Income Tax for NGOs (Part I)

- Income Tax Act 2025 & Draft IT Rules 2026 for Charitable institutions - Part 1

- FAQ: Income Tax for Charitable Institutions

Income Tax Act 2025 & Draft IT Rules 2026 for Charitable institutions - Part 1

You can read the information below in over 15 languages! Simply use the translation tool in the top-left corner of the screen to select your preferred language, including অসমীয়া, বাংলা, ગુજરાતી, हिन्दी, ಕನ್ನಡ, മലയാളം, मराठी, মৈতৈলোন্, नेपाली, ଓଡ଼ିଆ, ਪੰਜਾਬੀ, संस्कृतम्, தமிழ், తెలుగు, and اُردُو.

Thank you Sharad from Saathi Development Services for sharing this resource with us.

Got questions about Income Tax for NGOs? Ask them on the forum, or browse other Income Tax related questions here.

Session Layout – Session 1

- Provisions for charitable institutions under ITA 1961

- Challenges overcome through ITA 2025

- ITA 2025 – provisions and changes

- TDS provisions

- Misc provisions

Provisions in ITA 1961 for NPOs

- Chapter I-Section 2(15) Definition of charitable purpose

- Chapter III: Incomes which do not form part of total income

- Sections 11-13 (including section 10(23C) approval entities)

- Section 11 – Income from property held for charitable or religious purpose

- Section 12 – Income of trusts from contributions-12A (conditions for applicability of section 11-12) and 12AB (Procedure for registration)

- Section 13 – Section 11 not to apply in certain cases

- Chapter VI-A-80G – Deduction in respect of donations to certain funds, charitable institutions, etc

- Chapter XII – Section 115BBC Taxation of Anonymous donations 115BBI Specified income of certain institutions

- Chapter XIIB – Section 115TD-115TF Exit tax on accreted income of charitable institutions

- Chapter XVII-B – TDS provisions, Chapter XIV for Procedure for Assessment, Other scattered sections under various chapters

Challenges in ITA 1961 & Resolution in ITA 2025 effective 1.4.2026

Challenges

- Provisions spread across several chapters for charitable institutions

- Law has evolved over time

- Provisos and explanations inserted over time make understanding difficult

Resolution

- Consolidation – Chapter XVII – Special Provisions related to Certain Persons Part B – Special Provisions for Registered NPOs. Total words reduced from 12.8k to 7.6k

- Use of uniform terms for consistency and simplified language for clear understanding

- Tables, Schedules and definitions (interpretation) provided in Chapters.

- Provisos and explanations deleted

Key Definitions under ITA 2025

- "Registered non-profit organization" means any person having a valid registration under any specified provision and such registration has not been cancelled

- Section 2(23) "Charitable Purpose" includes—

- Relief of the poor;

- education;

- yoga;

- medical relief;

- preservation of environment (including watersheds, forests and wildlife);

- preservation of monuments or places or objects of artistic or historic interest;

- the advancement of any other object of general public utility;

Religious purpose not defined as was in ITA 1961

- Tax Year – means twelve months period of the financial year commencing on 1st April. Done away with Previous Year (PY) and Assessment Year (AY)

ITA 2025 for RNPO (Charitable and Religious Institutions)

Chapter XVII-B (Special Provisions for Registered NPO) is divided in seven structured subparts (Sections 332-355)

- Registration – Sections 332-333

- Income of registered NPO – Sections 334-343

- Commercial Activities by RNPO – sections 344-346

- Compliances – sections 347-350

- Violations – sections 351-353

- Approval for purpose of deduction under section 133(1)(b)(ii) – Section 354

- Interpretation – Section 355

1. Registration

Section 332 – Application for Registration – following persons (called registered non-profit organization) for claiming benefits under this Part, make an application for registration to P/CIT –

- a public trust;

- a society registered under the Societies Registration Act, 1860, or under any law in force

- a company registered under section 8/25 of the Companies Act, 2013/1956

- a University/ educational institution affiliated thereto or recognized by Govt

- an institution financed wholly/partly by Government/local authority;

- any person as referred to in

Schedule III – Income not to be included in total income of eligible persons (Table: Sl. No. 27) to (Table: Sl. No. 29) i.e. contribution to IPF setup by SE, CE and Depository and (Table: Sl. No. 36) i.e. section 10(46) i.e. entities created and notified by Govt for benefit of general public other than Sch VII Table sl 42 and

Schedule VII Persons exempt from Tax (Table: Sl. No. 10-16) PMNRF, PMCARES, SBM, Clean Ganga, CM Relief Fund etc – deleted in Budget 2026, Table Sl 17 – any University/edu institution substantially/wholly financed by Govt, Table Sl 18 – any medical institution wholly/substantially financed by Govt and Table, Sl 19 – any educational or medical institution with gross receipts upto Rs. 5 cr.PA, Table: Sl. No. 42 – any body/authority setup by Central/State Act for housing, development of cities, village, regulating activity for benefit of general public; or - any other person notified by CBDT

