Fund Accounting, Costs, Budget & Grant Management

- Fund Accounting, Costs, Budget & Grant Management

- FAQ: Resource Material on Accounting specifically Grant Accounting by NPOs (as extracted from the Technical Guide on Accounting for Non-Profit Organisations (NPOs) by ICAI)

Fund Accounting, Costs, Budget & Grant Management

You can read the information below in over 15 languages! Simply use the translation tool in the top-left corner of the screen to select your preferred language, including অসমীয়া, বাংলা, ગુજરાતી, हिन्दी, ಕನ್ನಡ, മലയാളം, मराठी, মৈতৈলোন্, नेपाली, ଓଡ଼ିଆ, ਪੰਜਾਬੀ, संस्कृतम्, தமிழ், తెలుగు, and اُردُو.

Got questions about Fund Accounting? Ask them on the forum.

Fund Accounting, Income Types & Aspects Of A Grant

Fund Accounting

NGOs follow Fund based Accounting for managing grants

-

Fund accounting is an accounting system for recording resources (fund) where its use has been limited by the donor.

-

This accounting system emphasises accountability/productively over profitability which is the accounting basis for for profits

-

A separate budget is established for each fund.

-

Fund accounting utilises good internal control and reporting systems

Income of IPs-Types of Funds

Income of charitable institutions being headless is reported under following categories:

-

Aggregate Income from property held in trust (Schedule AI)

-

Voluntary contribution (Schedule VC)

-

Capital Gains

Types of funds (specified by ICAI):

Unrestricted funds: Funds received with no specific restrictions categorised as:

- Corpus-non-refundable, non reducible, reinvestment obligation

- Designated/earmarked funds-appropriated and set aside for specific purpose/future, self imposed but not legally binding

- General funds-neither designated nor restricted and also surplus/deficit transferred from I&E

Corpus comply with Income Tax provisions - Section 11(5) modes of investment, Section 11(1)(d) not treated income.

Corpus donation to another registered entity not considered application.

Corpus application to be considered application in the year of replenishment.

Corpus should be shown as Capital and income earned shown in I&E.

Restricted funds:

- Project/program grants-Project Grants to be utilised as per terms and conditions of award, restriction on both utilisation and income earned from such funds. Principle of fund based accounting

- Endowment funds: fund amount cannot be utilised, only income utilised for general/specific purpose as per terms.

- Format of financial statements as per ICAI

Accounting treatment for grants to NGOs

Grant is trust money. 3 options followed as per convention:

Option 1: Grant treated only as income.

Option 2: Grant treated only as liability.

Option 3: Grant treated as income to the extent of expenditure-hybrid method.

AS 9 mentions income recognition to the extent of expenditure for grants applicable if there is business/commerce etc.

Follow the principle of prudence in selecting the right option.

Grant Management

Grant management is a system that includes applying for and securing grants, adhering to requirements, disbursing funds, evaluating outcomes.

Grants are provided to fulfil a specified purpose, a definite outcome. Provided to institutions constituted or incorporated as such by law.

Recipient, Sub-recipient and Vendor

Recipient is the organisation receiving the grant. A recipient is sometimes called the Prime because they have the full responsibility for the funds. The document evidencing is a grant contract

Sub-recipient is involved in substantive activities of the award project. The recipient passes on some or all of its duties to the sub-recipient through a sub award. All the terms and conditions from the grant award flow down to sub-recipients through the sub-award. The document evidencing is a sub grant contract

Vendor/service provider, is one who provides goods/services to the recipient so the recipient can accomplish the project’s purposes. Selected terms and conditions might be passed through to the vendor. The document evidencing is a contract

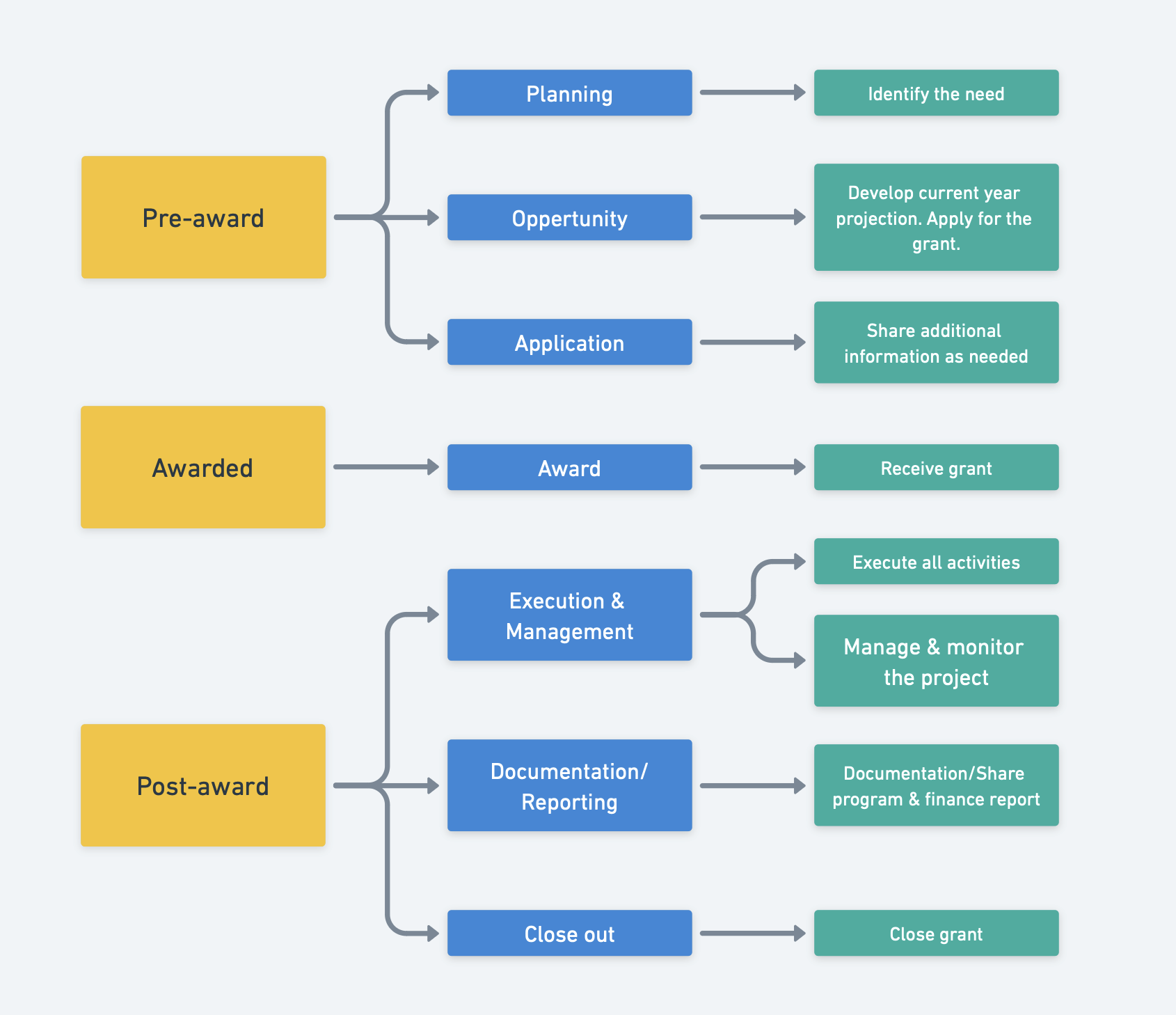

Grant management lifecycle

Illustrated:

Pre award:

- Planning

- Identify the need

- Opportunity

- Develop current year projection. Apply for the grant.

- Application

- Share additional information as needed

Awarded:

- Award

- Recieve grant

Post award:

- Execution & Management

- Execute all activities

- Manage & monitor the project

- Documentation/Reporting

- Documentation/Share program & finance report

- Close out

- Close grant

Principles of grant management

-

Accountability & Transparency with respect to utilisation of grant funds.

-

Efficient & Effective use of the grant funds.

-

Compliance with applicable laws of the land.

-

Adherence with terms and conditions of Grant Agreement.

-

Internal controls i.e. financial and accounting systems, budgetary control, funds management.

