has an insurance contract covering employee compensation, the rights of the employee transfer to them in the event of the employer's insolvency. The insurer's liability, however, cannot exceed the original liability of the employer. In cases of insolvency or liquidation, compensation is treated as a priority debt under the Insolvency and Bankruptcy Code and the Companies Act. Half-monthly payments already made are considered redeemable as a lump sum for insolvency purposes, protecting the employee's entitlement.

Special Cases: Accidents Outside India: Certain employees working abroad fall under specific provisions of the Code. These include ship masters, seamen, aircraft crew, persons recruited by Indian companies to work abroad, and drivers, helpers, or mechanics sent overseas. Notices of accidents must be served on the ship or aircraft master, captain, or the local agent. Time limits for filing claims are prescribed: in the case of death, claims must be filed within one year of receiving news, and if the ship or aircraft is lost, the limit extends to 18 months.

Employer Statements and Registration of Agreements: The competent authority may require employers to submit statements concerning fatal accidents. Any agreements for lump-sum compensation must be formally registered to be enforceable under the Code. Registered agreements have overriding effect over other laws, ensuring legal certainty. Failure to register such agreements renders the employer liable to pay the full compensation amount, emphasising the importance of compliance.