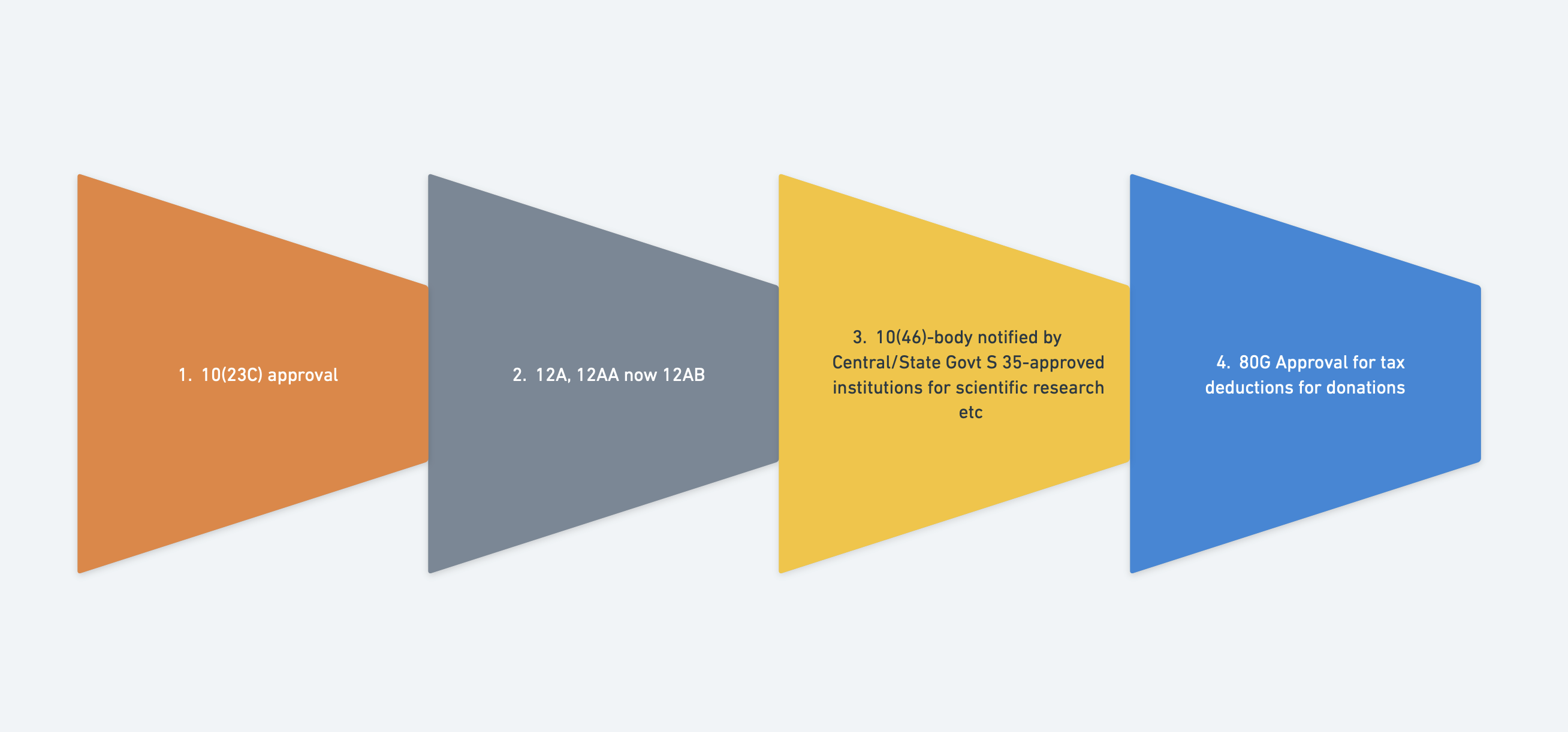

Illustrated:

10(23C) approval

12A, 12AA now 12AB

10(46)-body notified by Central/State Govt S 35-approved institutions for scientific research etc.

80G Approval for tax deductions for donations

Types of Registration/Approval for RNPO under ITA 2025

- Schedule VII (Table sl no 17-19) – erstwhile 10(23C)-(iiab-ae) non approval entities – First regime

- Chap XVII-B – Section 332 – erstwhile 12A, 12AB – 2nd regime

- Schedule III (Table sl. No 36) erstwhile 10(46) – a body notified by Central/State Govt; S 45 erstwhile S 35 – Deduction for exp by institutions on scientific research

- 133(1)(b)(ii) erstwhile 80G(5) Approval (deductions for Donations to certain Funds, charitable institutions etc)

Table-332 – Cases, Time Limit for Application, Approval by Dept and Validity of Registration

| Sl. No. | Case | Time limit for furnishing application | Time limit for passing order | Validity of registration |

|---|---|---|---|---|

| 1 | Where the activities of the applicant have not commenced and it has not been registered under any specified provision at any time before making the application. | At any time during the tax year beginning from which registration is sought. | One month from the end of the month in which application is made. | Three tax years commencing from the tax year in which such application is made. |

| 2 | Where the activities of the applicant have commenced and it has not been registered under any specified provision at any time before making the application. | At any time during the tax year, beginning from which registration is sought. | Six months from the end of the quarter in which application is made. | Five tax years commencing from the tax year in which such application is made. |

| 3 | Where the applicant has been granted provisional registration and activities have commenced. | Within six months of the commencement of activities. | Six months from the end of the quarter in which application is made. | Five tax years commencing from the tax year in which such application is made. |

| 4 | Where the provisional registration of the applicant is due to expire and activities have not commenced. | At least six months prior to the expiry of the provisional registration. | Six months from the end of the quarter in which application is made. | Five tax years following the tax year in which such application is made. |

| 5 | Where the registration of the applicant is due to expire, other than cases mentioned at serial number 4. | At least six months prior to the expiry of the registration. | Six months from the end of the quarter in which application is made. | Five tax years following the tax year in which such application is made. |

| 6 | Where the registration of the applicant has become inoperative due to switching over of regime under Section 333 | At any time during the tax year beginning from which the registration is sought to be made operative. | Six months from the end of the quarter in which application is made. | Five tax years commencing from the tax year in which such application is made. |

| 7 | Where the applicant, being a registered NPO has adopted or undertaken modification of its objects which do not conform to the conditions of registration. | Within thirty days of the date of such adoption or modification | Six months from the end of the quarter in which application is made. | Five tax years commencing from commencement of the tax year in which such application is made. |