-

Timely submission of narrative and financial reports as required under the grant.

Prerequisites for robust grant management system

-

Policies & Procedures (Finance & HR)-ensuring strong internal control environment

-

Accounting-ICAI Technical Guide for accounting of NPOs-framework

-

Fund based accounting for presentation of financial statements

-

Accrual basis of accounting

-

Maintenance of prescribed books of accounts

-

Accounting Standards as framework for recording and reporting in financial statements

-

- Segregation of duties-checks and balances, dedicated finance staff

- Encourage audit and assurance-risk mitigation

General Conditions of a Grant:

-

Definition of Terms used in the grant Agreement.

-

Commitments from Funder side.

-

Commitments from the grantee side.

-

Rights arising out of contracts.

-

Technical and Scientific Reports.

-

Fixed Assets and Equipments: where should they be used and how they will vest at the project end.

-

Project Termination, normal, premature or in abnormal circumstances. Force majeure.

- Dispute Resolution.

- Confidentiality.

- Interest and Project Income.

- Employment.

- Force Majeure.

- Intellectual Property.

- Delegation.

- Notices.

Operational Terms and Condition of Grant

Example:

-

Basis of accounting

-

Separate Books of Account and separate Bank Account for Grant Funds

-

Bills and Vouchers defaced with mention of project

-

Limit on Cash Expenditure.

-

Treatment of interest

-

Procurement rules

-

Inclusion of clauses as per the laws of land

-

Program/Financial reporting and audit timelines

-

Treatment of Fixed Assets

-

Income generated from project activity

-

Closure of grant

After grant signing, a “Compliance Calendar” be prepared to ensure all terms and conditions are being adhered as per grant.

Robust Grant Monitoring System

Grant monitoring is a process to measure/review performance during grant period. It assesses physical & financial progress, identifies risks and corresponding mitigation measures, ensures that funds are used as intended and programs achieve desired outcomes and impact.

Important Tools and Process:

-

Complete understanding of terms and conditions of Grant contract.

-

Budget and LFA clearly known to both finance and programme teams.

-

Periodic Budget Variance/Deviation Analysis by finance and programme team and review by top management.

-

Timely course correction through realignment etc through addendum in grant contract.

-

Timely reporting-narrative and financial reports as stipulated in the grant contract.

Interest apportionment:

-

With a single bank account for multiple projects, interest apportionment for reporting to donors has to be made as per well defined method.

-

Interest apportionment not applicable for a dedicated bank account.

-

Interest can be additive or deductive from grant as specified in grant agreement.

Common/Core Cost

Salary Allocation for multiple projects:

Costs & Budgets

Types of Cost

Capital & Revenue cost:

- Capital costs: are one-time purchases of fixed assets that will be used for revenue generation over a longer period - more than one year.

- Revenue costs: are referred to as operating expenses, which are short-term expenses that are used in running the daily business operations.

Fixed and Variable Costs:

- Fixed cost is one that does not change in total within a reasonable range of activity. Since the fixed cost remains constant in total, the fixed cost per unit of activity decreases when the volume increases, and increases when the volume decreases.

- Variable cost or expense is where the total cost changes in proportion to changes in volume or activity.

Nonprofits account for functional expenses-allocation based on purpose of the expense:

-

Direct Costs: A cost which results in direct benefit to a beneficiary. Can be directly attributed to a program or intervention. No cost if no program activity. Categorised as Program and Admin/Operating costs.

-

Overheads/Indirect/Common costs are core/support costs for general/administration, fundraising etc. These costs are not directly attributable to any specific outputs. Suitable common cost policy for computing Indirect cost rate (ICR) detailing the allocation principle and updation of rate for negotiation with the donors. Common direct cost is also an indirect cost.

-

Historical cost: the price paid for a god when it was purchased.

-

Sunk cost: money spent that cannot be recovered.

-

Marginal cost: increase or decrease in the cost of producing one more unit or serving one more customer.

-

Opportunity cost: forgone cost for available alternatives given the resource constraint.

Cost Principles in grant budgeting

Costs budgeted for a project grant should be:

-

Allowable cost - costs which are not subject to any restrictions/limitations in the grant award.

-

Allocable cost - costs which are incurred specifically for the attainment of the objective of the grant.

-

Reasonable cost - cost which is generally recognized as necessary to be incurred by a prudent person in the conduct of normal business.

-

Consistent cost - this is applied in the same fashion throughout the grant.

-

Unallowable cost - those costs that cannot be incurred and paid under the grant.

What is a budget?

A budget is an estimation of revenue and expenses over a specified future period of time. A budget is a financial plan. It is financial blueprint of the project plan. Pre requisites are:

-

Organisation structure.

-

Data.

-

Chart of accounts.

-

Managerial support.

-

Formal process of budgeting.

Types of Budgets: Activity budget

Activity based budget, as the name suggests, covers the costs required for implementing a project activity.

For example: If project strategy is to build the capacity of civil society leaders, workshops are an activity. Workshops costs would be towards hiring resource persons, booking a venue, transportation cost, food, lodging and materials and handouts.

Illustration: Activity Budget for Conducting a Workshop

|

Particular of Expense |

Rate per unit |

No of Units |

Total in Rs |

|

Trainer Fees |

@ Rs 1000 per day |

3 days |

3,000 |

|

Venue |

@ Rs 500 per day |

3 days |

1,500 |

|

Rental for Furniture |

@ Rs 500 per day |

3 days |

1,500 |

|

Rental for Equipment |

@ Rs 100 per day |

3 days |

300 |

|

Catering Exp for Lunch and tea two times |

@ 100 per person |

55 persons X 3 days= 165 |

16,500 |

|

Conveyance paid to attendees |

@Rs 50 per person per day |

50 attendees x 3 days = 150 |

7,500 |

|

Printing of handouts |

@ Re 1 per page |

50pages x 50 copies= 2500 pages |

2,500 |

|

Grand Total |

32,800 |

Line Item Budget

-

A Line-item budget presents the budget under broad areas.

-

A line-item budget is one in which the individual financial statement items are grouped by category.

-

As you will see in the image below, there are categories (in most cases, given by donors in proposal formats) and you are required to prepare the budget under these categories. Major donors like USAID, European Commission prefer to have their budget templates by line items.

|

Line Item Budget |

||||

|

Expenses |

Units |

# of Units |

Unit Rate ($) |

Costs ($) |

|

Human Resources: |

||||

|

CEO |

Per day |

3 |

350 |

1,050 |

|

Trainer Fees |

Per day |

2 |

200 |

400 |

|

Subtotal Human Resources |

1,450 |

|||

|

Travel: |

||||

|

Trainer Airfare |

Per Person |

1 |

300 |

300 |

|

Participant Transportation |

Per Person |

30 |

10 |

300 |

|

Subtotal Travel |

600 |

|||

|

Equipment & Supplies: |

||||

|

Materials & hand-outs |

Per Person |

30 |

15 |

450 |

|

Total Equipment & Supplies |

450 |

|||

|

Other Costs, Services: |

||||

|

Venue |

Per Day |

2 |

300 |

600 |

|

Catering |

Per Person |

30 |

15 |

450 |

|

Subtotal Other Costs, Services |

1050 |

|||

|

Subtotal |

3550 |

|||

|

Overhead (10%) |

355 |

|||

|

Total |

3905 |

|||

Types of Budget

Incremental budget: New budget by making only some marginal changes to the current budget. The current budget is used as a base to which incremental assumptions are added or subtracted from the base amounts to determine new budget amounts.

Value Proposition Budgeting focuses on allocating the ideal amount of financial resources to make a product or service that provides the highest value to the customer. Another name for Value Proposition Budgeting is Priority Based Budgeting. .

Zero-based budgeting (ZBB) based on efficiency and necessity rather than budget history. Management starts from scratch and develops a budget that only includes operations and expenses essential to running the business; there are no expenses that are automatically added to the budget.

Performance based budget (PBB) is one that reflects both the input of resources and the output of services. The goal is to link funding to results delivered.

Fixed Budget: not modified for variation in actual activity.