Conditions for registration

- Person constituted/registered/incorporated for charitable purpose under (2(23) or public religious purposes

- Properties held under an irrevocable trust for benefit of general public wholly for charitable/religious purpose

- Condonation for delay by P/CIT with reasonable cause for registration application

- Accreted tax if condonation is not granted in cases for Table sl. No 3,4,5,7 (3. conversion of provisional regn, 4. renewal of provisional and 5. renewal of regular regn and 7. modification of objects)

- If income in past 2 tax years prior to application is upto Rs. 5 cr, registration granted for 10 years – applicable to cases in Table sl. 3 to 7

- For cases in Table sl. No. 2-7, P/CIT see genuineness and compliance with other laws and grant/reject registration (after giving opportunity of being heard in case of rejection)

- Provisional registration granted by P/CIT only

- Where registration of an entity registered prior to 1.4.2021 has expired under ITA 1961 and now applies for registration, P/CIT can condone with reasonable cause for delay and grant registration within 3 months of application which will be valid for 5 years from Tax Year 2021-22 i.e. upto 31.3.2026.

- Section 333 – Switching over of regimes, registration under 332 will cease from date notified as covered under Schedule III (Table sl. No.27,28,29,36) or VII (Table sl. No. 42) and vice versa

2. Income of Registered NPO

- 334 – Tax on income of RNPO – Income tax on total income for a tax year will be (a) @30% on specified income (a) at the rate applicable on taxable regular income

- 335 – Regular income includes – (a) receipts from charitable or religious activity for which registered (b) capital/revenue receipts from property/investment held (c) voluntary contribution (d) gains from commercial activity received in tax year

- 336 – Taxable regular income is (a) nil if 85% or more of income in tax year applied or accumulated as per 342 (b) 85% regular income less application and accumulation

- 337 – Specified income – taxable in same tax year (except h where it is last year)

- Anonymous donation (excludes religious/charitable cum religious except for an educational/medical institution) – Rs.1 lakh or 5% of donations whichever is higher

- Income applied for benefit of a related person

- Income applied outside India in contravention of Section 338(a)

- Investment of any income, deemed accumulated income, accumulated income, corpus, deemed corpus or any other fund in violation of 350

- Deemed corpus donation for violation of conditions in 340 (donation for repair of religious places)

- Accumulated income applied for purpose other than for which accumulated

- Accumulated income ceases to be accumulated (conditions not fulfilled)

- Accumulated income not applied within prescribed period – 342(1)

- Accumulated income paid to another registered NPO

- Income applied for other than charitable or religious purpose for which registered

- Income determined by AO more than income as shown for business undertaking

- Fair market value of asset not held in modes under Schedule XVI after expiry of 1 year from end of tax year in which acquired

- Deemed application not applied within allowed timeline

- 338 – Income not to be included in regular income –

- income applied outside India approved by CBDT to promote international welfare in which India is interested and

- corpus donation received by RNPO

- 339 – Corpus donation – donation made with specific direction by donor to treat as corpus and invested in permitted modes of investment under section 350

- 340 – Deemed corpus donation – donation for repair of temple, gurudwara, church, mosque etc deemed corpus donation

conditions – separately identified, invested as per 350, used for repair, not given as donation to any person - 341 – Application of income –

- Applied for charitable or religious purpose in India (i) amount paid in tax year for charitable/religious purpose provided section 36(4-7) – cash payment >10k to a person in a day where exception can be made and 35(b)(i) – TDS not deducted under Chapter XIX-B will apply

- 85% as donation to another registered NPO

- Application where corpus applied after 1.4.2021 is deposited back in Section 350 modes and within 5 years from application

- Application from loans and borrowings made after 1.4.2021 repaid and within 5 years from application

Application not allowed

- Depreciation if original cost of asset claimed

- Set off of excess application for previous year

- Sum paid as corpus donation to another RNPO

Application from corpus, loans and borrowings, accumulated income, deemed accumulated income, specified income for 85% application

- Deemed application – regular income applied is less than 85%, the shortfall maybe treated as deemed application where income is not received or for any other reason

- Applied in succeeding year of receipt after exercising option

- Deemed application shall be considered as application

- Entire income from capital gains will be deemed as application if net consideration is for acquiring new capital asset or pro rata if entire net consideration not utilized for acquiring capital asset

- 342: Accumulated income – (i) accumulate/set apart for maximum 5 years (excluding period for a court order/injunction) stating purpose by furnishing statement on or before due date for furnishing income tax return – Section 263(1)

(ii) Amount paid out of accumulated income to another RNPO not application

(iii) Accumulated income is to be invested as per modes specified in 350

(iv) Repurposing of accumulated income which is in conformity of its objects with prior AO approval permitted

(v) If RNPO dissolved, AO allow application of income to any other RNPO for the year in which it is dissolved based on application by RNPO - 343 – Deemed accumulated income – (i) Regular income less application and accumulated income upto 15% of regular income is deemed accumulated income to be invested in modes as per Section 350. (ii) deemed accumulated income is different from accumulated income

3. Commercial Activities by RNPO

- 344 – Business undertaking held as property – AO to allow income from such property claimed in books as charitable under Chapter 17-B

- 345 – Restriction on commercial activity by RNPO – No RNPO other than for advancement of objects of GPU undertake commercial activity unless

- Such commercial activity is incidental to attainment of objectives

- Separate books of account maintained for such activity

- 346 – Restriction on commercial activity by RNPO for advancement of object of GPU – No commercial activity unless

- Such commercial activity is for advancement of GPU object

- Commercial receipts not >20% of total receipts of tax year

- Separate books of account maintained for such activity

4. Compliances

- 347 – Books of Account – when income exceeds max not chargeable to tax, maintain prescribed books of accounts

- 348 – Audit – when income exceeds max not chargeable to tax, get audit and file audit report as prescribed

- 349 – Return of income – when income exceeds max not chargeable to tax, file ITR under section 263((1)(a)(iii) within time allowed under 263(1)(b). Exemption benefit allowed for belated return – Budget 2026 by including reference to 263(4)

- 350 – Permitted modes of investment – specified in Schedule XVI and further addition by CG

Schedule XVI – Permitted Forms or Modes of Investment or Deposits by Charitable/Religious Institution

Lists 32 modes, few examples:

- deposit in any account with the Post Office Savings Bank

- deposit in any account with a scheduled bank or a co-operative society engaged in carrying on the business of banking

- investment in immovable property;

- investment in the units issued under any scheme of the mutual fund approved by SEBI

- investment in Stock Certificate of the Sovereign Gold Bonds Scheme, 2015

- shares in a public sector company

- voluntary contributions received and maintained in the form of jewellery, furniture or any other article as the Board may, by notification specify

5. Violations

- 351 – Specified Violations – by a RNPO

- Income applied other than for objects

- Commercial activity contravening 345 – deleted for 346 (GPU) in Budget 2026

- Private religious purpose

- Benefit particular religious community/caste other than SC/ST/backward class/women and children

- Activity not genuine/not as per conditions of regn certificate

- Not complied with requirements of any other law – 332(7)

- Application for registration under 332(1) contains false information

- Where CIT on his own noticed specified violation or reference by AO or selected as per risk management strategy call for information/inquiry and cancel or otherwise within 6 months of the quarter in which notice issued.

- 352 – Tax on Accreted income – in addition to income tax be liable for tax on accreted income at MMR in following cases calculated as

A=B-C where A is accreted income, B is Fair market value of total assets and C is Total liability

Tax on accreted income has to be paid within 14 days of due date specified in Table otherwise simple interest in addition as per below

I = 1% of (T*P) where T is accreted tax and P is period of delay in month from due date

Table provides cases triggering tax on accreted income:- Registration cancelled/withdrawn

- Modified object not conforming to registration conditions and not applied for fresh registration

- Not applied on switching of regime (inoperative clause)

- Converts into form not eligible for grant of registration

- Merges with an entity which is not RNPO with same/similar objects

- On dissolution, surplus assets not transferred to another RNPO within 12 months.

Assesse in default – principal officer or trustee or org into which assets have been transferred upon dissolution upt value of assets only

- 353 – Other violations – where RNPO fails to

- Maintain books of account

- Fails to get books of account audited

- Fails to file return of income

- Is for advancement of object of GPU has commercial receipts in contravention of Section 346

Regular income less expenditure subject to following conditions will be taxable:

- Capital expenditure not allowed (ii) Exp incurred in India

- Applied for objects (iv) Not made from corpus (vi) Not made from loans and borrowings

- No depreciation allowed if acquisition cost already claimed

- No sub grant

- Payment made in contravention of Section 36(4-7) and Section 35(b)(i)

Only above allowed as application

Please note: Information is for reference only. Read our disclaimer here.

FAQ: Income Tax for Charitable Institutions

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Q1. What are the types of entities that can be registered for undertaking charitable purposes?

For charitable purpose, the following entities can be constituted:

-

Society

-

Trust

-

Not-for-Profit Company

While the aforementioned entities have separate incorporation laws, the Income Tax law applies uniformly for all.

Q2. Are NGOs and other charitable and non-profit organisations entitled to claim tax exemption under income tax law in India? Are donors who contribute to such organizations also entitled to any tax deduction?

Yes, a tax exemption can be claimed, subject to fulfilment of a set of specified conditions. Donors who contribute to such organisations can also claim tax deduction to the extent of a specified proportion of their contribution (50 per cent in most cases).

Q3. What is the justification for such exemption?

NGOs and other voluntary/non-profit organisations supplement governmental efforts in promoting economic and social development and thus serve as partners in the advancement of welfare activities. Genuine voluntary organizations have the advantage of local presence, possess local knowledge, and also bring in additional resources which help meet social and economic goals of the government. The revenue foregone by way of tax exemption is therefore employed effectively for achieving the nation’s developmental goals.

Q4. Who are the authorities responsible for granting such an exemption?

For each type of exemption, the Income Tax law specifies the authority competent to grant the necessary approval.

Q5. Section 11 exempts income from property held for “charitable purposes”. What is meant by “charitable purpose”?

Section 2(15) defines "charitable purpose" which includes:

- Relief of the poor

- Education

- Yoga

- Medical relief

- Preservation of environment (including watersheds, forests and wildlife) and

- Preservation of monuments or places or objects of artistic or historic interest, and

- The advancement of any other object of general public utility:

Provided that the advancement of any other object of general public utility shall not be a charitable purpose, if it involves the carrying on of any activity in the nature of trade, commerce or business, or any activity of rendering any service in relation to any trade, commerce or business, for a cess or fee or any other consideration, irrespective of the nature of use or application, or retention, of the income from such activity, unless—

i) such activity is undertaken in the course of actual carrying out of such advancement of any other object of general public utility; and

ii) the aggregate receipts from such activity or activities during the previous year, do not exceed twenty per cent of the total receipts, of the trust or institution undertaking such activity or activities, of that previous year.