Flexible budget: budget changes in response to activity level

Balanced, Surplus and Deficit budgets:

-

A balanced budget is a budgeting process where total expected revenues are equal to total planned spending.

-

A budget deficit occurs when expenditures surpass revenue.

-

A budget surplus means there is additional money to spend at the end of the accounting period.

Budgeting & Budgetary Control

The purpose of budget is to:

-

Ascertain reasonable estimation of costs for interventions/activities in a grant proposal/award. It is budgeting the plan.

-

Segregates direct/common/indirect or OH costs.

-

Depicts cost matching/sharing (co-financing) for multi donor grant.

-

Is a framework for a grant for donor-donee.

-

Enables course correction based on measurement of actual achievements versus estimates.

Budgetary control is the process to:

-

Track income and expenditure (annual and cumulative) by budget lines versus original/revised (realigned) budget based on record of income and expenditure budget line and activity wise entered timely in books.

-

Ascertain deviation/tolerance for expenditure under budget lines in grant award and timely approvals for spends beyond permissible limits.

Please note: Information is for reference only. Read our disclaimer here.

FAQ: Resource Material on Accounting specifically Grant Accounting by NPOs (as extracted from the Technical Guide on Accounting for Non-Profit Organisations (NPOs) by ICAI)

Definitions and Key Concepts

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

As per the Technical Guide by ICAI, the following accounting terms have the meanings specified:

Accounting policies are the specific accounting principles, and the methods of applying these principles adopted by NPOs in the preparation and presentation of financial statements.

Accrual basis means a basis of accounting under which transactions and other events are recognized when they occur (and not only when cash or its equivalent is received or paid). Therefore, the transactions and events are recorded in the accounting records and reported in the financial statements of the periods to which they relate. The elements recognised under accrual basis of accounting are assets, liabilities, revenue and expenses. Financial statements prepared on an accrual basis inform users not only of past events involving the payment and receipt of cash but also of obligations to pay cash in future and of resources that represent cash to be received in future. Hence, they provide information about past transactions and other events that is most useful to users in making economic decisions.

Assets are resources controlled by an NPO as a result of past events and from which future economic benefits and/or service potential are expected to flow that enable the NPO to achieve its objectives.

Corpus is unrestricted funds which comprises of non-reducible funds of capital nature, contributed by founders/promoters of the NPO.

Designated funds are unrestricted funds which have been set aside by the management of the NPOs for specific purposes or to meet specific future commitments. These are also called earmarked funds

Expenses are decreases in economic benefits during the accounting period in the form of outflows or depletion of assets or incurrences of liabilities that result in decreases in NPO’s funds other than decreases relating to transfers from corpus.

Fair value is the amount for which an asset could be exchanged or a liability could be settled between knowledgeable, willing parties in an arm’s length transaction.

Financial statements include balance sheet as at the end of the financial year,income and expenditure account for the financial year, cash flow statement for the financial year (where applicable) and other statements and explanatory notes which form part thereof.

Government grants are assistance by the Government in cash or kind to NPO for past or future compliance with certain conditions. They exclude those forms of Government assistance which cannot reasonably have a value placed upon them and transactions with Government which cannot be distinguished from normal transactions of an NPO.

Government refers to Government, Government agencies and similar bodies whether local, national or international.

Income is the increase in economic benefits during the accounting period when that results in an increase in NPO’s funds other than increases relating to contributions to corpus.

Liabilities are present obligations of the NPO arising from past events, the settlement of which is expected to result in an outflow from the NPO’s resources embodying economic benefits.

Restricted funds are contributions received by an NPO, the use of which is restricted by the contributor(s).

Unrestricted funds are contributions received or funds generated by an NPO, the use of which is not restricted by the contributor(s).

Accounting Framework for NPOs

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

It is often argued that since profit is not the objective of NPOs, the accounting framework which is relevant for business entities is not appropriate for NPOs. With a view to recommend a suitable accounting system for NPOs, it would be imperative to understand the major ingredients of an accounting framework. An accounting framework primarily comprises the following:

(a) Elements of financial statements primarily comprising of income, expenses, assets and liabilities: The framework aims to identify the items that should be considered as income, expenses, assets and liabilities in NPOs, for the purpose of including the same in the financial statements by defining the aforesaid terms.

(b) Principles for recognition of items of income, expenses, assets and liabilities: These principles lay down the timing of recognition of the aforesaid items in the financial statements of NPOs. In other words, these principles lay down when an item of income, expense, asset or liability should be recognised in the financial statements.

(c) Principles of measurement of items of income, expenses, assets and liabilities: These principles lay down at what amount the aforesaid items should be recognised in the financial statements.

(d) Presentation and disclosure principles: These principles lay down the manner in which the financial statements are to be presented by NPOs and the disclosures to be made therein.

There is no difference in the application of the recognition principles to business entities and NPOs. For example, the timing of the recognition of a grant as an income in the financial statements of an organisation does not depend upon the purpose for which the organisation exists. A grant is recognised as income in the financial statements, under accrual basis of accounting, when it becomes reasonably certain that the grant will be received and that the organisation will fulfil the conditions attached to it. Similarly, principles for recognition of other income, expenses, assets and liabilities would be the same for business entities and NPOs.

In so far as the measurement principles are concerned, the same are relevant to NPOs as they are to business entities. For example, depreciation on assets represents primarily the extent to which an asset is used during an accounting period by an organisation. Thus, whether an asset, such as a photocopying machine, is used by an NPO or by a business entity, the measure of charge by way of depreciation depends primarily upon the use of an asset rather than the purpose for which the organisation is run, i.e., for profit or not-for- profit motive. Accordingly, the measurement principles for other expenses, income, assets and liabilities are the same for business entities as well as NPOs. However, considering the nature of activities performed by these entities, in limited cases, measurement principles have been amended where considered appropriate.

In so far as presentation of financial statements is concerned, NPOs generally follow what is known as ‘fund-based accounting’ whereas the business entities do not follow this system. This is because NPOs may be funded by numerous grants, donations or similar contributions, which may or may not impose conditions on their usage. In other words, the use of some funds may be restricted by an outside agency such as a donor or self - imposed by the organisation. The restrictions can be temporary or permanent (e.g., in case of endowments). Certain contributions may not carry restrictions of usage, i.e., these are unrestricted.

Basis of Accounting adopted by NPOs

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

-

The commonly prevailing basis of accounting are:

- cash basis of accounting; and

- accrual basis of accounting.

-

Under the cash basis of accounting, transactions are recorded when the related cash receipts or cash payments take place. Thus, the revenue of NPOs, such as donations, grants, etc. are recognised when funds are actually received. Similarly, expenses on acquisition and maintenance of assets used for rendering services as well as for employee remuneration and other items are recorded when the related payments are made. The end product of the cash basis of accounting is a statement of receipts and payments that classifies cash receipts and cash payments under different heads. A statement of assets and liabilities may or may not be prepared.

-

Accrual basis of accounting is the method of recording transactions by which revenue, expenses, assets and liabilities are recognized in the accounts in the period in which they accrue. The accrual basis of accounting includes considerations relating to deferral, allocations, depreciation and amortisation. This basis is also referred to as ‘Mercantile Basis/system of Accounting’.

-

Accrual basis of accounting attempts to record the financial effects of the transactions and other events of an enterprise in the period in which they occur rather than recording them in the period(s) in which cash is received or paid. Accrual basis recognises that the economic events that affect an enterprise’s performance often do not coincide with the cash receipts and payments. The goal of accrual basis of accounting is to relate the accomplishments (measured in the form of revenue) and the efforts (measured in terms of costs) so that the reported net income measures an enterprise’s performance during a period rather than merely listing its cash receipts and payments. Apart from income measurement, accrual basis of accounting recognises assets, liabilities or components of revenue and expenses for amounts received or paid in cash in past, and amounts expected to be received or paid in cash in future.

-

In cash-based accounting, no account is taken of whether the asset is still in use, has reached the end of its useful life, or has been sold. Thus, cash based information fails to show a comparable statement of the financial position and performance for the accounting period. A cash-based system does not provide information about total costs of an organisation’s activities. On the other hand, an accrual system of accounting offers the opportunity to the organisation to improve management of assets and provides useful information about the realistic amount of organisation’s liabilities, relating to both debts and other obligations such as employee entitlements.

-

NPOs registered under the Companies Act, 2013, are required to maintain their books of account according to accrual basis as mandated in section 128(1) of the said Act. If the books are not kept on accrual basis, it shall be deemed that proper books of account are not kept as per the provisions of the aforesaid section.

-

Accrual is the scientific basis of accounting and has conceptual superiority over the cash basis of accounting. It is, therefore, recommended that all NPOs, including non-corporate NPOs, should maintain their books of account on an accrual basis.

Accounting Standards

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

-

Accounting is often said to be a social science. It operates in an open and ever-changing economic environment. The nature of transactions entered into by various enterprises and the circumstances surrounding such transactions differ widely. This characteristic of accounting measurements historically led to the adoption of different accounting practices by different enterprises for dealing with similar transactions or situations.

-

Comparability is one of the important qualitative characteristics of accounting information. This implies that the information should be measured and presented in such a manner that the users are able to compare the information of an enterprise through time and with similar information of other enterprises. Adoption of different accounting practices by different enterprises for similar transactions or situations tends to reduce the comparability and interpretation of accounting information.

-

Recognising the need for bringing about a greater degree of uniformity in accounting measurements, the trend all over the world now is towards formulation of uniform Accounting Standards to be adopted in the preparation of accounting information and its presentation in financial statements. Accounting Standards lay down the rules for recognition, measurement, presentation and disclosure of accounting information by different enterprises.

Applicability of Accounting Standards to NPOs

- NPOs should follow recognition and measurement principles, within the framework of accrual basis of accounting, for the purpose of preparation of their financial statements. Sound accounting principles under accrual basis of accounting have been laid down in the Accounting Standards,

-

In India, the ICAI plays a pivotal role in formulating Accounting Standards that are instrumental in carrying out accounting reforms from time to time. ICAI has also recognised the needs of users of financial information of various forms of entities and formulated/ prescribed appropriate sets of Accounting Standards. Accordingly, at present, there are three sets of Accounting Standards:

-

Indian Accounting Standards (Ind AS) for specified class of companies notified under Companies (Indian Accounting Standards) Rules, 2015 (as amended from time to time);

-

Accounting Standards (AS) notified under Companies (Accounting Standards) Rules, 2021, (as amended from time to time) for companies other than those following Ind AS;

-

Accounting Standards (AS) prescribed by ICAI for entities other than companies.

-

-

Indian Accounting Standards (Ind AS) for Companies

In view of global developments and importance of integrating local Accounting Standards with global financial reporting standards, keeping in view the Indian legal and economic scenario, IFRS converged Ind AS have been notified and are applicable to all listed companies and listed Non- Banking Financial Companies (NBFCs) and to unlisted companies and unlisted NBFCs with networth of INR 250 crores or more. Ind AS are also applicable to holding/subsidiaries/joint ventures/associates companies of such companies.

-

Accounting Standards (AS) notified under Companies (Accounting Standards) Rules, 2021 for companies other than those following Ind AS

Companies that are not covered under Ind AS, as given in paragraph above, are required to apply Accounting Standards (AS) notified under the Companies Act as Companies (Accounting Standards) Rules, 2021. As on date, Accounting Standards (AS) 1 to 5, 7 and 9 to 29 are effective. As per the Companies (Accounting Standards) Rules, 2021, Small and Medium Companies (SMCs) are given certain exemptions/relaxations.

-

Accounting Standards (AS) prescribed by ICAI for entities other than companies.

ICAI, keeping in view the fact that the Accounting Standards (AS) notified under Companies Act will only be applicable to the companies, announced the scheme for applicability of Accounting Standards (AS) issued by ICAI for non-company entities.

It is apparent that the Accounting Standards formulated by the ICAI do not apply to an NPO if no part of the activity of such an entity is commercial, industrial or business in nature. The Standards would apply even if a very small proportion of activities is considered to be commercial, industrial or business in nature. It is, therefore, recommended that all NPOs, irrespective of the fact that no part of the activities is commercial, industrial or business in nature, should follow accrual basis of accounting and Accounting Standards other than for section 8 companies for which specific provisions of the Companies Act 2013 are already applicable. This is because following the Accounting Standards laid down by ICAI would help NPOs to maintain uniformity in the presentation of financial statements, appropriate disclosures and transparency. However, while applying the Accounting Standards certain terms used in the Accounting Standards may need to be modified in the context of the corresponding appropriate terms for NPOs.

Books of accounts maintained by NPOs

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Every NPO should maintain proper books of account with respect to:

-

all sums of monies received by the NPO and the matters in respect of which receipts take place, showing distinctly the amounts received from income generating activities and through grants and donations;

-

all sums of money expended by the NPO and the matters in respect of which expenditure is incurred;

-

all assets and liabilities of the NPO.

Proper books of account would not be deemed to be kept with respect to the matters specified therein if:

-

Such books are not kept as are necessary to give a true and fair view of the state of affairs of the NPO, and to explain its transactions;

-

Such books are not kept on accrual basis and according to the double entry system of accounting; and

-

Such books are not kept so as to reflect a true and fair view of various funds maintained by the NPO.

The books of account of an NPO may be structured in a manner that is suited to its needs and requirements. For instance:

-

A separate set of books and records may be maintained for foreign and Indian contributions, as per the requirements of the Foreign Contribution (Regulation) Act, 2010 (as amended).

-

Similarly, separate sets of books and records may be maintained for various projects, branches and field offices that the NPO may have for implementing its programmes and interventions.

-

Separate ledgers and records may also be maintained with regard to the funds representing the grants received from various sources, including the Governments and different funding agencies, received with or without stipulations and restrictions. This may also be referred to as Fund Based Accounting, which is discussed in detail in the following paragraphs.

Financial statements

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

The accounting process in an organisation culminates in the preparation of its financial statements. Financial statements are intended to reflect the operating results during a given period and the state of affairs at a particular date in a clear and comprehensive manner. The basic financial statements relevant to an NPO are income and expenditure account and balance sheet and notes, other statements and explanatory material that are an integral part of the financial statements. They may also include supplementary schedules and information based on or derived from, and expected to be read with such statements. In addition, NPOs should also prepare a cash flow statement in accordance with Accounting Standard (AS) 3, Cash Flow Statements where applicable. Financial statements do not, however, include reports by the governing body, for example, the trustees, statements by the Chairman, discussion and analysis by management and similar reports that may be included in a financial or annual report.

Income and expenditure account is a nominal account which is prepared by an NPO in lieu of a profit and loss account. An income and expenditure account should contain all revenue, gains and other income and expenses and losses incurred by an NPO during an accounting period. The net result, i.e., the difference between revenues and expenses is depicted in the form of surplus, i.e., excess of income over expenditure, or deficit, i.e., excess of expenditure over income for the period. For the preparation of income and expenditure account only revenue items are taken into consideration and capital items are totally excluded. Incomes received in advance and prepaid expenses at the end of the accounting period are also excluded while preparing this account and are disclosed as a liability and an asset, respectively, in the balance sheet. These are included as incomes and expenses in the accounting periods to which they relate.

Since the purpose of fund based accounting in an NPO, discussed in detail hereinafter, is to present income and expense in respect of restricted funds as distinguished from unrestricted fund, it is recommended that the income and expenditure account should have three columns, namely,

-

‘Unrestricted Funds’, in NPOs generally consists of General Fund or otherwise known as Capital Fund’;

-

‘Restricted Funds’; and

-

‘Total’ column reflecting aggregate income and expenses of ‘Unrestricted Funds’ and ‘Restricted Funds’.

The NPOs can further classify the ‘Unrestricted Funds’ column in the Income and Expenditure Account into ‘General Funds’ and ‘Designated Funds’.

NPOs reflect restricted and unrestricted funds separately in their financial statements. Restricted funds are those designated for utilisation for specific purposes either by donors or by NPO and such funds should be utilised only for those specific purposes. On the other hand, unrestricted funds are those which can be spent at the discretion of the NPO but within the defined objectives of such NPO.