Q6. How is “income” defined in the case of a charitable trust or institution?

“Income” in the case of a charitable trust or institution has to be understood in the broadest of terms. As in the case of any other assessee, it will include income falling under different heads, including profits and gains of business or profession, capital gains, income from house property and income from other sources (such as dividends, interest on securities, etc.).

Additionally, in the case of a charitable trust or institution, donations (voluntary contributions), which otherwise do not possess the character of “income”, are also to be included in income. All these amounts will, in the first instance, be included in the income of the charitable trust or institution, and, thereafter, exemption can be claimed subject to fulfillment of prescribed conditions.

Q7. What conditions are required to be fulfilled by a charitable or religious trust seeking exemption under Section 11?

To ensure that only organizations engaged in bona fide charitable or religious activities are allowed to claim exemption from tax, the law has prescribed a number of legal and procedural requirements. Taxpayers would be well-advised to go through the relevant provisions, particularly, Sections 11, 12, 12A, 13, 115BBC and 139(4A) of the Income Tax Act, and Rules 17, 17A, 17B and 17C of the Income Tax Rules.

For the sake of brevity and easy reference, however, the DOs & DON’Ts for the claim of exemption by a charitable or religious trust under Section 11 are summarised below:-

Dos:

(i) The trust must be a public charitable or public religious trust and not a private trust.

(ii) Income claimed to be exempt must be derived from property held under trust.

(iii) The trust must be wholly for charitable or religious purposes.

(iv) If the trust or institution has taxable income for the year before claiming exemption under Sections 11 and 12, its accounts must be audited by a Chartered Accountant (or other person competent to audit accounts under Income Tax Act) and audit report in the prescribed Form must be filed with the return of income.

(v) The trust must be registered by the Commissioner/Director of Income Tax under Section 12AB.

(vi) Activities of the trust must be carried out in India unless specific exemption is obtained

(vii) 85% or more of the income for the year must be applied to (i.e., put to use) for charitable or religious purposes, and the balance (i.e. 15% or less) must be accumulated or set apart for future application to charitable or religious purposes, or If 85% of the income is not applied to charitable or religious purposes during the year, the same must be accumulated or set apart for future application for definite and specified purposes.

For this purpose, the assessee must:

a, give a notice in writing (in Form No.10) to the Assessing Officer within the due date of filing of return of income

b, invest the money so accumulated or set apart only in specified modes.

The maximum period for which such income can be accumulated or set apart is 5 years.

(viii) If income of the trust or institution includes any income from business, such business must be incidental to the objectives of the trust, and separate accounts must be maintained for such business.

(ix) If the trust or institution had taxable income during the year without giving effect to Sections 11 and 12, it must file a return of income.

(x) Capital gains, if any during the year (whether short or long term), must be reinvested in a new capital asset in order to be deemed to have been applied to charitable purposes.

Don'ts:

(i) Property must not be held under trust for private religious purposes but for the benefit of the public.

(ii) The trust or institution must not have been created or established for the benefit of a particular religious community or caste (other than SC/ST/Backward Classes, women and children).

(iii) Under the terms of the trust or rules of the institution, no part of its income must directly or indirectly be for the benefit of the author/founder/trust/ institution/trustee/ manager or other such interested person

(iv) No part of the income or property of the trust or institution must actually be used or applied during the previous year either directly or indirectly for the benefit of any such person.

(v) None of its funds should be invested or continue to remain invested during the previous year otherwise than in the modes specified under Section 11(5) (this is subject to specified exceptions such as assets held as corpus, accretions to the same by way of bonus shares, debentures acquired under certain circumstances etc.).

(vi) Anonymous donations, if any, will be taxable at the rate of 30 per cent as per Section 115BBC of Income Tax Act.

(vii) The purposes for which income is sought to be accumulated or set apart for future accumulation must not be vague or non-specific, and cannot travel beyond the objects of the trust. The amount so accumulated cannot be applied to a different purpose, must continue to remain invested in the specified modes, and cannot be credited or paid to any other trust or institution.

Q8. What is the procedure for registration of a trust by the Commissioner of Income Tax?

The new regime for registration introduced from 1.4.2021 is now applicable for all charitable institutions for provisional and regular registration and 80G approval.

There is no perpetual registration or approval now for charitable institutions.

Q9. Is there a mechanism of provisional registration under Section 12 A of Income Tax Act for charitable institutions?

A charitable institution formed but which has not commenced charitable activity can obtain provisional registration by filing Form 10A which will be valid for a period of 3 years. The institution will have to apply in Form 10AB within 6 months of commencement of charitable activity or 6 months prior to 3 years - whichever is earlier.

Q10. Upon registration, from which Assessment Year does an assessee become eligible for exemption under Sections 11 and 12?

Upon registration, exemption under Sections 11 and 12 are available from the Assessment Year immediately after the financial year in which the application was made.

Q11. Who is competent to Audit the accounts of the trust for the purpose of Section 12A?