NPOs should not present the balance sheet in multi-columnar form. An integrated balance sheet for the NPO as a whole should be presented. In the balance sheet, assets and liabilities should not be set-off against each other, even though these may be related to the same programme/project. Rather these should be disclosed separately. Movement and balance of various funds should be distinctly disclosed in the balance sheet under their respective category.

In the preparation and presentation of financial statements, the overall consideration should be that they give a true and fair view of the state of affairs of the NPO and of the surplus or deficit as reflected in the balance sheet and the income and expenditure account, respectively. The financial statements should disclose every material transaction, including transactions of an exceptional and extraordinary nature. The financial statements should be prepared in conformity with relevant statutory requirements, the Accounting Standards and other recognised accounting principles and practices.

As explained in earlier paragraphs, NPOs incorporated under section 8 of the Companies Act, 2013, are governed by the provisions of the said Act. Under the Act, these NPOs are required to follow the Accounting Standards notified by the MCA and to prepare balance sheet and statement of profit and loss account (income and expenditure account in case of companies not carrying business for profit) in the formats set out in Schedule III to the Act, or as near thereto as circumstances admit. NPOs which are not registered under the Companies Act but the statute which governs them prescribes a format for the purpose of preparation of the financial statements, should prepare the financial statements in accordance with the requirements of the said statute. The Accounting Standards should also be followed by such NPOs as are already discussed in this Technical Guide. For use by NPOs, which are not governed by any statute or for which the governing statute does not prescribe any formats, formats of financial statements are given hereinafter. It may be emphasised that an NPO may modify the formats appropriately keeping in view the nature of activities, requirements of donor agencies, etc. The formats should be viewed as laying down the minimum requirements that NPOs should present in their financial statements. Those NPOs which wish to present more detailed information are encouraged to do so.

Fund based accounting

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

NPOs frequently receive grants/donations and other forms of revenue the use of which may be either unrestricted or subject to the restrictions imposed by the contributors, i.e., such funds can only be used for specific purposes and, therefore, are not available for an NPO’s general purposes. Further, there might also be legal/ other binding restrictions on NPOs to use certain specific amounts only for specified purposes or NPOs may also, on their own, earmark certain unrestricted funds for specific purposes. For the purpose of appropriate presentation and disclosure of these funds in the financial statements, it is necessary to understand their nature and characteristics, which is described below:

-

Unrestricted funds: Unrestricted funds refer to funds contributed to an NPO with no specific restrictions. The obligation of an NPO while accepting an unrestricted donation or grant is to ensure its usage for the general purposes of the NPO. All incomes (donations, legacies, investment income, fees, etc.) not subject to external restrictions are part of unrestricted funds. The unrestricted funds can be further classified into three categories viz., corpus, designated funds and general fund.

- Corpus: Corpus refers to the funds contributed by founders/promoters generally to start the NPO. They are non- reducible funds which can, however, be increased by additional contribution by the founders/ promoters in furtherance of the objects of the NPO. These funds need to be distinguished from funds which are in the nature of founders’/promoters’ contribution, which are grants given by contributors other than founders/promoters with reference to the total investment in an undertaking or by way of contribution towards outlay. No repayment is ordinarily expected of such grants.

- Designated funds: Designated funds are unrestricted funds which have been set aside by the trustees/ management of an NPO for specific purposes or to meet future commitments. Unlike restricted funds, any designations are self-imposed and are not normally legally binding. The NPO can lift the designation whenever it wishes and reallocate the funds to some other designated purpose.

- General fund: Unrestricted funds other than ‘designated funds’ and ‘corpuses’ are part of the ‘General Fund’.

-

Restricted funds: Restricted funds are subject to certain conditions and obligations set out by the contributors and agreed to by the NPO when accepting the contributions. The restriction may apply to the use of the monies received or income earned from the investment of such monies or both. Funds, the use of which is subject to legal restrictions are also considered as restricted funds.

Endowment funds are another form of restricted funds. Endowment funds are those funds which have been received with a stipulation from the contributor/donor that the amount received should not be used for any purpose. Only the income earned from these funds can be used either for general purposes of the NPO or for specific purposes, depending on the terms of the contribution made. Usually, the amount received is invested outside the NPO as per the terms of the contribution, if any.

Designated funds are created by appropriation of the surplus for the year for meeting a revenue expenditure or capital expenditure in future. When revenue expenditure is incurred with respect to a designated fund, the same is debited to the income and expenditure account. A corresponding amount is transferred from the concerned designated fund account to the credit of the income and expenditure account after determining the surplus/deficit for the year since the purpose of the designated fund is over to that extent. Where the designated fund has been created for meeting a capital expenditure, the relevant asset account is debited by the amount of such capital expenditure and a corresponding amount is transferred from the concerned designated fund account to the credit of the income and expenditure account after determining surplus/deficit for the year. In respect of the assets, e.g., a building, being constructed by an NPO, on completion of the same, the entire balance, if any, of the relevant designated fund is transferred to the credit of the income and expenditure account after determining the surplus/ deficit for the year.

In case an NPO holds specific investments against the designated funds, income earned, if any, on such investments, is credited to the income and expenditure account for the year in which the income is earned. An equivalent amount may be transferred to the concerned designated fund account after determining the surplus/deficit for the year as per the policy of the NPO.

All items of revenue and expenses that do not relate to any designated fund or restricted funds are reflected in the ‘General Fund’. The surplus/ deficit for the year after appropriations is transferred and disclosed as surplus/deficit as a part of ‘General Fund’ in the balance sheet. Apart from such surplus/deficit, the ‘General Fund’ also includes the following which are separately disclosed in the balance sheet:

Restricted funds, that represent the contributions received the use of which is restricted by the contributors, are credited to a separate fund account when the amount is received and reflected separately in the balance sheet. Such funds may be received for meeting revenue expenditure or capital expenditure. Where the fund is meant for meeting revenue expenditure, upon incurrence of such expenditure, the same is charged to the income and expenditure account (‘Restricted Funds’ column); a corresponding amount is transferred from the concerned restricted fund account to the credit of the income and expenditure account (‘Restricted Funds’ column). Where the fund is meant for meeting capital expenditure, upon incurrence of the expenditure, the relevant asset account is debited which is depreciated as per AS 10. Thereafter, the concerned restricted fund account is treated as deferred income, to the extent of the cost of the asset, and is transferred to the credit of the Income and Expenditure Account in proportion to the depreciation charged every year (both the income so transferred and the depreciation should be shown in the ‘Restricted Funds’ column). The unamortised balance of deferred income would continue to form part of the restricted fund. Any excess of the balance of the concerned restricted fund account over and above the cost of the asset may have to be refunded to the donor. In case the donor does not require the same to be refunded, it is treated as income and credited to the income and expenditure account pertaining to the relevant year (as ‘General Fund’). Where the restricted fund is in respect of a non-depreciable asset, the concerned restricted fund account is transferred to the ‘Capital Reserve’ in the balance sheet when the asset is acquired.

The restricted funds will normally carry a stipulation as to the use of income earned on investments made out of the contributions received. If the terms stipulate that the income earned should be used for the same purpose for which the contribution was made, the income earned should be credited to the concerned restricted fund account. Where the terms stipulate a general use of the income earned, the same should be credited to the income and expenditure account (as ‘General Fund’) of the year in which the income is so earned.

With regard to endowment funds, the income earned from investments of these funds is recognised in the income and expenditure account only to the extent of the expenditure incurred for the relevant purpose. Both the income and the expense should be shown in the ‘Restricted Funds’ column. Any excess of the income not recognised as aforesaid would continue to remain part of the concerned fund.

Disclosures

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

Accounting Standard (AS) 1, Disclosure of Accounting Policies, principally requires the disclosure of significant accounting policies and specifies the manner of their disclosure. A clear statement of significant accounting policies followed in the preparation and presentation of financial statements is necessary, irrespective of the type of entity presenting the financial statements. Further, all significant accounting policies should be disclosed at one place. Accordingly, NPOs should disclose their significant accounting policies at one place.

Where an NPO has followed a basis of accounting other than accrual, a disclosure in this regard should be made. Further, an illustrative list of accounting policies that an NPO could disclose in accordance with the laid down Accounting Standards governing these policies is as follows:

-

The basis of recognition of major types of expenses and revenue

-

Accounting for income from and expenditure on specialised activities such as research

-

Conversion or translation of foreign currency (in case of organisations receiving foreign funds)

-

Valuation of inventories

-

Valuation of investments

-

Treatment of employee benefits

-

Valuation of property, plant and equipment

-

Treatment of provisions, contingent liabilities and contingent assets

-

Treatment for Government grants

-

Treatment for Intangible assets

-

Impairment of assets

-

Effects of changes in foreign exchange rates

As per Accounting Standard (AS) 2, Valuation of Inventories, an NPO should disclose in the financial statements:

-

the accounting policies adopted in measuring inventories, including the cost formula used; and

-

The total carrying amount of inventories and its classification appropriate to the NPO.

As per Accounting Standard (AS) 9, Revenue Recognition, in addition to the disclosures required by AS 1, an NPO should also disclose the circumstances in which revenue recognition has been postponed pending the resolution of significant uncertainties and should recognise revenue when ultimate collection is reasonably certain.

As per Accounting Standard (AS) 10, an NPO should disclose in the financial statements for each class of property, plant and equipment:

-

The measurement bases (i.e., cost model or revaluation model) used for determining the gross carrying amount;

-

total depreciation for the period for each class of assets; and

-

the gross carrying amount and accumulated depreciation at the beginning and end of the period; and

-

a reconciliation of the carrying amount at the beginning and end of the period showing additions, disposals, acquisitions and other movements during the year.

The depreciation rates or the useful lives of the assets should be disclosed in the financial statements alongwith the disclosure of other accounting policies In case, they are different from the principal rates specified in the statute governing the NPO it should make specific mention of the fact.

As per Accounting Standard (AS) 10, an NPO should make the following disclosures in the financial statements:

-

amount of expenditure recognised in the carrying amount of an item of property, plant and equipment in the course of its construction or amount of contractual commitments for the acquisition of property, plant and equipment; and

-

the effective date of the revaluation, , the method and significant assumptions applied in estimating fair values of the items, whether an external valuer was involved in carrying out the revaluation, and revaluation surplus.

As per Accounting Standard (AS) 11, The Effects of Changes in Foreign Exchange Rates, an NPO should make the following disclosures in its financial statements:

-

the amount of exchange differences included in the income and expenditure account for the period; and

-

net exchange differences accumulated in foreign currency translation reserve separately, and a reconciliation of the amount of such exchange differences at the beginning and end of the period.

As per Accounting Standard (AS) 12, Accounting for Government Grants, an NPO should make the following disclosures in the financial statements:

-

The accounting policy adopted for Government grants, including the methods of presentation in the financial statements.

-

The nature and extent of Government grants recognised in the financial statements, including grants by way of non-monetary assets given at a concessional rate or free of cost.

These disclosures are also required to be made in respect of donations and other grants received by an NPO.

As per Accounting Standard (AS) 13, Accounting for Investments, an NPO should make the following disclosures in the financial statements:

- the accounting policies for the determination of carrying amount of investments;

- classification of investments - whether current or long-term (refer AS- 13);

- the amounts included in income and expenditure account for:

- interest, dividends, and rentals on investments showing separately such income from current and long-term investments;

- profits and losses on disposal of current investments and changes in the carrying amount of such investments; and

- profits and losses on disposal of long-term investments and changes in the carrying amount of such investments;

- significant restrictions on the right of ownership, realisability of investment or the remittance of income and proceeds of disposal;

- the aggregate amount of quoted and unquoted investments, giving the aggregate market value of quoted investments;

- other disclosures as specifically required by the relevant statute governing the NPOs.

As per Accounting Standard (AS) 17, Segment Reporting, an NPO that is operating in different geographical locations or is involved in different kinds of service delivery programmes/projects which meet the definitions of ‘geographical segment’ and ‘business segment’, should disclose segmental information according to the requirements of AS 17. However, for micro, small and medium sized NPOs falling within the meaning of MSMEs/SMCs AS 17 is not mandatory. Such entities are, however, encouraged to comply with AS 17.

Accounting Standard (AS) 18, Related Party Disclosures, establishes the requirements for disclosure of related party relationships, and transactions between a reporting enterprise and its related parties. Related party – parties are considered to be related if at any time during the reporting period one party has the ability to control the other party or exercise significant influence over the other party in making financial and/or operating decisions. Related party transaction is a transfer of resources or obligations between related parties, regardless of whether or not a price is charged. Key management personnel are those persons who have the authority and responsibility for planning, directing and controlling the activities of the reporting enterprises.

- sale, purchase, and transfer of property;

- services received or provided;

- property and equipment leases;

- borrowing or lending, including guarantees; and

- receipt of salary, honorarium or any other monetary or non-monetary benefits.

Parties are considered to be related if at any time during the reporting period one party has the ability to control the other party or exercise significant influence over the other party in making financial and/or operating decisions. For the purposes of AS 18, trustees of an NPO would be considered as key management personnel and, accordingly, trustees and their relatives would, inter alia, be treated as related parties. It may be noted that according to AS 18, relative, in relation to an individual, means the spouse, son, daughter, brother, sister, father and mother who may be expected to influence, or be influenced by, that individual in his/her dealings with the reporting enterprise. For micro and small sized NPO falling within the meaning of MSME/SMC , AS 18 is not mandatory. However, due to the onerous implications of related party transactions on the functioning of an NPO, it is recommended that the disclosures required in AS 18 should be made by all NPOs.

As per the requirements of Accounting Standard (AS) 19, Leases, where an NPO is a lessee, in case of a finance lease, it should in addition to the requirements of AS 10, make the following minimum disclosures:

- assets acquired under finance lease as segregated from the assets owned;

- for each class of assets, the net carrying amount at the balance sheet date;

- contingent rents recognised as expense in the income and expenditure account.

(Only minimum disclosure requirements as per AS 19)

Where an NPO is a lessee, for operating leases it should make the following minimum disclosures:

-

Lease payments recognised in the income and expenditure account for the period, with separate amounts for minimum lease payments and contingent rents;

-

Sub-lease payments received (or receivable) recognised in the income and expenditure account for the period.

As per Accounting Standard (AS) 26, Intangible Assets, with regard to intangible assets, an NPO should disclose in the financial statements the following for each class of intangible assets, distinguishing between internally generated intangible assets and other intangible assets:

-

the useful lives or the amortisation rates used;

-

the amortisation methods used;

-

the gross carrying amount and the accumulated amortisation (aggregated with accumulated impairment losses) at the beginning and end of the period; and

-

a reconciliation of the carrying amount at the beginning and end of the period showing additions indicating separately those from internal development and through amalgamation, retirement and disposals, impairment losses recognised and reversed, amortisation recognised and other movements during the period

An NPO should also disclose in the financial statements:

-

if an intangible asset is amortised over a period of more than ten years, the reasons why it is presumed that the useful life of an intangible asset will exceed ten years from the date when the asset is available for use. While giving these reasons, the NPO should describe the factor(s) that played a significant role in determining the useful life of the asset;

-

a description, the carrying amount and remaining amortisation period of any individual intangible asset that is material to the financial statements of the NPO as a whole;

-

the existence and carrying amounts of intangible assets whose title is restricted and the carrying amounts of intangible assets pledged as security for liabilities; and

-

the amount of commitments for the acquisition of intangible assets.

-

The financial statements of an NPO should also disclose the aggregate amount of research and development expenditure recognised as an expense during the period.

Accounting Standard (AS) 27, Financial Reporting of Interests in Joint Ventures, sets out the principles and procedures for accounting for interests in joint ventures and reporting of joint venture assets, liabilities, income and expenses in the financial statements of venturers and investors. In case of NPOs, there may be instances where two or more NPOs jointly undertake or fund a certain project or activity which is considered as a jointly controlled operation. Similarly, two or more NPOs may jointly control an asset. In addition, an NPO may also have joint control in a jointly controlled entity with other enterprises that may be in any form of organisation. Accordingly, in such cases, NPOs should report their interests in such joint ventures in separate as well as in consolidated financial statements (prepared as per AS 21) in accordance with the requirements of AS 27.