A Chartered Accountant or a person entitled to be appointed as an auditor of companies is authorized to carry out the requisite audit. The 3 conditions laid down in Section 12A are as follows:

a. The provisions of section 11 and section 12 shall not apply in relation to the income of any trust or institution unless organization is registered under section 12AA now 12AB

b. Books of accounts of the organization have been audited by the Chartered Accountant

c. Organization has furnished the return of income for the previous year in accordance with the provisions of sub-section (4A) of section 139, within the time allowed under that section.

Q12. What are “anonymous donations”? To what extent are they exempt in the hands of a charitable or religious trust or institution?

“Anonymous donation” has been defined as a voluntary contribution where the trust or institution receiving such contribution does not maintain record of identity indicating the name and address and other requisite particulars of the person making such contribution. Anonymous donation does not apply to religious trust or charitable cum religious trust unless donation is for education or medical institution. Anonymous donation can be received upto Rs.1 lakh or 5% of total donation received whichever is higher in a financial year beyond which tax at maximum marginal rate (MMR) would be attracted.

Q13. What are “corpus donations”? Are they taxable in the hands of a charitable or religious trust or institution?

Income in the form of voluntary contributions made with a specific direction from the donor that they shall form part of the corpus of the trust or institution, are generally referred to as “corpus donations”. Such donations are fully exempt from tax under Section 11(1 )(d) of the Act.

Q14. What is the rate of taxation applicable to the taxable income, if any, of a charitable or religious trust or organization?

Income derived from property held under trust wholly for charitable or religious purposes, to the extent it is not exempt under Sections 11 and 12 is liable to tax at normal rates applicable to an Association of Persons (AOP). Further, in cases where exemption under Section 11 is forfeited by a trust or institution on account of a default under Section 13(1)(c) or 13(1)(d) (i.e., where the trust or institution either directly or indirectly benefits its author, founder or any other person mentioned under Section 13(3), or because the funds of the trust or institution were invested otherwise than in the specified modes), income of such trust or institution will be taxable at the rate (including surcharge) applicable to the highest slab of income for the assessment year under consideration.

Q15. What is the extent of tax deduction available to a donor who contributes to charitable or religious trust or institution?

Under Section 80 G of the I-T Act, donors to such organizations are eligible for deduction as a percentage of the amount donated by them. In most cases the rate of exemption applicable is 50 per cent of the amount donated. For a donor to claim such exemption, the trust or institution to which the donation has been made must be one which has been approved by the Income Tax Department for this purpose.

Q16. What is the procedure to be followed by a trust or institution for obtaining approval under Section 80G?

The trust or institution can make an application in Form No. 10A and obtain approval in Form 10AC for a period of 3 years for provisional registration and 5 years for regular registration.

Q17. For what period is the approval granted by the Commissioner valid for 80G?

For 3 years in case of provisional registration and 5 years for regular registration

Q18. What type of organizations can claim the benefit of exemption under Section 10(23C)?

Apart from the various funds set up by the government (such as the Prime Minister’s National Relief Fund) which are specifically mentioned in Section 10(23C), a university or other educational institution, a hospital or other such institution as well as various other religious or charitable funds, trusts, institutions are eligible for the benefit of Section 10(23C) provided they are approved for this purpose by the prescribed authority [the jurisdictional Chief Commissioner of Income Tax or Director General of Income Tax(E)].

Q19. What is Section 13 of the Income Tax Act?

Section 13(1): Section 11 i.e. exemption of income does not apply in case of:

-

Trust for private religious purposes which does not ensure for the benefit of the public.

-

Trust for charitable purposes or a charitable institution created or established after the commencement of this Act, any income thereof if the trust or institution is created or established for the benefit of any particular religious community or caste.

-

If such trust or institution has been created or established after the commencement of this Act and under the terms of the trust or the rules governing the institution, any part of such income ensures, directly or indirectly for the benefit of any person referred to in sub-section (3).

-

If any part of such income or any property of the trust or the institution (whenever created or established) is during the previous year used or applied, directly or indirectly for the benefit of any person referred to in sub-section (3).

-

Non compliance of Section 11(5)-permitted modes of investment

Under Section 13(2), the following conditions will trigger disallowance:

-

if any part of the income or property of the trust or institution is, or continues to be, lent to any person referred to in sub-section (3) for any period during the previous year without either adequate security or adequate interest or both.

-

if any land, building or other property of the trust or institution is, or continues to be, made available for the use of any person referred to in sub-section (3), for any period during the previous year without charging adequate rent or other compensation;

-

if any amount is paid by way of salary, allowance or otherwise during the previous year to any person referred to in sub-section (3) out of the resources of the trust or institution for services rendered by that person to such trust or institution and the amount so paid is in excess of what may be reasonably paid for such services;

-

if the services of the trust or institution are made available to any person referred to in sub-section (3) during the previous year without adequate remuneration or other compensation;

-

if any share, security or other property is purchased by or on behalf of the trust or institution from any person referred to in sub-section (3) during the previous year for consideration which is more than adequate;

-

if any share, security or other property is sold by or on behalf of the trust or institution to any person referred to in sub-section (3) during the previous year for consideration which is less than adequate

-

if any income or property of the trust or institution is diverted during the previous year in favor of any person referred to in sub-section (3):

Section 13(3) defines the following categories as specified persons:

Here, "relative", in relation to an individual, means—

-

spouse of the individual;

-

brother or sister of the individual;

-

brother or sister of the spouse of the individual;

-

any lineal ascendant or descendant of the individual;

-

any lineal ascendant or descendant of the spouse of the individual;

-

spouse of a person referred to in sub-clause (b), sub-clause (c), sub-clause (d) or sub-clause(e)

-

any lineal descendant of a brother or sister of either the individual or of the spouse of the individual

Q20. What are the income tax returns and forms that are filed by charitable institutions?

- Form 9A-deemed application

- Form 10-Accumulation

- Form 10B/BB-Audit Report

- Form ITR 7- IT return

Q21. What are the current provisions related to Audit Report for charitable institutions

As per IT Rules 2023, eligibility for Audit Report in 10B is as follows:

-

If the total income of the trust or institution exceeds Rs.5 crore during the previous fiscal year.

-

In case a trust or institution receives any amount of foreign contribution.

-

In case any institution or trust has used any amount of its income outside India in the previous year.

Applicable uniformly for 12A and 10(23C) entities.

If 10B not applicable, 10BB to be used.

Very elaborate form specially 10B as against simple form earlier.

Q22. What are section 11(5) modes of investments

The forms and modes of investing or depositing the money referred to in clause (b) of sub- section (2) shall be the following, namely :—

-

investment in savings certificates as defined in clause (c) of section 2 of the Government Savings Certificates Act, 1959 (46 of 1959), and any other securities or certificates issued by the Central Government under the Small Savings Schemes of that Government;

-

deposit in any account with the Post Office Savings Bank

-

deposit in any account with a scheduled bank or a co-operative society engaged in carrying on the business of banking (including a co-operative land mortgage bank or a co-operative land development bank)

-

investment in units of the Unit Trust of India established under the Unit Trust of India Act, 1963 (52 of 1963)

-

investment in any security for money created and issued by the Central Government or a State Government

-

investment in debentures issued by, or on behalf of, any company or corporation both the principal whereof and the interest whereon are fully and unconditionally guaranteed by the Central Government or by a State Government

-

investment or deposit in any public sector company:

-

deposits with or investment in any bonds issued by a financial corporation which is engaged in providing long- term finance for industrial development in India and which is eligible for deduction under clause (viii) of sub- section (1) of section 36

-

deposits with or investment in any bonds issued by a public company formed and registered in India with the main object of carrying on the business of providing long-term finance for construction or purchase of houses in India for residential purposes and which is eligible for deduction under clause (viii) of sub-section (1) of section 36;

-

deposits with or investment in any bonds issued by a public company formed and registered in India with the main object of carrying on the business of providing long-term finance for urban infrastructure in India

-

investment in immovable property.

Additional as per Rule 17C (March 2018)

-

Investment in units of any scheme of a mutual fund

-

deposit with authority for low cost housing

-

Stock certificate of Sovereign Gold Bonds

-

Debt instruments of infrastructure finance company

-

Acquiring shares of NSDC, Depository.

Q23. What type of associations are entitled to seek notification under Section 35(1)(ii) or 35(1)(iii) and to exemption under Section 10(21)? What is the procedure for claiming such exemption?

After the recent amendments, approved “research associations” (and not necessarily “scientific” research associations as was the case earlier) are now eligible for notification under Section 35 and exemption from tax under Section 10 (21). However, all such associations must be approved by the central government for this purpose. The restrictions which apply to a trust or institution claiming exemption under Section 11 regarding manner of application and accumulation of income, investment of funds, business income etc. also apply to such research associations with necessary modifications. For further details, please see Chapter 10. The procedure for seeking approval of the central government under Section 35 is also discussed in detail in Chapter-10 (Para-10.3 to 10.10). The central government may reject an assessee’s application for approval under this Section where it is not satisfied regarding the eligibility of the assessee. The central government may also withdraw the approval already granted by it for the reasons discussed in Para-10.7.

Q24. Where a trust fund or institution is approved by the central government under Section 35, can an Assessing Officer still reject the claim of such trust or fund or institution to exemption under Section 10 (21)?

In such cases, the Assessing Officer, if he is of the view that the contravention of Section 10(21) has taken place, is required to intimate the central government of the contravention. He can complete the assessment by denying the benefit of Section 10(21) only if the central government withdraws the notification.

Q25. Can you state the changes in recent budgets for charitable institutions in the past 3 years?

Budget 2025

-

Government has liberalized period of registration for small NGOs i.e. those whose income in past 2 years preceding date of application is upto Rs.5 cr. Such NGOs will be registered for 10 years instead of 5 years on renewal and will not have to undergo the pain of renewal every 5 years. For instance, if 5 year NGO registration under 12AB or approval under 80G is valid upto AY 25-26 i.e. 31.3.2025, it needs to apply for12AB/80G renewal before 30.9.2025. If income in FY 24-25 and FY 23-24 is upto Rs. 5 cr, the renewal will be granted for 10 years by the Department after process of inquiry.

-

Government has provided clarification that Incomplete information provided to Income Tax Department will not be a specified violation calling for cancellation of 12AB registration. This step is welcome.

-

The definition of Specified Person under Section 13 which includes among others a person (other than founder, author) making substantial contribution of Rs.50.000/- has been revised to Rs.100,000/- in a year and Rs.10 lakhs in aggregate up the relevant year. This would reduce the reporting requirements for NGOs.