In respect of the funds created in the financial statements, the NPO should disclose the following in the Schedules/Notes to the accounts:

-

In respect of each major fund, opening balance, additions during the period, deductions/utilisation during the period and balance at the end;

-

Assets, such as investments, and liabilities related to each fund separately;

-

Restrictions, if any, on the utilisation of each fund balance;

-

Restrictions, if any, on the utilisation of specific assets.

NPOs should also disclose the following in the Notes to accounts:

- Details of the services rendered by volunteers for which no payment has been made.

- Fair value of the non-monetary grants and donations, e.g., a fixed asset received free of cost during the year. The quantitative details of such grants and donations should be separately disclosed.

- Fair values of all the assets, received as non-monetary grants, existing on the balance sheet date, should be separately disclosed. If it is not practicable to determine the fair values of the assets on each balance sheet date, then such values may be determined after a suitable interval, say, every three years, and disclose the date of determination, along with the fair values. The fair value of an asset would normally be the market price in an active, liquid and freely accessible market. The market price of an item can be the purchase price of the item donated, where the proof of purchase price is available, e.g., the donor has provided the invoice received from the supplier, declaration for customs duty purposes where the assets have been received from abroad, etc. In case the market price of the asset is not available, then the market price of a comparable asset may be used as fair value. It is recommended that the method of determination of fair value is also disclosed.

Format of Financial statements of NPOs

Disclaimer: This document is intended solely for educational purposes. The content herein is subject to change based on evolving finance trends and any relevant rulings by the Government of India. Readers are advised to consult with qualified professionals for specific guidance related to their individual circumstances.

The financial statements should give a true and fair view of the state of affairs of the NPOs, comply with the applicable Accounting Standards and shall be in the form as provided hereafter.

Part I – General Instructions for the preparation of Balance Sheet and Income and Expenditure Account of Not-For- Profit Organisations

-

These formats are recommended for preparation of Balance Sheet and Income and Expenditure Account of NPOs. Where compliance with the requirements of the relevant statute including Accounting Standards as applicable to the NPOs require any change in treatment or disclosure including addition, amendment, substitution or deletion in the head or sub-head or any changes, inter se, in the financial statements or statements forming part thereof, the same should be made and the formats should be modified accordingly.

-

The disclosure requirements recommended in the formats are in addition to and not in substitution of the disclosure requirements specified in the Accounting Standards issued by the Institute of Chartered Accountants of India. Additional disclosures specified in the Accounting Standards should be made in the notes to accounts or by way of additional statement unless required to be disclosed on the face of the Financial Statements. Similarly, all other disclosures as required by the relevant statute should be made in the notes to accounts in addition to the requirements set out in these formats.

-

The financial statements of NPOs (viz., balance sheet and income and expenditure account) should be prepared on an accrual basis.

-

A statement of all significant accounting policies adopted in the preparation and presentation of the balance sheet and the income and expenditure account should be included in the NPO’s balance sheet.

-

Accounting policies should be applied consistently from one financial year to the next. Any change in the accounting policies which has a material effect in the current period or which is reasonably expected to have a material effect in later periods should be disclosed. In case of a change in accounting policies which has a material effect in the current period, the amount by which any item in the financial statements is affected by such change, should also be disclosed to the extent ascertainable. Where such an amount is not ascertainable, wholly or in part, the fact should be indicated with reasons.

-

The accounting treatment and presentation in the balance sheet and the income and expenditure account of transactions and events should be governed by their substance and not merely by the legal form.

-

In determining the accounting treatment and manner of disclosure of an item in the balance sheet and/or the income and expenditure account, due consideration should be given to the materiality of the item.

-

(i) Notes to accounts may contain information in addition to that presented in the Financial Statements and may provide where required

(a) narrative descriptions or disaggregations of items recognised in those statements; and

(b) information about items that do not qualify for recognition in those statements.

(ii) Each item on the face of the Balance Sheet and Income and Expenditure Account should be cross-referenced to any related information in the notes to accounts. In preparing the Financial Statements including the notes to accounts, a balance should be maintained between providing excessive detail that may not assist users of financial statements and not providing important information as a result of too much aggregation.

-

(i) Depending upon the Gross Income of the Non-Company NPOs, the figures appearing in the Financial Statements may be rounded off as given below:—

|

Gross Income |

Rounding off |

|

(a) less than one hundred crore rupees |

To the nearest hundreds, thousands, lakhs or millions, or decimals thereof. |

|

(b) one hundred crore rupees or more |

To the nearest lakhs, millions or crores, or decimals thereof. |

(ii) Once a unit of measurement is used, it should be used uniformly in the Financial Statements.

-

Except in the case of the first Financial Statements prepared by the NPOs (after its incorporation) the corresponding amounts (comparatives) for the immediately preceding reporting period for all items shown in the Financial Statements including notes shall also be given.

-

For the purpose of this format, the terms used herein shall be as per the applicable Accounting Standards.

Note:—This part recommends the minimum requirements for disclosure on the face of the Balance Sheet, and the Income and Expenditure Account (and Notes. Line items, sub-line items and sub- totals shall be presented as an addition or substitution on the face of the Financial Statements when such presentation is relevant to an understanding of the NPOs financial position or performance or when required for compliance with the amendments to the relevant statutes or under the Accounting Standards.

-

A cash flow statement should be prepared, wherever applicable, showing cash flows during the period covered by the income and expenditure account and during the corresponding previous period.

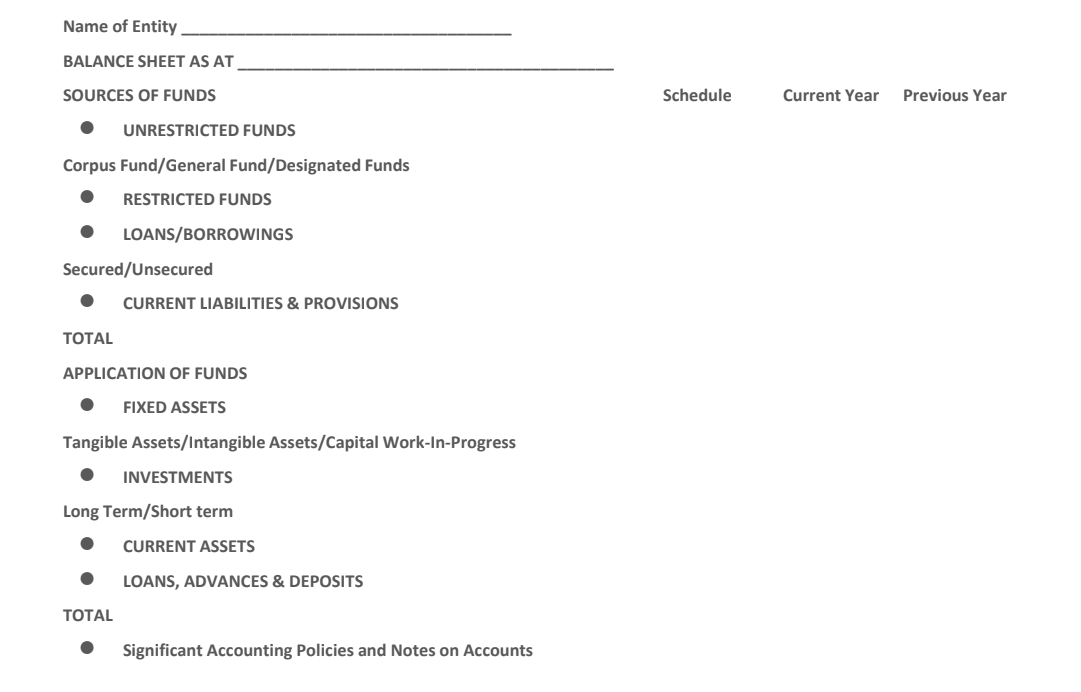

Format of Financial Statements (Not for Profit Organisation) Name of Not-for-Profit Organisation

BALANCE SHEET AS AT

(figures in Rs….)