Budget 2024

- Merger of first 10(23C)-approval category with second regime Section 12 of registration under income tax-Section 11(7) effective 1.10.2024

- Section 80G can be applied even if charitable status benefit taken which was not allowed- effective 1.10.2024

- Condonation of delay in filing registration application for all categories by PCIT/CIT in case of reasonable cause effective 1.10.2024

- Timeline for disposal of application under 12AB/80G-6 months from end of the quarter in which application made effective 1.10.2024

- Merger of a charities with same/similar objects-new section 12AC specifying situations of merger when accreted tax will not be applicable effective 1.4.2025

Budget 2023

-

Application made from corpus funds or through loans and borrowings only if replenished/repaid in 5 years

-

Retrospective section 11 exemption benefit withdrawn

-

Inter charity donations of local funds-85% of amount as application

-

Exemption benefit not available for Updated IT Return

-

Timeline for filing Form 9A and 10

-

No provisional registration for existing unregistered entities

-

Exit tax in case of non renewal, non re registration or not converting provisional to normal registration

-

Incorrect or incomplete information in Form 10A a specified violations inviting cancellation of registration

Q26. What are the provisions related to maintenance of books of accounts for charitable institutions

Maintenance of books of accounts and records/documents:

-

There was no regulation regarding books of accounts by NGOs upto FY 21-22

-

Section 12A(1)(b)(i) inserted for maintaining of books of accounts and other documents wef AY 23-24.

-

Not applicable if total income is below threshold chargeable to tax.

-

Rule 17AA inserted from 10.8.2022 providing for four sub rules

Books of accounts & other documents

The specified books of accounts shall include:

-

cash book

-

ledger

-

journal

-

copies of serially numbered receipts, original copy of invoices, etc

Other documents include:

a. Record of all the projects and institutions run by the organisation

b. Record of income of the organisation during the previous year

(I) voluntary contribution containing details of name of the donor, address, permanent account number (if available) and Aadhaar number (if available);

(II) income from property held under trust referred to under section 11 of the Act along with list of such properties;

(III) income of trust other than the contribution referred in items (I) and (II)

c. Record of application out of the income during the year

(I) application of income in India, containing details of amount of application; name and address of the person to whom any credit or payment is made and the object for which such application is made, amount credited or paid

(II) application of income outside India, containing details of amount of application, name and address of the person to whom any credit or payment is made and the object for which such application is made;

(III) deemed application of income referred in section 11(1) of the Act containing details of the reason for availing such deemed application;

(IV) income accumulated or set apart as per section 11(2) containing details of the purpose for which such income has been accumulated;

(V) money invested or deposited in the forms and modes specified in 11(5)

(VI) money invested or deposited in the forms and modes other than those specified in 11(5)

d. Record of specified application out of the income of preceding years

e. Record of voluntary contribution with a specific direction to form Corpus

(I) the contribution received containing details of name of the donor, address, permanent account number and Aadhaar number;

(II) application out of such voluntary contribution referred to in item (I) containing details of amount of application, name and address of the person to whom any credit or payment is made and the object for which such application is made; amount credited or paid towards corpus to 12AB or 10(23C) institution;

(III) the forms and modes specified in section 11 (5) of the Act in which such voluntary contribution, received during the previous year, is invested or deposited;

(IV) money invested or deposited in the forms and modes other than those specified in 11(5)

f. Record of contribution received under 80G(2)(b) being treated as corpus

g. Record of Loans and Borrowings

(I) information regarding amount and date of loan or borrowing, amount and date of repayment, name of the person from whom loan taken, address of lender, permanent account number and Aadhaar number (if available) of the lender;

(II) application out of such loan or borrowing containing details of amount of application, name and address of the person to whom any credit or payment is made and the object for which such application is made;

(III) application out of such loan or borrowing, received during any previous year preceding the previous year, containing details of amount of application, name and address of the person to whom any credit or payment is made; (IV) repayment of such loan or borrowing (which was applied during any preceding previous year and not claimed as application) during the previous year

h. Record of properties held by the assessee

(I) immovable properties containing details of,

(i) nature, address of the properties, cost of acquisition of the asset, registration documents of the asset;

(ii) transfer of such properties, the net consideration utilized in acquiring the new capital asset;

(II) movable properties including details of the nature and cost of acquisition of the asset

i. Record of specified persons, as per section 13 (3) of the Act

(I) containing details of their name, address, permanent account number and Aadhaar number(if available);

(II) transactions undertaken with specified persons under 13(3) containing details of date and amount of such transaction, nature of the transaction and documents to the effect that such transaction is, directly or indirectly, not for the benefit of such specified person

j. Any other document

2. Form of keeping books of accounts and documents: Kept in written form or electronic form or digital form or print-outs of data stored in electronic form or in digital form or any other form of electromagnetic data storage device.

3. Place of maintaining books of accounts and other documents: shall be kept and maintained at its "registered office“. If the accounts are maintained other than the registered office or at various project locations, intimate assessing Officer in writing, giving full address of the other places supported by resolution of the board

4. Period for which books of accounts & other documents should be kept: Kept and maintained for a period of ten years from the end of the relevant assessment year

-

Organization having income subject to section 11(4) and 11(4)(a) to maintain a separate set of books of account of such income in line with the provision under Income Tax Act.

5. Implication of Non-Maintenance of Books of Account:

Section 13(10) and (11) inserted with effect from f AY 22-23 stating that

Income chargeable to tax shall be computed after allowing a deduction for expenditure incurred for the objects of the institution as specified in this section subject to fulfillment of the following conditions, namely:

(a) Such expenditure is not from the corpus standing to the credit of such trust or institution

(b) Such expenditure is not from any loan or borrowing;

(c) Claim of depreciation is not in respect of an asset, acquisition of which has been claimed as an application of income in the same or any other previous year; and

(d) Such expenditure is not in the form of any contribution or donation to any person.

(e) Such expenditure violating section 40(3) and 40(a)(ia) disallowed

(f) Carry forward of loss and expenditure/decurion not allowed except under the Code from section 11-13.