Notes |

Figure as at the end of the current reporting period (DD/MM/YYYY) |

Figure as at the end of the previous reporting period (DD/MM/YYYY) |

||

|

I |

SOURCES OF FUNDS |

|||

|

(1) |

NPO FUNDS |

|||

|

UNRESTRICTED FUNDS |

||||

|

RESTRICTED FUNDS |

||||

|

(2) |

NON-CURRENT LIABILITIES |

|||

|

Long-Term borrowings |

||||

|

Other Long-Term Liabilities |

||||

|

Long-Term Provisions |

||||

|

(3) |

CURRENT LIABILITIES |

|||

|

Short Term |

||||

|

Borrowings |

||||

|

Payables |

||||

|

Other Current Liabilities |

||||

|

Short Term Provisions |

||||

|

TOTAL |

||||

| II |

APPLICATION OF FUNDS |

|||

| (1) |

NON-CURRENT ASSETS |

|||

|

Property, Plant and Equipment & Intangible Assets |

||||

|

Property, Plant & Equipment |

||||

|

Intangible Assets |

||||

|

Capital Work in Progress |

||||

|

Intangible assets under Development |

||||

|

Long-Term Investments |

||||

|

Long-Term Loans and Advances |

||||

|

Other Long-Term Assets (specify nature) |

||||

|

CURRENT ASSETS |

||||

|

Current Investments |

||||

|

Inventories |

||||

|

Receivables |

||||

|

Cash and bank balances |

||||

|

Short-term Loans & Advances |

||||

|

Other Current Assets |

||||

|

TOTAL |

See accompanying notes which form part of the financial statements

Notes:

GENERAL INSTRUCTIONS FOR PREPARATION OF BALANCE SHEET

-

An asset shall be classified as current when it satisfies any of the following criteria:

-

it is expected to be realized within twelve months after the reporting date; or

-

it is cash or cash equivalent unless it is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting date.

-

All other assets shall be classified as non-current.

-

A liability shall be classified as current when it satisfies any of the following criteria:

-

it is due to be settled within twelve months after the reporting date; or

-

the NPO does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting date.

-

All other liabilities shall be classified as non-current.

-

An NPO shall disclose the following in the Notes to Accounts:

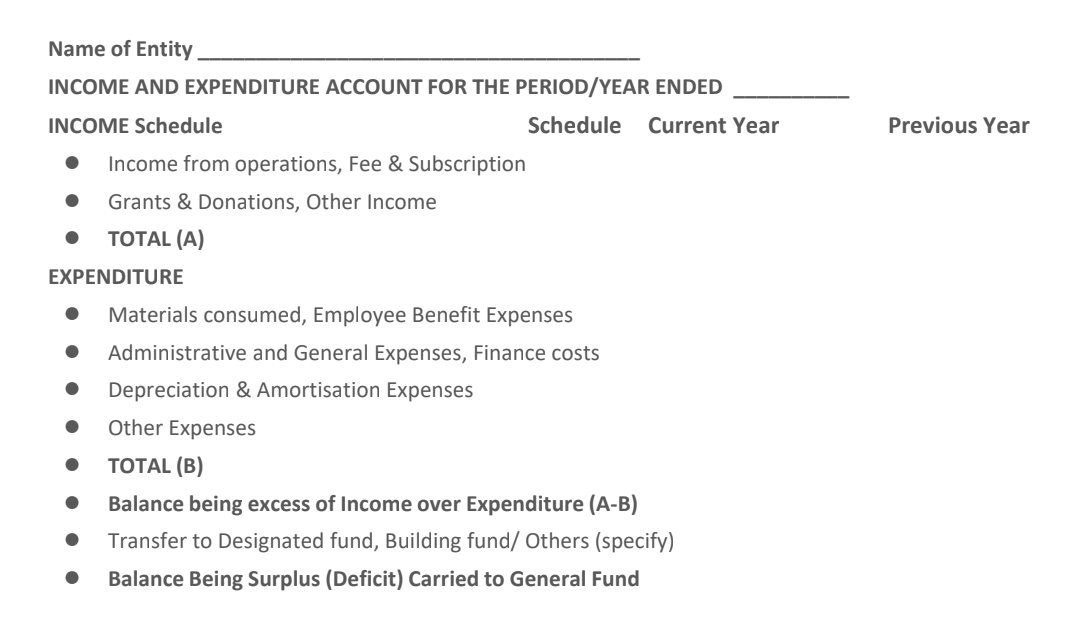

Form of Income and Expenditure Account

Name of Not-for-Profit Organisation

INCOME AND EXPENDITURE ACCOUNT FOR THE YEAR ENDED

|

Particulars |

Figures for the current reporting period from --- (DD/MM/YYY) to --- (DD/MM/YYY) |

Figures for the previous reporting period from --- (DD/MM/YYY) to --- (DD/MM/YYY) |

|||||

|

Unrestricted Funds |

Restrict ed Funds |

Tota l |

Unrestri cted Funds |

Restricted Funds |

Total |

||

|

I |

INCOME |

||||||

|

Donations and Grants |

|||||||

|

Fees from Rendering of services |

|||||||

|

Sale of goods |

|||||||

|

II |

Other Income |

||||||

|

III |

Total Income |

||||||

|

IV |

EXPENDITURE |

||||||

|

Materials consumed/ distributed Opening balance Add: Purchases Less: Closing balance |

|||||||

|

Donation/contribu tion paid |

|||||||

|

Employee Benefit Expense |

|||||||

|

Depreciation and amortization expense |

|||||||

|

Finance Cost |

|||||||

|

Other Expenses

|

|||||||

|

Total Expenses |

|||||||

|

V |

Excess of Income over Expenditure for the year before exceptional and extraordinary items (III-IV) |

||||||

|

VI |

Exceptional items (specify nature and provide note/delete if none) |

||||||

|

VII |

Excess of Income over Expenditure for the year before extraordinary items (V-VI) |

||||||

|

VIII |

Extraordinary items (specify nature and provide note/delete if none) |

||||||

|

IX |

Excess of Income |

|

over Expenditure for the year (VII- VIII) |

|||||||

|

Appropriations Transfers to funds, e.g., Building fund Transfers from funds |

|||||||

|

Balance transferred to General Fund |

Part IV: GENERAL INSTRUCTIONS FOR PREPARATION OF INCOME AND EXPENDITURE Account

-

The income and expenditure account should disclose every material feature and should be so made out as to clearly disclose the result of the working of the NPO during the period covered by the account.

-

Donations and grants should be recognised only at a stage when there is a reasonable assurance that:

-

the NPO will comply with the conditions and obligations attached, and

-

the donations and grants will be received.

-

Depreciation should be provided so as to charge the depreciable amount of a depreciable asset over its useful life.

-

Fair value and quantitative details of items, being sold or being distributed free of cost or at nominal amount that have been received as non-monetary grants and donations, should be disclosed as, in the notes to accounts:

Balance at the beginning of the year Add: Receipts during the year

Less: Distribution during the year: Sale during the year Balance at the end of the year

-

Finance Costs shall be classified as:

-

Interest expense

-

Other borrowing costs;

-

Applicable net gain/loss on foreign currency transactions and translation

-

Other Income shall be classified as:

-

Interest Income;

-

Dividend Income;

-

Net gain/loss on sale of investments;

-

Other income (net of expenses directly attributable to such income).

-

Following shall be disclosed by way of notes regarding aggregate expenditure and income on the following items:

(i)

- Employee Benefits Expense showing separately (i) Salary and wages (ii) Contribution to provident and other funds, (iii) staff welfare expenses

-

Any item of income or expenditure which exceeds 1 percent of the gross income of the NPO or Rs. 1,00,000/-, whichever is higher

-

Adjustments to the carrying amount of investments

-

Net gain or loss on foreign currency transaction and translation (other than considered as finance cost)

-

Details of items of exceptional and extraordinary nature;

-

Prior period items.

(ii) Expenditure incurred on each of the following items, separately for each item:

- Consumption of stores and spare parts;

- Power and fuel;

- Rent;

- Repairs to buildings;

- Repairs to machinery;

- Insurance;

- Rates and taxes;

- Miscellaneous expenses